Stockwatch: Why fears of Tullow Oil’s demise are overdone

The shares are worth a fraction of what they were, but our companies analyst has more faith.

13th December 2019 13:08

by Edmond Jackson from interactive investor

The shares are worth a fraction of what they were, but our companies analyst has more faith.

While “Avoid” is a broadly fair stance – respecting risks for the average retail investor – the market’s knee-jerk reaction against mid-cap oil company Tullow Oil (LSE:TLW) went too far this week versus current evidence.

Last Tuesday’s downgrades to production and, more significantly, cashflow prompted analysts to speak of a rescue rights issue and enough shareholders to panic-sell amid fear of banks taking control should Tullow be unable to meet its debt obligations.

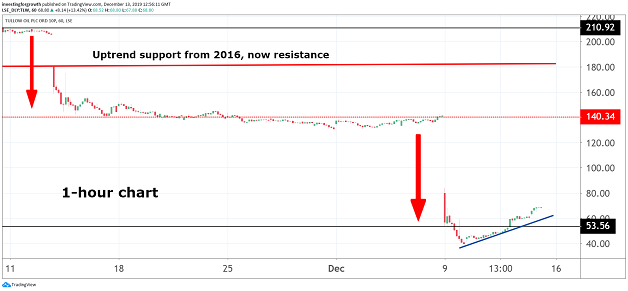

M&G fund managers dumped stock at presumably distress prices – down to 40p relative to 240p eight months ago, or 1,270p in 2012. One report said the company “has to pay down $2.9 billion (£2.2 billion) net debt”. Well, the debt has looked excessive for a while, but essentially Tullow needs to settle a $300 million convertible bond maturing in 2021 and $650 million of bonds maturing in 2022.

It does have $1 billion of liquidity headroom via current facilities, ample despite a prospect of their narrowing, and, though slashing the dividend meant some drastic headlines, the financial summary shows it should anyway never have been reinstated. So, the stock is rebounding, and currently sits near 67p.

Source: TradingView Past performance is not a guide to future performance

Risk/reward may tilt overall positively at this level

Be aware, the situation is highly speculative due to a range of possible outcomes. But I think shareholders can take heart that, unless oil prices slide and/or an operations review underway reveals new nasties that materially compromise Tullow’s asset base, either its Executive Chair (stepping up from a non-executive role) stands a good chance of managing through.

Tullow’s reserves are broadly unchanged despite production issues, offering scope for disposals. It’s possible the likes of an opportunistic hedge fund reckon on a sum-of-parts value that argues for taking a stake and hassling for asset sales, even a full takeover.

Exploration values “in the market price for free”?

Tullow’s end-June 2019 balance sheet had $4.9 billion property/plant/equipment and $1.9 billion intangible value ascribed to exploration/evaluation assets. Accounting values like this are to an extent questionable (both ways) but, even so, and despite $3.3 billion long-term debt and thumping trade payables - $1.3 billion short-term and another $1.3 billion longer-term - plus $1.1 billion deferred tax liabilities, net assets were $2.8 billion.

That represents a per share equivalent of 152p. Knocking off 100p, which equates to the per share value of exploration/evaluation assets, share buyers this week have pretty much got those “for free” as the stock rose to 60p. Yes, that’s a simple view and balance sheet values are a moving feast, but the market rebound has a rationale.

A long-term strategic dilemma is exploration & production firm Tullow being pretty impressive at the “E” side of things, discovering major assets offshore Ghana – the Jubilee field and three-field “TEN” complex – but running into issues when it came to “P”, developing those assets. To me it seems success possibly went to their heads and they tried to have it all as an E&P business.

Recalling the managers of oil & gas E&P’s 20 years and more ago, they were more modest: debt was generally avoided; exploration funded from mature cash generative production assets typically acquired from the “majors” that didn’t need a lot of technical development; and dedicated explorers would promptly sell on their finds, sticking to their skills.

Tullow has been variously ambitious, ending up a mess, albeit one – on the current evidence – that stands a fair chance of being unpicked.

Can Dorothy Thompson defy a key Buffett adage?

The odds are raised by Tullow coincidentally being chaired by the ex-CEO of Drax Group (LSE:DRX). While I’m unimpressed by Drax’s long-term financial record from power generation, she has over time gained a strong City fan club and is taking firm action here since her appointment in July 2018 – removing the incumbent CEO/exploration director, and re-appraising the cost base and investment plans, to bolster cash flow.

