A buying opportunity at a brand with strength and spread

10th August 2022 08:42

by Rodney Hobson from interactive investor

This firm’s products are found in almost every home in the West, there is a chance of a dividend being introduced, and the company has a momentum that is unlikely to slow, says our overseas investing expert.

Its products are found in almost every home in the Western world yet its shares are ignored by most investors. The company is Mattel (NASDAQ:MAT).

It makes toys and sells them to retailers and directly to consumers. Its products include some of the most famous lines for preschool and infant children such as Barbie dolls, Polly Pocket, Fisher-Price and Thomas the Tank Engine. It also holds exciting film franchises including Jurassic Park.

Second-quarter results were pretty good, rounding off a first half that chairman and chief executive Ynon Kreiz described as an outstanding period of growth.

- Discover more: Buy international shares | Interactive investor Offers | Most-traded US stocks

Second-quarter net sales were an impressive 20% up on the previous year at $1.24 billion despite the strength of the dollar providing a tough headwind. Adjusted earnings per share soared from 3 cents to 18 cents.

North America, which accounts for roughly half of revenue, led the way with sales up 30% as demand for a wide range of products such as action figures, building sets and dolls soared.

- Two big dividends for adventurous income seekers

- A profit machine to buy and a tempting recovery play

There were just a couple of slight niggles: gross margins were tighter and sales of American Girl such as Barbie dolls were poor. Gross margins were, however, still substantial at 44.9% as cost inflation, additional supply chain costs and extra royalty payments were offset by increased selling prices and strict control of fixed costs.

Much now depends on how well the crucial Christmas period goes. An early encouraging sign is that in the US the economy is charging ahead much better than expected in the post-pandemic period. Jobs and wages show no sign of weakening despite hefty interest rate rises that are set to continue. Indeed, Mattel itself, like other American employers, is having to pay higher wages to attract and retain staff.

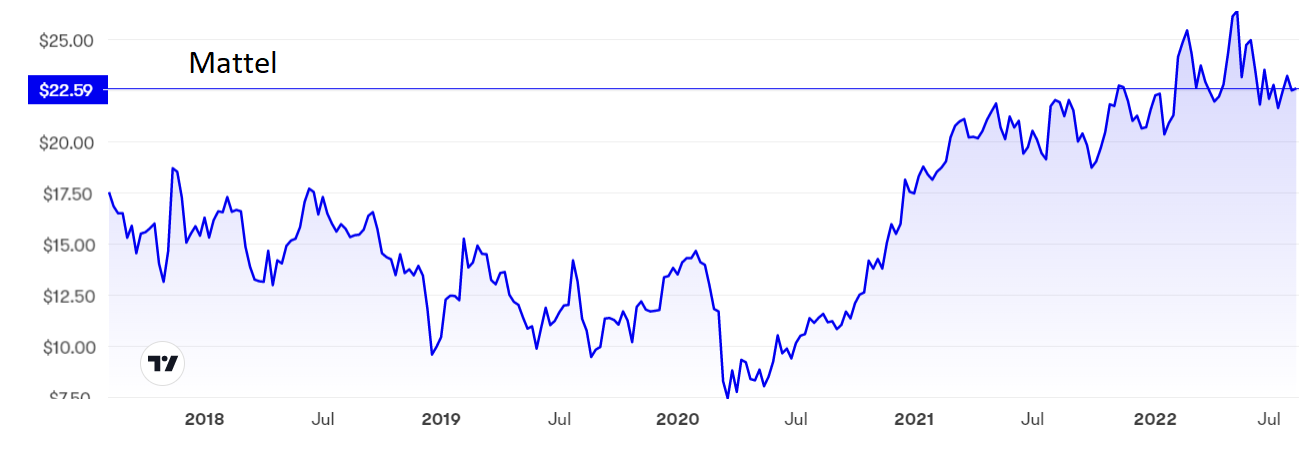

Source: interactive investor. Past performance is not a guide to future performance.

Despite the increasingly partisan nature of American politics, Congress has approved several measures that will pump $3.5 trillion into the economy. It is hard to see parents turning into Scrooges by the time the festive season arrives.

Even so, Mattel is cautiously predicting much slower growth in the second half, leaving sales up only 8-10% for the full year. This guidance is likely to be beaten, especially if supply chain issues ease as seems to be happening across various sectors.

More importantly, full-year earnings per share are projected at $1.42-1.48, reflecting the bias towards the second half. Again this is more likely to be an under, rather than an over, estimate, which is why analysts are currently going for something a little higher, especially if gross margins edge up again to a projected 47-48%.

There is scope for further price rises, since Mattel’s prices are not expensive compared with other toy makers.

- Two stocks to keep your portfolio clean and healthy in a downturn

- Ask ii...what are the pros and cons of investing in a US company?

Mattel has also made forecasts for next year, suggesting net sales will grow at a similar level to this year, producing earnings per share that top $1.90. A lot can happen over the next 18 months and investors should take this forecast with some caution.

However, it does show management’s confidence that the company has a momentum that is unlikely to slow, let alone judder to a halt. Given the strength and spread of the brands, this confidence looks fully justified.

The shares dropped below $8 in March 2020 but are now back above pre-pandemic levels at $22.50, where the price/earnings ratio is an undemanding 7.26. It is disappointing that there is no dividend, but if sales and profits go as well as management expects then there is every chance that one will be introduced in the foreseeable future.

Hobson’s choice: Buy up to $25, which could prove a temporary ceiling. There is a floor at $21.50 and the momentum is upwards.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.