Follow the top funds into this computer chip star

Rapid growth at this lesser-known semiconductor giant has got our international shares analyst excited.

20th November 2019 11:20

by Rodney Hobson from interactive investor

Rapid growth at this lesser-known semiconductor giant has got our international shares analyst excited.

Rodney Hobson is an experienced financial writer and commentator who has held senior editorial positions on publications and websites in the UK and Asia, including Business News Editor on The Times and Editor of Shares magazine. He speaks at investment shows, including the London Investor Show, and on cruise ships. His investment books include Shares Made Simple, the best-selling beginner's guide to the stock market. He is qualified as a representative under the Financial Services Act.

There were fears that sales of semiconductors, the most important parts of the electronics supply chain, were stalling earlier this year. Recent trading updates across the sector suggest that growth is back on the agenda, and one attractive investment is Taiwan Semiconductor Manufacturing (NYSE:TSM), which designs, makes and tests integrated circuits and other semiconductor devices.

Its headquarters and main operations are located in the Hsinchu Science and Industrial Park in Taiwan, and the shares are quoted in Taipei, but interactive investor customers can buy them in the form of American depository receipts (ADRs) traded on the New York Stock Exchange.

Founded in 1987, the company has always placed a strong emphasis on its own research and development. Investors should be warned that a visit to TSMC's website is challenging for those unfamiliar with semiconductor technology, with its references to global capacity of more than 12 million 12-inch equivalent wafers per year, and the broadest range of technologies from 2 micron all the way to the most advanced processes, currently 7-nanometer.

Easier to comprehend is that third-quarter net revenue came in at $9.4 billion, up 10.7% on the same period last year and even better than the optimistic guidance given earlier by the company. Significantly, the figure was 21.3% ahead of the disappointing second quarter of 2019, when sales were depressed as customers digested the latest technological updates.

Margins, which had been squeezed earlier this year, recovered to last year’s levels and were at the top end of the guidance range.

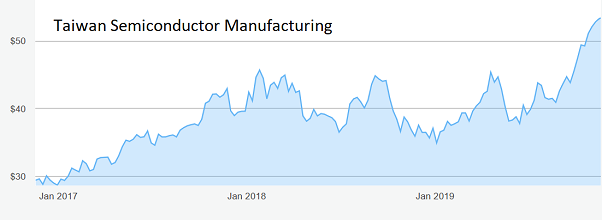

Source: interactive investor Past performance is not a guide to future performance

The prognosis for the fourth quarter, based on current business levels, is for revenue of $10.2 billion, a clear further quarterly gain. Margins are also set to improve.

Half the revenue comes from smartphone makers, sales that were up 33% quarter on quarter. High performance computing accounted for 29% of sales and, although this sector is showing decent growth, it is overshadowed at 10%. That could change dramatically, though, as industry experts believe this will be one of the biggest growth areas for semiconductors over the next two years.

High performance computing evolved as far back in the 1960s but tended to be very expensive to build and maintain. As with so much else in computing, massive leaps forward in technology and economies of scale have opened up opportunities for manufacturers to mass produce purpose-built high-performance chips tailored to individual customers.

- Stockwatch: The investment case for Apple

- Chart of the week: A fallen star stock in recovery mode?

- Get exposure to Asian equities via these ii Super 60 recommended funds

The interesting area is the much-hyped internet of things market. Although this is still only 9% of TSMC’s business it is the fastest growing with a 35% spurt and the one that may yet prove to be the boost that shareholders hope to see.

Automotive comes a distant fourth, just 4% of sales. Despite the travails of the motor industry around the globe, this section did manage decent growth of 20%. Computer chips have become a major part of modern vehicles, but it is hard to see this side of the business becoming a major part of TSMC, though any improvement in any part of the business is obviously welcome.

The shares stood at only $22 five years ago but peaked at $53.67 earlier this month. After settling back to $52 they are on the move again and have returned to their all-time high.

Although the best chance to buy has passed, the shares still offer good prospects with a yield of 3%, which is quite high for New York quoted stocks at the moment. The price/earnings ratio at 25.6 is somewhat toppy but, again, is not out of line for American stocks, especially those with excellent prospects.

Hobson's Choice: Buy at up to $55. You would be in good company as the stock is included in the portfolios of a number of respected funds, including Murray International (LSE:MYI) and JPM Asia Growth.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.