ii investment performance review: Q2 2022

14th July 2022 11:21

Surging inflation and Russia's war in Ukraine unnerved investors as the rotation out of growth-oriented sectors towards value stocks gathered pace.

Market round-up

Investment markets continued to keep investors on their toes throughout the second quarter of the year as volatility and uncertainty remained high. For just the second time in 40 years, both stocks and bonds posted losses for two consecutive quarters as inflation and policy responses from central banks, government and organisations like OPEC continued to shape economic data and market movements.

Whilst perhaps not as front-and-centre in the news as was the case in the first quarter, the war in Ukraine rages on and the consequential impact on energy prices threatens a range of outcomes from a tightening of belts to a severe economic downturn across Western Europe.

- Invest with ii: Top UK Shares | Share Prices Today | Investing in Bonds

Central banks have begun raising interest rates in all developed markets, except for Japan, as inflation reaches levels not seen for a number of decades. Despite this, the labour market remains tight, with some reports in the US suggesting there are twice as many vacancies as there are people looking for jobs. Covid cases have once again started to rise with an estimated 1 in 15 people in the UK having the virus at points over the quarter, but this data barely registers anymore, as market focus has shifted to the rapidly rising cost of living and the costs of inputs for businesses.

Investors are trying to determine who has the pricing power to survive inflation and the staying power to survive a recession, something that seems more and more inevitable as each day passes.

Shares

US, and, as a result, global equities have slipped into bear markets (20% decline) in base currencies, although, due to the pound being weak, in sterling terms losses have not been as severe.

The UK was once again the strongest performing developed market posting more subdued losses than other countries, and also seeing a wide dispersion of returns, with large caps again outperforming and the FTSE 250 finishing the quarter almost 7.5% behind the FTSE 100.

This was a phenomenon that continued across the globe as small-cap stocks, which generally have growth biases and are more economically sensitive, were the worst performers in each region, once again except Japan given the risk of stagflation.

The US was the worst-performing developed market, with growthy tech names continuing to sell off, and Europe also fared poorly against the backdrop of economic disruption over gas pipelines and the impact of a possible recession on exporters like Germany. Emerging markets delivered strong performance for the quarter relative to other regions, driven exclusively by China, which posted double digit gains and carried the Emerging Market Index to much smaller losses than the US and Europe, despite losses in India, Korea and Taiwan, as investors bet that the worst of the lockdown-induced economic shock and the tech sector crackdown in the country, had passed.

| Performance (%) | Q2 | YTD | 1 Year | 3 Years | 5 Years |

| China | 12.12 | -1.03 | -22.41 | 1.00 | 3.52 |

| Russia | 8.42 | -100.00 | -100.00 | -98.89 | -92.61 |

| Asia Pacific Ex Japan | -3.04 | -5.93 | -12.80 | 3.72 | 4.69 |

| FTSE 100 | -3.74 | -0.97 | 5.76 | 2.46 | 3.50 |

| Emerging Markets | -4.00 | -8.13 | -15.01 | 2.15 | 3.56 |

| FTSE All Share | -5.04 | -4.57 | 1.64 | 2.41 | 3.32 |

| India | -6.38 | -5.48 | 8.29 | 8.97 | 8.71 |

| TOPIX Japan | -6.68 | -9.98 | -8.38 | 2.46 | 2.88 |

| Europe Ex UK | -8.65 | -15.41 | -10.57 | 2.88 | 3.53 |

| S&P 500 | -9.04 | -10.73 | 1.68 | 12.34 | 12.82 |

| World | -9.13 | -11.34 | -2.56 | 8.68 | 9.13 |

| FTSE Small Cap | -9.48 | -15.12 | -12.56 | 6.73 | 5.23 |

| FTSE 250 | -10.98 | -19.40 | -14.59 | 0.86 | 1.76 |

| Brazil | -18.04 | 14.60 | -12.75 | -7.76 | 2.17 |

Source: Morningstar. Total returns in GBP. | |||||

Sectors

For the most part the themes of the first quarter persisted, with more growth orientated sectors underperforming those that exhibit a value bias. Energy remained the top performing sector globally as oil and gas prices continued to rise, and, as a result, the profitability of associated companies rose too, although these companies saw a pull-back at the end of the quarter. Related to that, utilities companies performed strongly given the rising prices.

