Share Sleuth adds an enchanting company at a decent price

Richard Beddard explains why Bloomsbury, the Harry Potter publisher, won out in a shares duel.

29th November 2019 09:11

by Richard Beddard from interactive investor

Richard Beddard explains why Bloomsbury, the Harry Potter publisher, won out in a shares duel.

This month Share Sleuth is spoilt for potential trades. Victrex (LSE:VCT), one of the most highly rated shares in Share Watch, is under-represented at 2.5% of the portfolio’s total value, whereas the share price of Judges Scientific has risen so much that the portfolio’s holding has grown to 8.5% of its total value, so it is over-represented.

Meanwhile, two companies I have evaluated for the first time, Bloomsbury Publishing (LSE:BMY) and PZ Cussons (LSE:PZC), scored highly and would probably make good additions. Finally, the annual re-evaluation of Alumasc (LSE:ALU) (see Share Watch) has put its place in the portfolio in jeopardy.

Attractive addition

Since we have cash to spare, I have gone with an addition rather than a disposal, so Alumasc gets a reprieve and the Judges Scientific (LSE:JDG) holding remains intact.

Because Victrex publishes its results soon, I have deferred a decision on adding more shares in the polymer manufacturer.In a straight duel between Bloomsbury Publishing and PZ Cussons, PZ Cussons comes out on top. It scores 7.7 out of 10 compared with 7.0 for Bloomsbury Publishing. I have gone for the publisher, though.

Both companies are changing shape in ways that may make them more profitable, but Bloomsbury is further advanced, so the opportunity to buy its shares at a decent price may be short-lived.

Bloomsbury is known mostly as the UK publisher of the Harry Potter books. The abnormal profits it earns from these means the books are by far the firm’s biggest money-spinner. But that balance may be shifting, as heavy investment in digital resources for universities and colleges begins to bear fruit. For decades Bloomsbury has been using the bounty from Harry Potter to expand abroad and acquire imprints and publishers, many of them academic.

Since 2016, it has been welding its academic titles into digital collections for libraries, in an initiative known as Bloomsbury Digital Resources. The investment has weighed on the profitability of Bloomsbury’s second-biggest division, Academic and Professional, but the division as a whole returned to profitability in the year to February 2019, and in the half year to August 2019 Bloomsbury Digital grew revenue by 76% and made a profit for the first time.

Bloomsbury is launching four or five digital collections a year until 2020 and expects to earn £15 million in revenue and £5 million in profit by 2022 from Bloomsbury Digital – highly profitable business that will balance Bloomsbury’s consumer and non-consumer divisions and make it much less dependent on the wizardry that has bankrolled it so far.

Bloomsbury sells other fiction and non-fiction titles too, while Potter’s appeal shows no sign of waning as parents introduce their children to the books and Bloomsbury releases new illustrated editions. There are risks: Amazon’s dominance of book retailing, for example, and the free publication of academic research through open access. But Bloomsbury is prospering alongside these developments.

On the face of it, the firm is a good business.Its return on capital in the year to February 2019 was 16%. Its share price of 259p, which values it at nearly £190 million or about 15 times adjusted profit, is a reasonable price to pay.

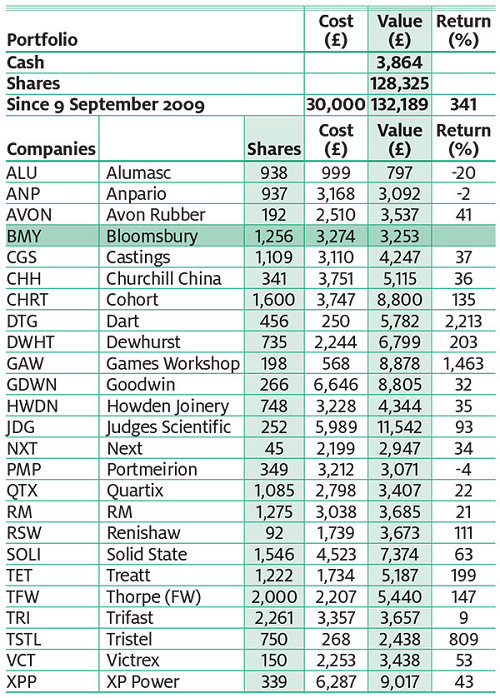

This is the first time I have investigated Bloomsbury, so I have committed only 2.5% of the portfolio’s total value to it (about £3,250), a proportion I dub the minimum trade size.On 1 November I added 1,256 shares. The total transaction, including charges in lieu of stamp duty (£16) and broker fees (£10) was £3,274.

Sleuth sustains successful spell

Bloomsbury looks a solid addition

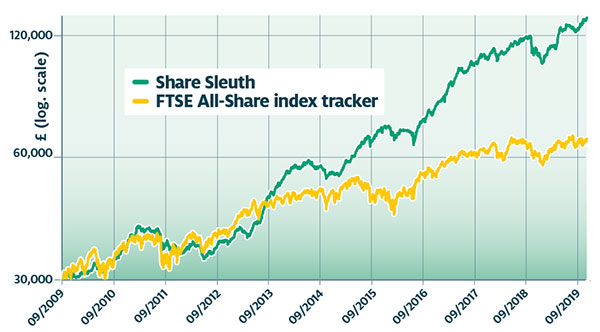

Notes: New additions in darker green. Transaction costs include £10 broker fee and 0.5% stamp duty where appropriate. Cash earns no interest. Dividends and sale proceeds are credited to the cash balance. £30,000 invested on 9 September 2009 would be worth £132,189 today. £30,000 invested in FTSE All-Share index tracker accumulation units would be worth £66,642 today. Objective: To beat the index tracker handsomely over five-year periods. Source: SharePad, as at 5 November 2019.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.