How to make £10,000 from investment trusts in 2019

For the fourth year on the spin, our £10k income portfolio has delivered the goods. Here's how.

15th February 2019 15:02

by Helen Pridham from interactive investor

For the fourth year on the spin, our £10k income portfolio has delivered the goods. Here's how.

Most people who want to generate income from their capital, particularly in retirement, like to know they can rely on that income. Many shy away from the stock market for this reason. However, that is because they tend to focus on share price volatility rather than looking at the much steadier trajectory of share dividends. One of the best ways to tap into a steady flow of share dividends is through investment trusts.

A very important objective for many investment trusts is to provide investors with increasing income year after year, and another is to achieve capital growth over the long term. Investment trusts are particularly well-placed to deliver their income objective because, unlike investment funds (OEICS) and unit trusts, investment companies are allowed to hold up to 15% of their annual income in reserve to support their dividends in tougher times. Funds, on the other hand, are obliged to pay out all the income they receive each year.

This is not just a theoretical advantage for investment companies. More than 40 investment trusts have raised their dividends for 10 consecutive years or more, including four that have done so for more than 50 years.

Another weapon trusts have in their armoury is the ability to dip into their capital gains to boost dividends. The attraction of this for income investors is that it means they can benefit from growth-oriented trusts without having to cash in shares themselves to boost their income. The potential downside is the possibility of some capital erosion in a period of prolonged market falls; but investors only have modest exposure to such strategies, and boards are able to use their discretion, so the risks are limited.

Recipe for income

There are plenty of trusts to choose from if you want regular income. To cater for increasing demand, there has even been a growing trend among investment companies towards paying dividends quarterly. Half of all conventional investment trusts now pay quarterly dividends, up from 43% in 2016, according to the Association of Investment Companies.

So much choice can be bewildering, but the limit on how much you have to invest may narrow your choice. A small investor could be well-served with one global equity income trust. However, investors with larger sums are better off spreading their risk across a range of trusts run by different managers.

To help investors achieve their aims, we put together a portfolio of trusts each year to demonstrate how an annual income of £10,000 can be achieved, based on current yields. However, it is important to be aware that such a portfolio is not without risk. We don't promise that it will achieve its objectives. It is also important that investors only consider such a portfolio if they have a medium- to long-term investment perspective.

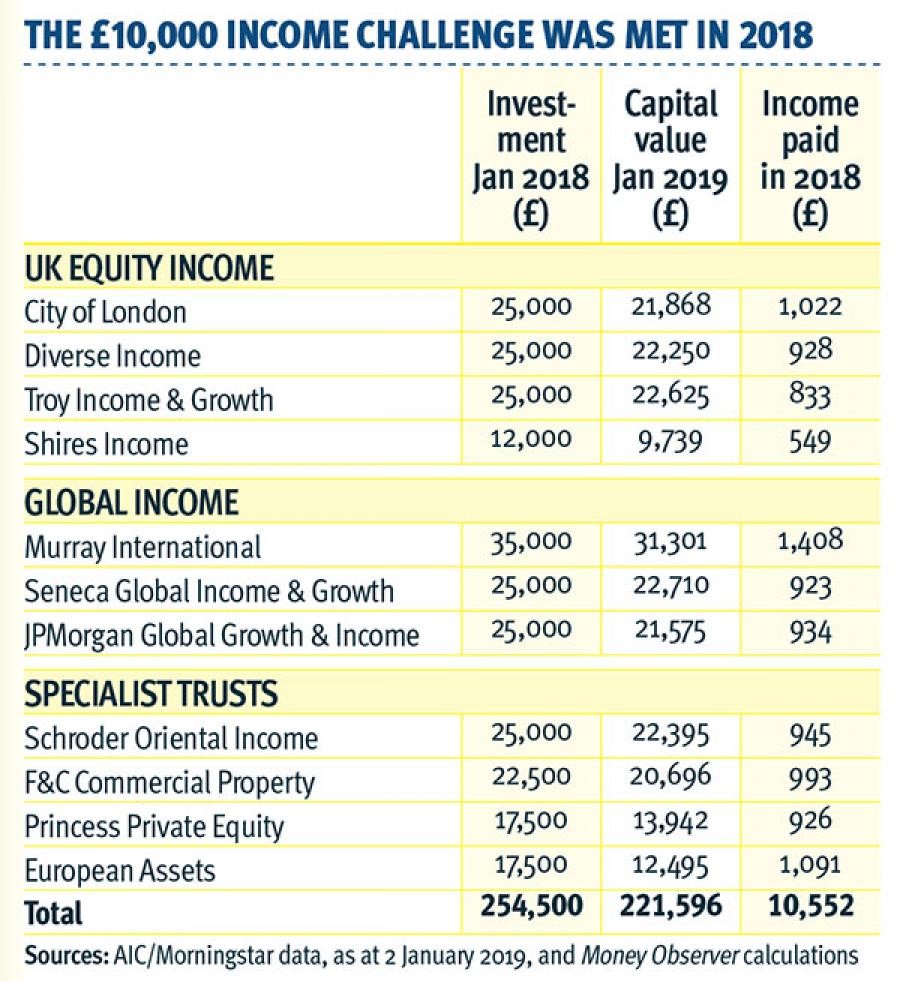

To date our exercise has shown the ability of trusts to deliver reliable income even when capital values are ¬fluctuating. Since the start of the project in 2015, the annual income produced by our portfolio has been above target every year. However, capital movements have been less predictable. In 2015 the capital value fell by 4.6%, but in the following two years it grew by 15.9% in the first year and by 8.4% in the second. In 2018 the portfolio produced 4.8% more income than we predicted, but lost 13% of its capital value.