Tobacco, pharmaceuticals and healthcare all proved their economic resilience by posting relatively strong performance. At the other end of the scale tech stocks had another challenged quarter, as is to be expected given the lofty multiples they have been trading at, these multiples continued to compress against the rates and inflation background. Interestingly mining stocks were some of the worst performing, as many commodities came under pressure as the global economic outlook continued to worsen.

| Performance (%) | Q2 | YTD | 1 Years | 3 Years | 5 Years |

| Energy | 2.86 | 38.25 | 49.24 | 7.26 | 6.77 |

| Consumer Staples | 1.47 | 0.64 | 10.31 | 7.13 | 6.43 |

| Health Care | 0.61 | 0.02 | 11.18 | 12.80 | 11.23 |

| Utilities | 0.33 | 4.57 | 17.41 | 7.09 | 8.12 |

| Real Estate | -7.53 | -10.42 | 0.68 | 2.76 | 5.17 |

| Financials | -9.14 | -7.98 | -0.57 | 5.42 | 4.93 |

| Industrials | -9.64 | -12.83 | -7.61 | 4.38 | 5.69 |

| Communication Services | -12.61 | -19.52 | -19.55 | 5.17 | 5.61 |

| Materials | -12.89 | -8.03 | -1.94 | 8.21 | 8.16 |

| Information Technology | -15.20 | -21.63 | -8.20 | 17.02 | 18.82 |

| Consumer Discretionary | -17.36 | -24.03 | -17.10 | 7.20 | 9.33 |

| Source: Morningstar. Total returns in GBP. | |||||

Bonds

Investors looking to take shelter from falling equity markets were unable to do so in the traditional refuge of bonds. Investors in some types of bonds felt more pain than other markets, with over 15-year Index-Linked gilts down 25% for the quarter, and the broader Index-Linked Gilt market down 17.5%. These bonds have some of the longest durations, so rising interest rates have really had an impact.

UK investors buying overseas bonds fared much better however, with short-term US Treasuries returning over 7% in sterling terms, although many investors are likely to hedge their fixed income exposure. The conventional UK gilt market fell around 7.5% compared to around 4.5% for global treasuries, as the structurally longer duration of gilts again caused them to sell off in the rising rate environment, whereas in the US investors are coming round to the idea that the Fed will begin to cut rates in 2023 as a looming recession bites.

Corporate bonds fared slightly better than gilts in the UK but slightly worse than treasuries in the global market, as recession fears caused some global investors to opt for the safety of government bonds which supported their prices, whereas future earnings fears weighed on corporate debt and, as a result, high yield bonds performed even worse. Interestingly within investment grade credit, AAA bonds (the highest quality), were the worst performing as they face the possibility of ratings downgrades in tough economic times.

