Personal Pension (SIPP) stories

The people switching and saving with ii

See why thousands of people have switched to ii's five-time Which? Recommended Personal Pension and started saving more money for their future.

Important information: The people featured in these videos are actual interactive investor SIPP customers and were remunerated for their time. The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

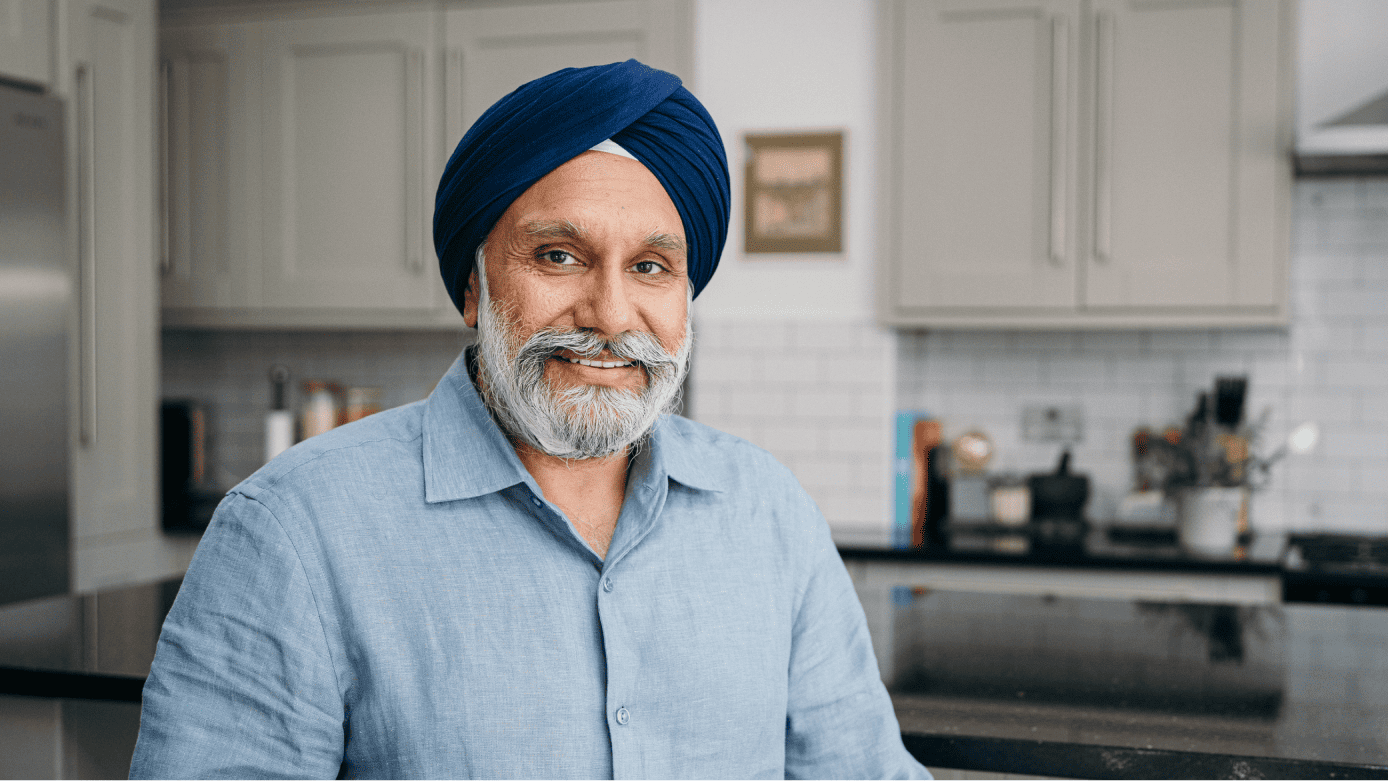

Fang’s saving more of her money

Fang wants to travel the world when she retires. With our low, flat fee, she’s in a better position to achieve what she wants. After a simple, pain-free transfer, she can rest easy.

“Once I heard flat fees, I jumped at it. I calculated all my other fees and I said ‘that’s really expensive compared to ii’. Why did I not do it earlier? That’s why I’m with ii.”

