Stockwatch: This high-profile small-cap could fly

There are early signs of green shoots at this well-known tiddler, but this is for brave investors.

14th May 2019 12:18

by Edmond Jackson from interactive investor

There are early signs of green shoots at this well-known tiddler, but this is for brave investors.

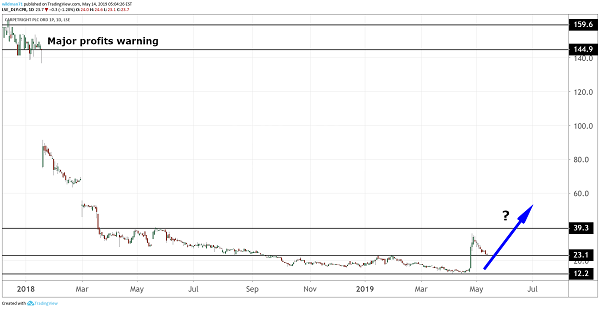

Does a 70%-plus spike in the shares of UK floor coverings retailer Carpetright (LSE:CPR) to near a one-year high suggest they have broken with disillusion that has persisted since early 2018?

The price had crept up ahead of a 25 April trading update and doubled on excitement about an "improved" revenue trend in recent months. It tested 34p but has retreated to 24p (lately with the markets' slide) for a market cap around £60 million.

Mind how the number of shares in issue has increased from 67 million (cited in some tables) to 251 million due to a placing and open offer at 28p a year ago. Raising £60 million net was an important first step in a turnaround programme to cut debt, implement a Company Voluntary Arrangement (CVA) to restructure the store portfolio.

- Invest with ii: Top UK Shares | Share Prices Today | Open a Trading Account

The money will also fund recovery and reduce trade debtors (one of my regular warning signals where a big imbalance with trade creditors can imply delayed payments supporting profit or mitigating losses).

But the fundraising will mean a substantial dilutive effect on earnings per share (EPS), even if Carpetright's £19 million cost-cutting programme re-rates profit, so beware historic figures in the table.

Source: TradingView Past performance is not a guide to future performance

Tussle versus Tapi may be the chief factor overall

The context is Carpetright shares down from over 600p in mid-2015 when the business made around £14 million normalised pre-tax profit, albeit (see table) on a very low operating margin around 2%, making profit vulnerable to weaker revenue.

Such risk manifested itself with the founding of Tapi Carpets & Floors in 2015 by the Harris family, who were the original founders of Carpetright but sold all their equity, backed afresh by substantive investors able to take a long-term view.

Companies House records show Tapi's 2017 accounts (filed October 2018) with turnover up 88% to £56 million and losses up from £10.2 million to £10.9 million as 24 new stores took the total to 91 at end-2017 and a further 8 during 2018 took the total to 111. Tapi's directors were confident of moving into profit, citing a higher gross margin of 58.1% and "an industry leading Trustpilot rating of 9.5 with the majority of customers rating their experience at 4 or 5 out of 5."

While this sounds competitively horrific, and Trustpilot.com currently shows an "Excellent" five-star rating based on 6,679 reviews for Tapi, it also gives Carpetright five stars based on 35,425 reviews.

Mind there's criticism about how independent or prompted are Trustpilot reviews. AIM-listed Purplebricks (LSE:PURP), nowadays struggling in a stagnant property market, also attracted similar past positive reviews. Elsewhere, Reviews.co.uk give Carpetright a 1.34 rating based on 418 reviewers with only 7% recommending, while Tapi get 5.00 and are 100% recommended albeit with only 4 reviews to date.

There's also a dilemma about how reviews may only appear when customers have a gripe – and some inevitably will – so 418 is tiny in context.

Yet it's vital to be aware that you can pour over Carpetright's figures, but the crux for its shares is how the tussle with Tapi evolves in a challenged consumer environment.

A trading improvement of sorts

The 25 April update affirmed overall expectations for the year to end-April 2019, like February's did after the December interims.

What triggered buying zeal was the UK like-for-like sales trend improving "significantly" in the fourth quarter (Feb to April) "as customer confidence in the business started to return following the group’s restructuring last year."

Possibly some buyers interpreted this as a nominally positive sales trend, but the 11 December interims showed fiscal first-quarter sales down 16.8% like-for-like and 8.9% down in Q2 – said to be due to a negative brand impact of engaging the CVA.

