Italy crisis: Winners and losers

7th June 2018 09:33

by Graeme Evans from interactive investor

Markets regained some poise today, despite little sign that the threat of eurozone contagion from ongoing Italian political turmoil has gone away.

With Rome appearing closer to announcing yet another election this summer, the uncertainty sweeping European markets is likely to persist for some time yet.

The equities sell-off and a massive surge in Italian bond yields was triggered last week by fears that a coalition including the anti-establishment Five Star Movement will add to Italy's already huge debt burden. In response, the country's President Sergio Mattarella vetoed their choice of appointment for the economy ministry at the weekend.

That's increased the chances of another election in which support for Five Star and the far-right League could grow and result in a eurosceptic government.

Deutsche Bank said today: "If we do go to elections on July 29 or early August, much will depend on how the populists campaign on the topic of the Euro.

"In last month's election, leaving the euro didn't come up as an issue. This fear has only really emerged by concerns of a secret plan B to leave which underpinned the rejection of populist proposed finance minister Paolo Savona over the weekend.

"If the populists continue to stress their desire to stay within the euro then this goes back to being more about their spending plans and the slow burning clashes with the EU."

The yield on Italian government bonds surged to a four-year high above 3% in recent days, although a successful bond auction eased some of the jitters today and meant European stock markets were trading in positive territory.

Fabrizio Quirighetti, CIO and Co-Head of Multi-Asset at SYZ Asset Management, said the way markets had behaved in recent days pointed to a mood of crisis.

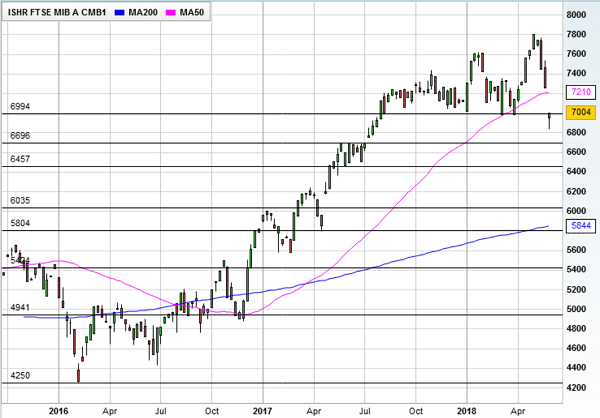

iShares FTSE MIB Ucits ETF EUR (ACC)iShares FTSE MIB ETF EUR Acc GBP

Source: interactive investor Past performance is not a guide to future performance

He said: "The markets are reacting normally for a crisis, with safe-havens including German bunds, US treasuries, USD, CHF and JPY flying higher, while equities and credit are under pressure, especially if related more or less directly to Italy and Europe."

However, Quirighetti pointed out that the surge in other peripheral yields such as Spain or Portugal looked to be overdone as European institutions now have tools to contain the contagion risks from Italy to other countries.

Finncap analyst Jeremy Grime said the extent of the current Germany/Italy bond spread put Italy's place in the currency union in doubt, ultimately bringing about the end of the euro.

He noted that around 13% of Italian debt is owned by insurance companies and pension funds with the main holders of non-resident debt being France and Luxembourg followed by Germany and Spain. Following this is the US, UK, China and Japan, largely held by funds.

The volatility sent gold prices spiking to 8-month highs in sterling terms and 11-month highs in euro terms, according to BullionVault.

Adrian Ash, its director of research, said: "While more active investors are using gold's volatility to trade in and out for profit, private investors look far too calm about the growing risks to shares, bonds and currency."

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.