Downgrades to group production aren’t so bad: around 70,000 barrels of oil equivalent per day projected over the next three years, down from 87,000 b/d previously expected for 2019 and 100,000 b/d for 2020. The dilemma is its effect on cashflow that’s now guided to plunge from around $500 million to just $150 million – but at least this is now prioritised for turnaround.

A cynic might recall Warren Buffett’s adage:

“When a manager with a reputation for excellence tackles a business with a reputation for bad fundamental economics, it’s the reputation of the business that stays intact.”

I’d differentiate: the fundamentals of E&P can be made to work; it’s that Tullow has over-ambitiously made a hash of them.

| Tullow Oil - financial summary | ||||||

|---|---|---|---|---|---|---|

| Year ending 31 Dec | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| Turnover ($ million) | 2,647 | 2,213 | 1,607 | 1,360 | 1,885 | 2,048 |

| Operating margin (%) | 14.4 | -88.8 | -68.1 | -55.5 | 1.2 | 25.8 |

| Operating profit ($m) | 381 | -1965 | -1094 | -755 | 22.4 | 528 |

| Net profit ($m) | 169 | -1,556 | -1,035 | -600 | -176 | 84.8 |

| Reported earnings/share ($) | 0.2 | -1.5 | -1.0 | -0.6 | -0.1 | -0.1 |

| Normalised earnings/share ($) | 0.7 | 0.3 | -0.2 | 0.1 | 0.2 | 0.2 |

| Price/earnings multiple (x) | 4.1 | |||||

| Operating cashflow/share ($) | 1.6 | 1.4 | 0.9 | 0.5 | 1.0 | 0.8 |

| Capex/share ($) | 1.9 | 2.2 | 1.6 | 1.0 | 0.2 | 0.3 |

| Free cashflow/share ($) | -0.3 | -0.8 | -0.7 | -0.5 | 0.7 | 0.5 |

| Dividend per share ($) | 0.2 | 0.05 | ||||

| Covered by earnings (x) | 0.9 | 1.2 | ||||

| Net assets per share ($) | 5.0 | 3.7 | 3.0 | 2.1 | 2.0 | 2.1 |

| Source: historic Company REFS and company accounts |

Key news hurdles in the near term

This stock’s risk/reward profile rests in a company-specific sense, on the outcome of a thorough operational review – with an update on progress due within a trading statement on 15 January, then more thoroughly at prelims on 12 February. And in a macro sense, you have to assume oil prices being reasonably stable.

On both counts, however, I think it should be possible to manage through and re-set Tullow. If the company’s reserves base was looking shaky, or it lacked financial headroom, then there would be a risk of genuine crisis. More likely, new nasties will be needed to trigger one. With the US and China finally appearing to see sense in finding a trade accord, or at least stop their mutually defeating tit-for-tat, this would remove a key risk of oil prices falling.

For the rest of 2019, however, a next pivot for sentiment is the outcome of drilling the Carapa-1 well – to test a deeper Cretaceous play in Tullow’s offshore Guyana acreage. Tullow has a 37.5% stake, where test results are made more significant by November’s revelation that oil from offshore Guyana discoveries was heavy/sulphurous – i.e. less economic to refine.

Oil quality may be less of an issue this time following a light oil discovery in the zone nearby. Moreover, Tullow says around half of potential reserves across two blocks are likely located in the Cretaceous zone. But with sensitivities running high towards Tullow, a sense of “winner versus duster” on this well is likely. Traders are dominating the stock currently, apt towards a binary view.

I would put the question of a new chief executive to one side for the time being; it’s not a critical issue relative to clearing the decks and setting a new course. Tullow will prefer to get the appointment right and, equally, the best talent will likely want to see conclusions of the operational review. Such an absence is conceivably a plus by way of raising takeover/break-up interest.

Technical chart factors possibly applying

There appeared a classic institutional shareholder capitulation, where on 9 December M&G went from holding 5.89% to sub-5% implicitly at a distressed price. Who knows if they just sold what they could to reduce exposure or are completely out; such is the occasional ambiguity of regulatory announcements.

Computers appear to pick up on and extend trends in the very short term - intraday charts showing advances and periods of flat-lining, punctuated with profit-taking. Yet, with the stock testing 69p this Friday, the rebound continues. Excepting bad news from Carapa-1, I think holders can take some comfort the market is testing for fair value higher still. Obviously, much remains speculative.

Yes, investors should avoid highly indebted companies that are effectively using debt to pay dividends, where in the resources sector extraction issues and commodity price volatility, combined with operational gearing, can be disastrous. Yet big share price falls at companies with assets to work with, and financial headroom, are likely to trigger a rebound. Hold.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.