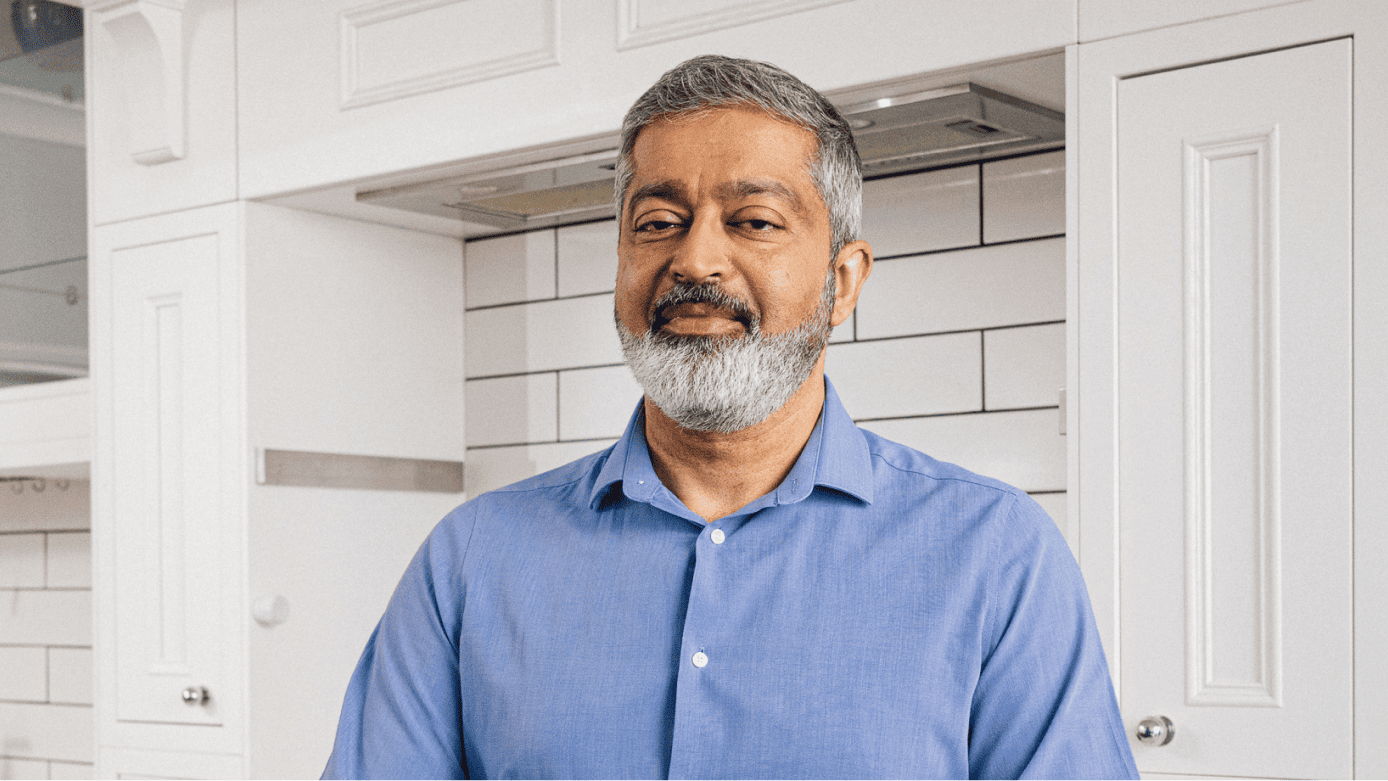

Enzo’s got more flexibility and control

Enzo felt it was time to tidy up his pensions and achieve his retirement goals. He chose the ii Personal Pension for the combination of flat fees, investment options and leading customer support.

“My previous providers were Aviva and Scottish Widows. I had the realisation that the fees element, compared to ii, didn’t sit too well with me. It was clear that ii is recognised as one of the best SIPP providers. That’s why I’m with ii.”

