When will Terry Smith’s Fundsmith Emerging Equities Trust find its FEET?

Performance at the trust has underwhelmed. Tom Bailey explains how the two new managers plan to revamp t…

13th February 2020 10:03

by Tom Bailey from interactive investor

Performance at the trust has underwhelmed. Tom Bailey explains how the two new managers plan to revamp the portfolio.

Terry Smith is one of the UK’s most well-known fund managers. His open-ended Fundsmith Equity fund has been a blinding success, returning 132% over the past five years. Last year his company launched a new trust, Smithson; while not managed by Smith, it aims to take the Fundsmith investment philosophy and apply it to global smaller companies. The trust’s launch was the largest ever in UK investment trust history, raising £822 million.

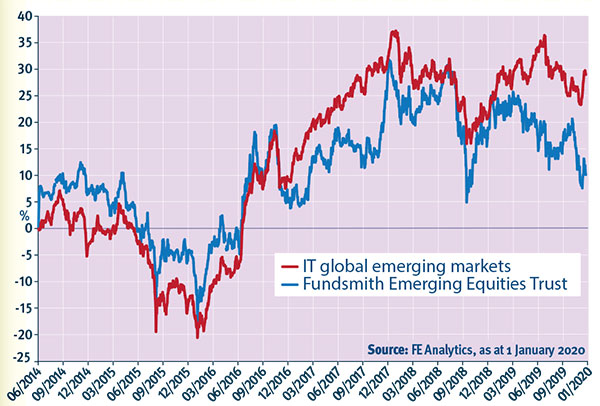

Less successful, however, has been Terry Smith’s emerging market venture, Fundsmith Emerging Equities Trust (FEET). The trust was launched at the end of June 2014, raising £193 million. Since then (as the graph below shows) it has broadly lagged the emerging market index, returning just 10.2% in share price terms to the end of 2019. In comparison, over that period the Association of Investment Companies’ global emerging markets sector returned 29%.

- Specialist investment trust choices for 2020: hidden gems

- 11 investment trusts for a £10,000 annual income

- Global fund and trust tips for 2020: growth and income options

- Regional fund and trust tips for 2020: the hunt for great returns

Last May, however, Smith announced he would be stepping back from the day-to-day running of the trust. Leadership has been handed to Michael O’Brien and Sandip Patodia as portfolio manager and assistant portfolio manager, respectively. Smith still provides advice to the two managers in his role as chief investment officer.

In light of this change, we take a look under the bonnet of FEET. We speak to its new lead manager, Michael O’Brien, to get a better insight into the trust’s approach to emerging markets and what potential changes the new managers may oversee.

Fundsmith emerging equities lags behind

Wide divergence

FEET has a relatively unusual approach to emerging market investing. As a result, the portfolio barely resembles most emerging market trusts or open-ended funds. FEET also diverges widely from emerging market indices.

“The approach [of the trust] is to invest in good businesses that have exposure to the rise of the consumer in emerging economies,” says O’Brien. It’s a theme that many emerging market investors pay lip service to FEET, however, has gone all in: consumer staple companies represent just over 60% of the trust’s portfolio. In contrast, the MSCI Emerging and Frontier Market index (FEET’s benchmark) has a weighting to the sector of just 6.3%.

Meanwhile, the trust is underweight several of the region’s most prominent sectors. For example, financials are the largest sector in the MSCI Emerging and Frontier Market index, with a weighting of 25%. FEET has no financials in its portfolio. Also avoided are cyclical sectors such as construction and manufacturing and resources.

Technology and communication services stocks are also largely absent from the portfolio, each accounting for just over 3%. In contrast, information technology is 15.4% of the trust’s benchmark index and communication services has a weighting of 11%.

This is largely due to Smith’s dislike of China’s tech giants such as Alibaba, Tencent and Baidu – companies to which other emerging market funds are heavily weighted. Smith has long voiced his scepticism of the country’s investment climate, previously arguing: “The problem is the government can simply take your property away.”

However, more specifically, O’Brien says Chinese tech companies are avoided “given their financial and governance track record on capital allocation, ownership rights and/or the reliance on their relationship with the Chinese government”.

All of this makes for a wide divergence from the MSCI Emerging Market and Frontier index in terms of regional allocation. For example, the index has a weighting towards China of over 33%, while FEET’s is just 4.6%.