Last February's update in respect of fiscal Q3 didn’t quantify but cited the UK trend remaining negative albeit improving relative to the first half. Continental European sales are faring better thanks to strong performance in the Netherlands, albeit are only 22% of group total. So it's entirely possible the Q4 "significant improvement" saw the trend at say minus 2-3%, and quite whether it’s a blip or the start of something stronger.

Home sales are currently sluggish due to Brexit uncertainties dragging on. Yes, carpets and floors still need replacing, but moving house is a more likely prompt to refresh.

| Carpetright - financial summary | Broker estimates | ||||||

|---|---|---|---|---|---|---|---|

| year ended 30 Apr | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Turnover (£ million) | 448 | 470 | 457 | 458 | 444 | ||

| IFRS3 pre-tax profit (£m) | -7.2 | 6.6 | 12.8 | 0.9 | -70.5 | ||

| Normalised pre-tax profit (£m) | 4.9 | 14.2 | 17.3 | 13.4 | -58.0 | 13.7 | 16.2 |

| Operating margin (%) | 0.7 | 1.8 | 2.7 | 1.9 | -14.0 | ||

| IFRS3 earnings/share (p) | -5.3 | 6.7 | 14.9 | 1.1 | 1.1 | ||

| Normalised earnings/share (p) | 12.5 | 17.9 | 21.5 | 19.2 | -94.6 | -4.9 | 1.3 |

| Earnings per share growth (%) | 2.3 | 43.0 | 20.5 | -11.0 | |||

| Price/earnings multiple (x) | -0.3 | -4.9 | 18.5 | ||||

| Annual average historic P/E (x) | 28.8 | 15.5 | 9.9 | 5.7 | |||

| Cash flow/share (p) | 13.6 | 28.2 | 12.3 | 8.1 | -36.4 | ||

| Capex/share (p) | 15.1 | 11.2 | 14.3 | 20.7 | 24.9 | ||

| Net tangible assets per share (p) | 3.7 | 5.0 | 24.9 | 30.5 | -10.8 | ||

| Source: Company REFS | |||||||

Black clouds at interims albeit a silver lining too

The May to October 2018 period was politely described as "a transitional year" given an operating "EBITDA" loss of £1.7 million on revenue down 15.7% to £191.1 million and the statutory loss up from £0.6 million like-for-like to £11.7 million.

Net debt fell to £12.4 million from £53 million in April 2018. Not to succumb unduly to risk warnings in company updates - that nowadays can be severe in order to cover all bases - but Carpetright's risk/reward profile looks pretty hairy according to how trading evolves.

The interims cautioned about regular covenant testing with the company's principal banking facility due to expire at end-December 2019, where if Carpetright doesn't suffice then there's "a material uncertainty which may cast significant doubt about the group's ability to continue as a going concern." That could take the stock down to single penny status.

More positively, it's the board's objective to complete a refinancing prior to announcing prelims on 25 June, which would potentially be seen as bankers viewing the situation well, at least for them to earn interest/fees. As of last October, the board took the view the group was resourced to operate for a minimum 12 months.

So, with retail still tough and no sign of insider buying now Carpetright should be out of any closed period, it’s hardly surprising profit takers have emerged after the stock spike.

Stock rating reflects confidence in turnaround

Carpetright's situation is potentially mercurial that forecasts seem unreliable – but say the 2020 year projection (according to Company REFS, dated 17 March and most likely by Carpetright's broker i.e. signed off by management) for EPS of 1.3p is reasonably indicative of the extent of dilution, a forward price/earnings (PE) ratio of around 18.5x shows the stock at a reasonably fair level now that the market entertains improving chances of corporate recovery.

According to the classic pattern of turnarounds – capital-raising and radical cost-cutting – Carpetright bodes well, although the present CEO has been in position since 2014 so must share responsibility about why actions – like reducing store lease length - were not taken sooner.

Clearly from the table the operating margin needs to improve massively and the interims gave no confidence on that score, although on a 1-2 year view Carpetright could indeed emerge with a more attractive cost base. But don't lose sight that, despite Tapi, it's still the leading UK carpet/floorings retailer.

So, it's a risky bet - most investors will prefer to avoid - yet speculators will recognise the potential for a steady, if volatile, re-rating. You may get a chance to accumulate at lower prices, yet broadly and sticking my neck out: Speculative Buy.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.