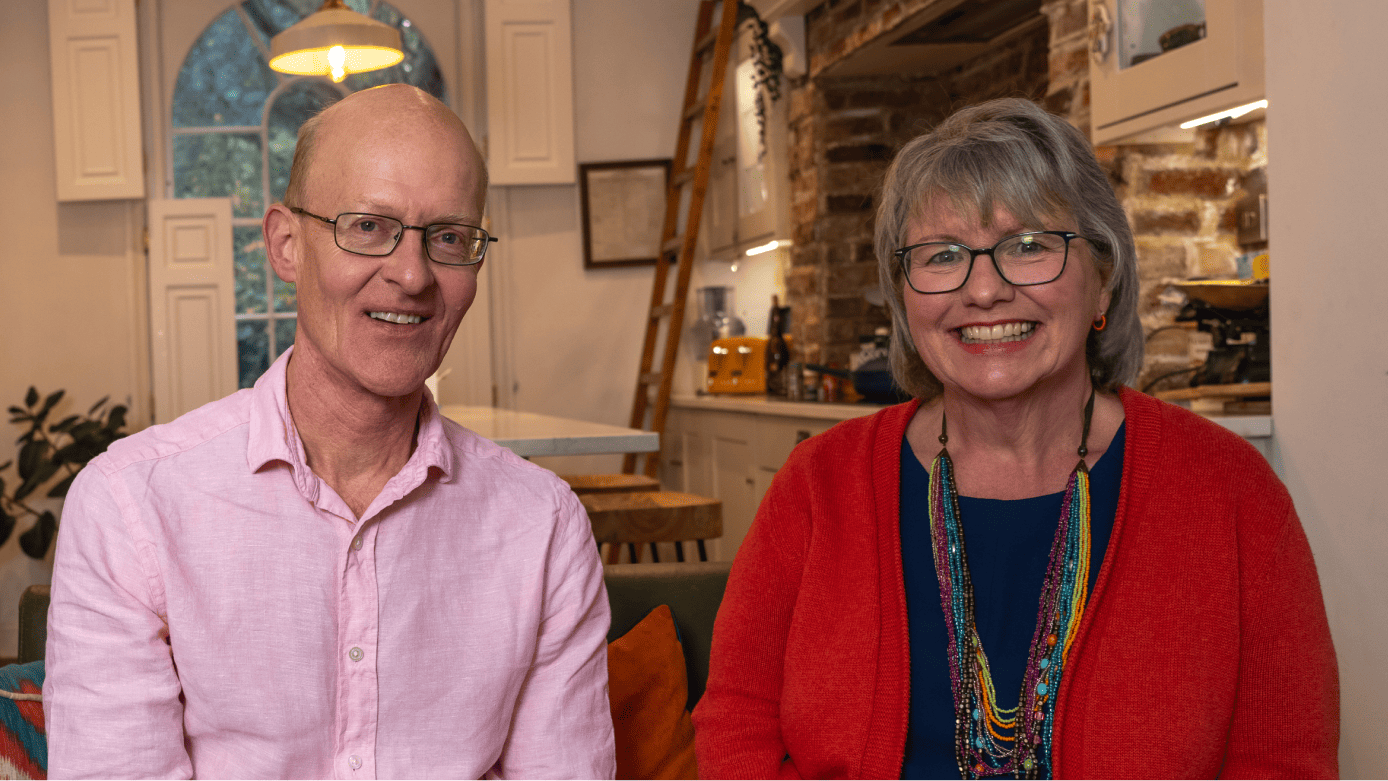

Monika and Lionel have the clarity they need

Monika and Lionel were anxious about the state of their pensions. They felt they couldn’t plan their future. Now they’ve both switched to ii and have the clarity they were always looking for.

“Since moving to ii – eye-opening. Clarity, power, decision, service and the app is fantastic. It’s good to know that if I need to talk to someone, people are there. It’s freedom. That’s why we’re with ii.”

Claire can see all her investments in one place

After Claire’s circumstances changed, she began looking to transfer her pension from her previous provider, Prudential. She already had an ISA with ii, so to her, switching was a no-brainer. After a straightforward transfer, she’d gladly recommend ii.

“My ISAs and now my pension – my SIPP – are all with ii. The ease in which I deal with my finances all in one place... it’s night and day. That’s why I’m with ii.”