Those holdings the trust does have in China are in keeping with the play on consumer growth. For example, the trust’s third-largest holding is Chinese sauce manufacturer Foshan Haitian.

Big country bet

The emphasis on consumer staple companies has seen FEET build up a portfolio that is heavily overweight India. The subcontinent accounts for over 41.4% of the portfolio but just 8.5% of the index. According to O’Brien: “India is the single-largest repository of companies of the type and quality we seek, and we believe that it has commenced upon a long period of sustained and inclusive economic growth driven by the reforms of Prime Minister Modi’s government.”

Some of FEET’s largest holdings are Indian consumer-facing companies. For example, Godrej Consumer Products, which makes and sells soap, hair colourants, toiletries and liquid detergents, is a top 10 position. The trust also has large holdings in Hindustan Unilever and Nestlé India.

The trust also has a large position in Egypt, a country not usually holding a prominent place in emerging market portfolios and one that makes up only a small part of emerging and frontier indices. This large weighting is the result of the trust’s holding in Eastern Tobacco, an Egyptian tobacco manufacturer.

Absent from the line-up are Taiwan and South Korea, which collectively account for over 20% of the trust’s benchmark. O’Brien says: “We have historically not invested in Taiwan and South Korea, as we view them as developed in terms of bothGDP per capita and demographic trends.”

How rival trusts compare

| Share price total return (%) | |||

|---|---|---|---|

| Investment trust | One year | Three years | Five years |

| Aberdeen Emerging Markets | 20 | 28 | 54 |

| Aberdeen Frontier Markets | 1 | -21 | -8 |

| BlackRock Frontiers | 4 | 17 | 48 |

| Fundsmith Emerging Equities | -7 | 4 | 3 |

| Genesis Emg Mkts | 27 | 39 | 61 |

| JPM Emg Mkts | 26 | 61 | 91 |

| Mobius Investment Trust | -9 | n/a | n/a |

| Templeton Emg Mkts | 27 | 50 | 69 |

| Utilico Emerging Markets | 20 | 36 | 53 |

| Average | 12 | 27 | 46 |

Note: Data to 2 January 2020. Source: Winterflood

On the same path

Smith’s decision to step back from the running of the trust is unlikely to spark any fundamental change in this approach to emerging market investing, orientated around the rise of emerging markets consumers and companies.

However, there are likely to be some changes to the trust’s portfolio in the near future. First of all, O’Brien notes, the trust will holder fewer companies than it has in the past. He says: “The number of shares in the trust currently stands at 36, a low for the fund. We expect the number of holdings to stay at the lower end of the 35-55 range we said we would normally hold when we launched it.”

The sort of shares it holds might also see a change. O’Brien says: “We expect that FEET will increase its exposure to related sectors such as healthcare and technology that are providing services to consumers, as such opportunities become available.” This is not so much a divergence from the trust’s original thesis of playing the rise of emerging market consumers as a recognition of the growing wealth and sophistication of such consumers.

The trust has already been increasing its exposure to healthcare, with the sector going from zero at launch to around 16% today.

However, the trust will also see some divergence from the consumer focus. According to O’Brien: “Eventually we may also seek some exposure to companies which gain competitive advantages from operating from emerging economies but which do not earn the majority of their revenues in those economies.”An example of this would be Indian IT services businesses which, says O’Brien, benefits from an attractively priced and skilled labour pool.

What the experts think

According to Priyesh Parmar, an investment trust analyst at Numis, a key feature of FEET is the companies it holds that trade at a notable valuation premium versus the market. This is a reflection of the sort of high-quality companies that the management team favours. Right now, notes Parmar, the trust is trading on a discount, as has been the case since the news of Smith “stepping back”. Previously, since launch in June 2014 the trust had typically traded at a premium, despite its underperformance. Parmar says: “A period of relative outperformance may be required before the discount narrows.”

Ben Yearsley, a director at Shore Financial Planning, generally takes a negative view of the trust. He says: “I didn’t like the trust when it launched, as I felt that whilst Smith was doing a great job with Fundsmith Equity, this wouldn’t necessarily translate to an emerging markets franchise.” Yearsley says the new managers at the helm will not change his view and argues that there are many other “high-quality existing funds and trusts to choose from”.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.