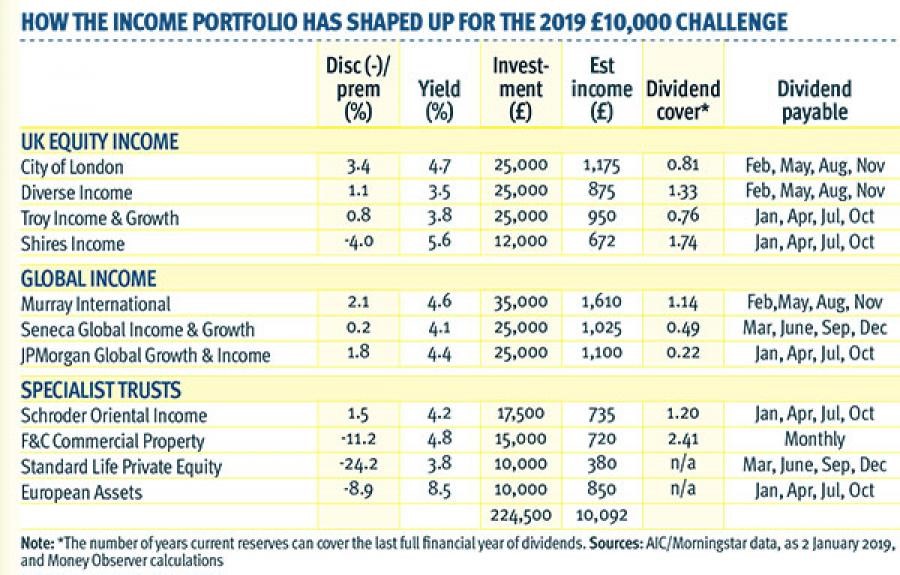

Each year we rebase the portfolio to make it relevant for new investors. The good news this year for new investors is that the amount required to achieve a £10,000 income has fallen to £224,500 (compared with £254,500 a year ago) due to lower share prices, which have in turn pushed up yields. With just one exception, we have maintained the same holdings as last year.

UK exposure matters

The foundation of the portfolio is four UK equity income trusts that together account for nearly 40% of the total. Although the Brexit impasse makes the outlook for the UK economy uncertain, it is important for income investors to keep a reasonable level of exposure to their home market to avoid taking on too much currency risk.

Over the past year, all four holdings paid out more income than we had estimated, but all four lost ground in capital terms. We have held City of London (LSE:CLIG) and Troy Income & Growth (LSE:TIGT) since this exercise started. City of London has the distinction of being the trust with the longest record of paying out consecutive annual dividend increases. This year it will celebrate its 53rd year of higher dividends.

The trust, managed by Job Curtis for the past 27 years, focuses on large blue-chip firms, many of which have seen their overseas earnings boosted by the weakness in the pound since the 2016 Brexit referendum.

The managers of Troy Income & Growth have a risk-averse approach and also invest in large, high-quality companies. It has proved the most resilient of the UK holdings, having fallen in value by less than 10% over the course of 2018.

The trust that paid out the biggest increase in income compared with our estimate was Diverse Income (LSE:DIVI). It paid out 20% more, partly due to a special dividend payment. It has a strong bias toward small- and mid-cap equities, but its managers focus on companies with strong cash ¬flows and improving productivity to help them maintain an increasing dividend.

Shires Income (LSE:SHRS), the smallest of our UK holdings, saw its price fall by 19%, but it has a good long-term record. There was a change of investment manager during the year, but there was no change to the trust's investment objective or process. We feel this trust is worth holding onto, as it is somewhat different from its peers: its high yield is boosted by the fact that it is around a quarter invested in fixed-income securities, mainly preference shares.

Global search for income

The importance of investing globally for income has been increasingly recognised in recent years. It gives investors increased diversification, particularly given that UK dividends are concentrated in a handful of sectors, including tobacco, pharmaceuticals and oil producers as well as banks.

Our portfolio includes three global trusts with an income focus. All three holdings delivered slightly more income than we expected for 2018. However, all saw their capital values fall. The most resilient in this respect was Seneca Global Income & Growth (LSE:SIGT), which was down just 9%, helped by its ¬flexible mandate, which allows it to invest in both overseas and UK equities, and a range of other as set types, including fixed income, as well as specialist areas such as infrastructure.