| Performance (%) | Q2 | YTD | 1 Year | 3 Years | 5 Years |

| Global Aggregate | -0.54 | -3.99 | -3.59 | -1.69 | 0.79 |

| Global Government | -0.71 | -3.99 | -3.97 | -2.30 | 0.46 |

| Global Corporate | -0.84 | -5.66 | -4.98 | -0.75 | 1.58 |

| Global High Yield | -3.94 | -7.12 | -6.30 | -0.27 | 2.14 |

| EURO Corporate | -5.73 | -10.20 | -12.70 | -4.80 | -1.41 |

| Sterling Corporate | -6.66 | -12.41 | -12.90 | -1.89 | 0.16 |

| Global Inflation Linked | -6.75 | -8.31 | -3.37 | 0.47 | 2.07 |

| UK Gilts | -7.42 | -14.06 | -13.60 | -3.43 | -0.75 |

| UK Inflation Linked | -18.17 | -22.80 | -17.33 | -4.21 | -0.51 |

| Source: Morningstar. Total returns in GBP. | |||||

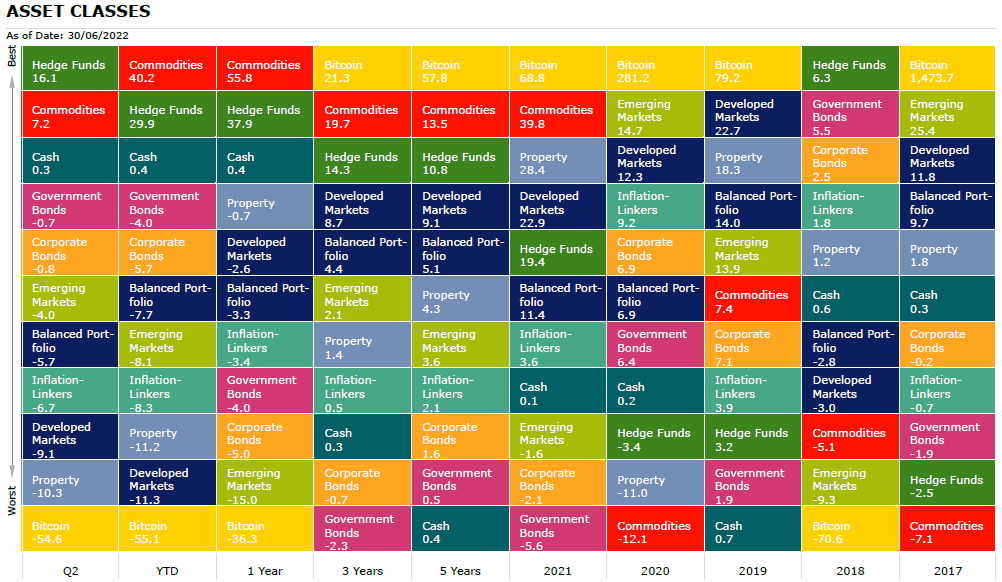

Commodities and Alternatives

Despite the inflation levels we are seeing, it is perhaps unusual to see such a wide dispersion in commodity movements, as whilst energy and grains continued to perform strongly in the second quarter, precious metals and especially base metals suffered falls over the quarter and are flat/negative for the year depending on the metal and the currency of trade.

Oil and gas both went higher over the quarter, with gas nearly doubling by the first week of June, as uncertainty around European access to Russian gas and an explosion at a US liquified natural gas plant, cut supply. However, some of these gains were given back towards the end of the quarter as the US was able to bring more production online and commit to getting the Freeport plant back in action. Copper, often seen as an economic bellwether, fell almost 30% over the quarter in USD terms, as recession fears loomed.

Interestingly, however, direct property remained solid, especially in the UK where the asset class delivered modest positive returns. Sales of commercial properties were often at the top or above expected ranges and, in the UK residential market, although house building is beginning to slow, prices remain at record highs.

| Performance (%) | Q2 | YTD | 1 Year | 3 Years | 5 Years |

| CBOE Market Volatility (VIX) | 51.39 | 85.94 | 106.30 | 25.88 | 22.40 |

| Hedge Funds | 16.09 | 29.89 | 37.89 | 14.27 | 10.80 |

| Brent Crude Oil | 15.35 | 64.62 | 73.83 | 21.82 | 20.71 |

| Commodity | 7.22 | 40.22 | 55.78 | 19.68 | 13.48 |

| Gold | 2.19 | 11.13 | 17.36 | 10.38 | 9.31 |

| Global Infrastructure | 0.37 | 10.96 | 20.12 | 5.12 | 6.25 |

| Cash | 0.26 | 0.39 | 0.42 | 0.34 | 0.44 |

| Global Natural Resources | -8.46 | 10.00 | 17.11 | 10.28 | 10.39 |

| UK REITs | -17.03 | -19.15 | -5.86 | 1.61 | 1.52 |

| Source: Morningstar. Total returns in GBP. | |||||

Most-traded shares on the ii platform in Q2 2022

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.