The Ian Cowie portfolio: bargain trusts and big yields

Our columnist finds cheap, high-yielding trusts exposed to the biggest consequence of the pandemic.

21st May 2020 09:11

by Ian Cowie from interactive investor

In his latest weekly column for interactive investor, Ian finds high-yielding bargains exposed to the biggest and most long-lasting of all the consequences of the coronavirus crisis.

Here is how investors, who fear they have left it too late to log onto the online shopping boom, can catch up with an investment trust yielding 6% and trading at a double-digit discount.

Ignore the red-hot technology sector, where the typical trust is now priced at a premium to net asset value (NAV), and consider instead funds exposed to a fundamental requirement of internet retail; warehouses or ‘big box’ storage and distribution sites.

Everyone can see how the coronavirus is hurting the high street. But fewer investors are following how many of those consumers’ pounds and euros are being diverted into 'clicks and mortar’ logistical operations on the edge of town.

It might be worth taking a closer look. For example, Aberdeen Standard European Logistics (LSE:ASLI) (stock market ticker: ASLI) reports “unprecedented demand” from online food and pharmaceutical companies among the tenants of its 14 warehouses across five continental countries. Everything you buy on the internet has to be stored somewhere before it is delivered to your door.

While shares in Polar Capital Technology (LSE:PCT), a more obvious way into digital retail, have soared by 39% over the last year, ASLI shares have slumped by 9.8% over the same period, according to independent statisticians Morningstar. One share seems pricey; the other looks cheap.

Both shares are in my ‘forever fund’ and I am jolly glad I have held PCT for more than a decade. But ASLI - in which I invested at flotation in December 2017 - may offer better value for contrarian buyers today, with its shares trading nearly 13% below NAV.

Source: TradingView. Past performance is not a guide to future performance.

Fund manager Evert Castelein explained: “While some of our tenants are experiencing short term operational and financial challenges, a good proportion of our tenants are experiencing greatly increased levels of trading as demand for home delivery and essential logistics have risen sharply.

“Three of our top four tenants by income operate in the food and pharmaceutical sectors and they are experiencing unprecedented levels of trading volume. While the Covid-19 pandemic creates significant short-term market disruption, the forced lockdown and reduced social mobility for the foreseeable future will inevitably lead to an accelerated take up of e-commerce in European countries.”

Against all that, ASLI’s share price has been dragged down by aversion to the property sector in general as fears rise of tenancy voids and rental holidays being demanded by distressed retailers. Those fears should not be underplayed because, although all of ASLI’s first-quarter rents were paid on time, a third remained unpaid at the end of April.

- Gold boom: prices and prospects by Petropavlovsk

- Dividend hunt: where the big payouts will likely be in 2020

- COMING SOON: More fund manager videos and gold analysis

Castelein claimed:

“Following the conclusion of rent deferral discussions, the level of payments for the second quarter is expected to materially increase as tenants fulfil their payment obligations.”

While shareholders wait to see how many of those ‘cheques in the post’ actually arrive and are honoured, ASLI can point to outperformance over the last difficult year both in terms of total returns and dividend yield. It’s closest rival, Tritax EuroBox (LSE:BOXE), has shrunk shareholders’ capital by 19% and yields 3.9% to trade on a discount of 22%. The comparable figures for ASLI are a loss of 9.8%, a yield of 6% and a 13% discount.

Meanwhile, the average for the Association of Investment Companies Property: Europe sector is a capital loss of nearly 18%, a yield of 4.3% and a discount of 25%. The explanation is that conventional property trusts are depressed by exposure to depopulated office, manufacturing and retail assets.

For example, Schroder European Real Estate (LSE:SERE) has shrunk shareholders’ capital by an eye-watering 38% over the last year, to trade at an eye-stretching 41% discount to NAV. Bargain-seeking income investors might be tempted by its 9.8% dividend yield but they will need to be brave.

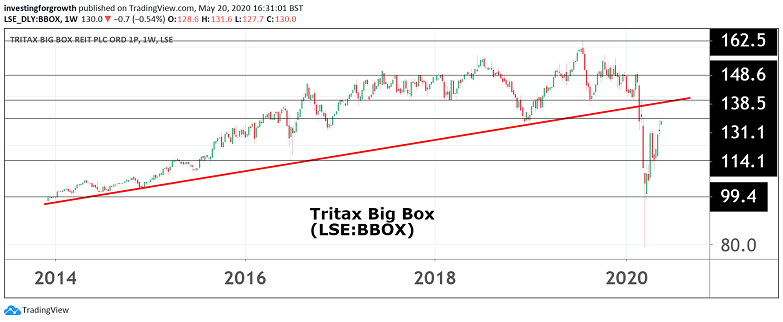

Closer to home, in the Property: UK Commercial sector, Tritax Big Box (LSE:BBOX) is the daddy of them all with total assets of nearly £3.7 billion, compared to £218 million at ASLI, €477 million at BOXE and £163 million at SERE.

But size is no guarantee of safety for shareholders and BBOX has shrunk their capital by 8.1% over the last year, to trade at a 13% discount to NAV with a 5.4% yield. As its name suggests, this trust also focuses on warehouses and gives indirect exposure to the trend toward shopping online.

Source: TradingView. Past performance is not a guide to future performance.

From a financial point of view, this looks likely to be the biggest and most long-lasting of all the consequences of the coronavirus crisis. Many folk of all ages, who had formerly shunned shopping online, have been given a crash course in internet retail by the coronavirus and may remain converts forever.

Spending half of Saturday at the supermarket or shopping mall might soon seem as quaint as 1950s consumers traipsing up and down the high street, popping into the butcher, the greengrocer and the off-licence. That view is in the share price at PCT, but it certainly is not at ASLI, BBOX or BOXE.

Ian Cowie owns shares in ASLI and PCT as part of a diversified portfolio of global equities. Other trusts mentioned: BBOX, BOXE and SERE.

Ian Cowie is a freelance contributor and not a direct employee of interactive investor.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.