The other two holdings, JPMorgan Global Growth & Income (LSE:JPGI) and Murray International (LSE:MYI), have good longer-term records and were winner and runner-up respectively in the global income category in Money Observer's 2018 Investment Trust Awards. Both have high overseas exposures. The JPMorgan trust focuses on larger companies, and its largest regional weightings are to North America and Europe. Murray International has raised its dividend every year since 2004. It has significant exposure to Asia ex Japan and Latin America, whereas North America, Europe and the UK account for just over a third of the portfolio, a notably lower exposure than most other global trusts have.

Specialist switch

Our four specialist trust holdings also help give the portfolio a more global spread. In income terms, all four delivered, with F&C Commercial Property (LSE:FCPT) and Princess Private Equity (LSE:PEY) producing dividends that matched our expectations closely, while Schroder Oriental Income (LSE:SOI) paid out 5% more. European Assets (LSE:EAT), which supports its high yield using a mixture of capital and income, paid out 15% more income than we had expected.

However, specialist trusts can be more volatile, and as a result this part of our portfolio produced both the best and worst performances in capital terms in 2018.

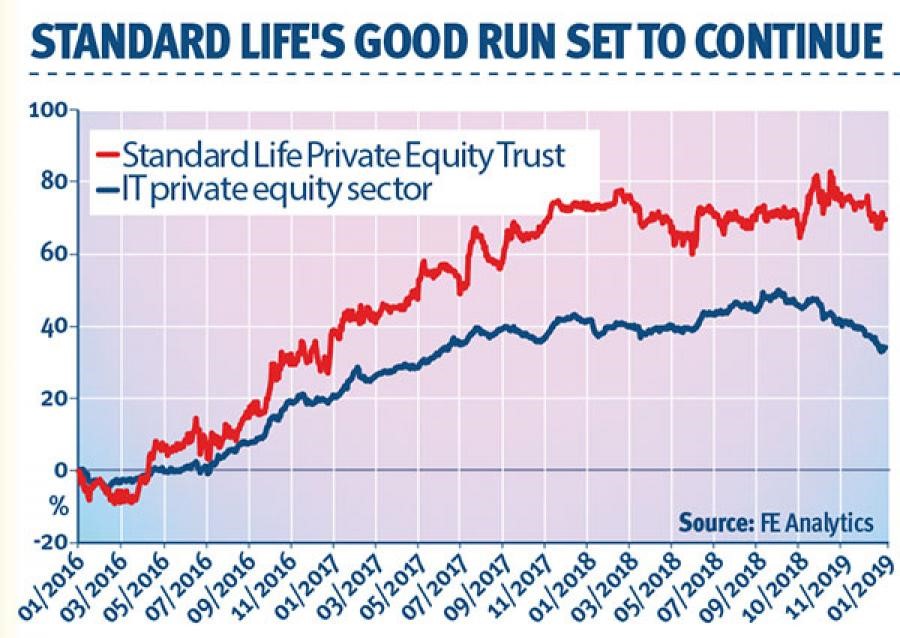

F&C Commercial Property was the portfolio's overall best performer in capital terms, losing ‘just' 8% of its value, while European Assets suffered the greatest fall, of 29%. This was exacerbated by its share price having gone from a 1.1% premium to net asset value to a 9% discount. Nevertheless, we have decided to retain European Assets. We still find European smaller companies an attractive area to invest in and believe manager Sam Cosh will do a good job. We have decided to drop our holding in Princess Private Equity this year and switch into to Standard Life Private Equity (LSE:SLPE) instead. This trust has lower charges and also pays a quarterly dividend. It has raised its dividends by 20% a year over the past five years. It was highly commended in Money Observer's 2018 Investment Trust Awards.

Money Observer's Private Equity Trust Choice switched for 2019

Exiting the portfolio:Princess Private Equity (LSE:PEY)

This trust has been included in the portfolio since inception and has served us well. It invests in private equity holdings globally, with around half its portfolio in Europe and a third in the US. Its main focus is on direct investment in small- and medium-cap buyouts.

While we still believe this trust is well run by its parent company, Partners Group, we decided it was time to refresh this part of our income portfolio. One reason for selling the trust is that its dividends, taken from capital, have remained fairly static, but another is its high ongoing charge, currently 2.6%, which includes a performance fee.

Entering the portfolio:Standard Life Private Equity (LSE:SLPE)

Standard Life Private Equity has a high-quality portfolio run by an experienced team. It has been focused on Europe, which its managers still believe is an attractive area for private equity investment, but in 2017 it was decided that it should look for opportunities further afield and it is now 15% invested in the US.

It invests principally in a selection of private equity funds, but the board has recently concluded that it would be beneficial to broaden its investment objective and policy to allow it to make its own direct investments – its target is 20% of net assets by 2023. We believe this gives the trust greater potential.

For income investors, the trust also has the attraction that it pays a quarterly dividend – an attractive yield of 3.8% – out of income. It has increased its dividends in recent years and the board says it is committed to maintaining their real value. Its ongoing charge is 1.14%. There is no performance fee.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.