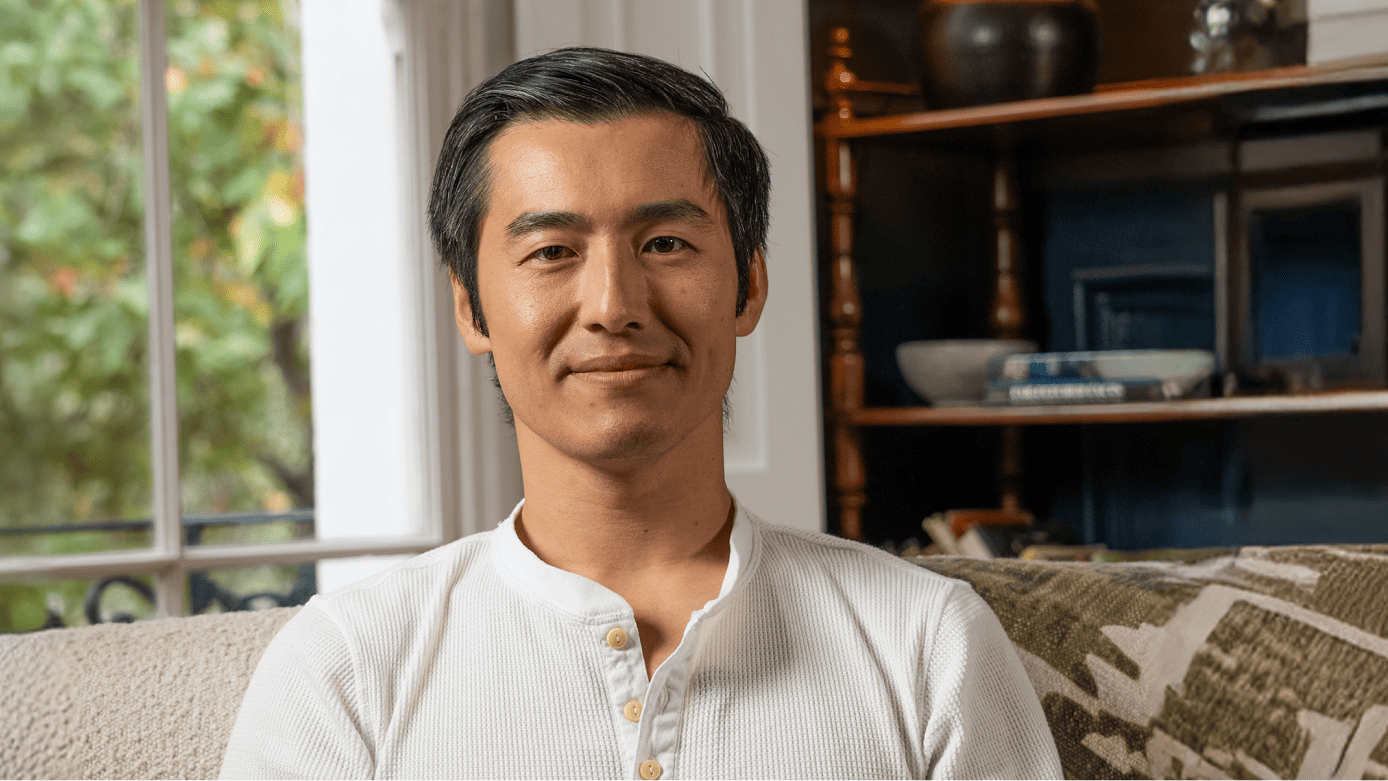

Even more stories from ii investors

Jerome

“The transfer process was really easy. You trigger the process and it all happens in the background. So it’s very smooth.”

Lisa

“The reason I chose ii for my SIPP was to consolidate everything. They have a flat-fee structure, so that was amazing. It’s very transparent.”

Bhupinder

“I had 2 pensions and thought ‘well let me put these all in one platform’. It’s great to have just one website to log in to, or one app to look at.”

Faisal

“Switching to ii was simple. I did my research, called up, and they explained their transfer system. The transfer took a couple weeks and I was kept up to date.”

Rhian & Julian

“When you ring up, you talk to real people who know what you’re talking about. And the ii website is rich in clear and compelling content.”

Bobby

“The investment options with ii are best in class. They let me make choices quickly and at a low cost.”

Mark

“Being really blunt, ii was just so much cheaper. With other platforms, it’s this plus that plus that. Whereas with ii, what I pay is what I pay.”

Five years straight and we’re topping the table

Another year as a Which? Recommended SIPP Provider. This year, our service and low-cost fees have landed us on top with an overall score of 83% and a fees score of 86%.

Put your pension in an award-winning, low-cost SIPP designed to go the distance.

Thinking about a Self-Invested Personal Pension?

Our free Essential Guide to SIPPs has everything you need to know to help you get started. It covers what a SIPP is, how it works and whether it’s right for you.