Adding two funds that rise as stocks fall

Saltydog Investor has bought two bond funds for its portfolios, arguing the outlook has changed for the sector

20th August 2024 08:50

by Douglas Chadwick from ii contributor

This content is provided by Saltydog Investor. It is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

There used to be a fairly clear relationship between the performance of bonds and equities. When bond prices rose, equity prices tended to fall, and vice versa.

Under normal market conditions, bond prices move inversely to interest rates, at least in the short-term. It has got more to do with mathematics than market sentiment. When interest rates rise, existing bonds with lower yields become less attractive, so their prices fall. This brings their returns in line with the new bonds currently being issued. Conversely, when rates drop, bond prices rise.

- Invest with ii: How Bonds & Gilts work | What is a Managed ISA? | Buy Bonds

Equities, or stocks, should also benefit when interest rates fall. Lower interest rates reduce borrowing costs for companies, making it cheaper for them to finance expansion, invest in new projects, and manage existing debt. This can lead to higher corporate profits, which generally boosts stock prices.

At the same time, when interest rates are low, the returns on bonds and other fixed-income investments decrease, making equities more attractive to investors seeking higher returns. This shift in investor preference towards equities can further drive up stock prices.

However, this dynamic does not take into account the intervention of central banks, who can deliberately upset the equilibrium.

- Bond Watch: why inflation rise is nothing to worry about

- Bond Watch: ii unlocks access to UK Treasury Bills

Back in the 1980s, the market adage “don’t fight the Fed”, first started gaining traction. Investors had come to realise the power of the central banks. Whether you agreed with their policies or not, and regardless of underlying economic conditions, it was usually better to be on their side, rather than fighting against them.

In the last financial crisis, we saw several large financial institutions rescued by the taxpayer, because they were seen as ‘too big to fail’ … remember Fannie May and Freddie Mac in the US, and the Royal Bank of Scotland, Lloyds Bank, and Northern Rock in the UK. They probably captured most of the headlines, but AIG, Citigroup, Bank of America, Merrill Lynch, Wells Fargo, Morgan Stanley, Goldman Sachs, and Barclays, along with others, also got a helping hand.

The central banks are slightly different … they are ‘too important to fail’. It is hard to imagine a situation where any government would allow its central bank to fail. If push came to shove, it would just force through the relevant legislation to change the rules.

Following the Global Financial Crisis of 2008-2009, central banks around the world, particularly the US Federal Reserve, implemented unprecedented monetary policies, including maintaining ultra-low interest rates and engaging in large-scale asset purchases (quantitative easing).

The prolonged period of low interest rates diminished the yield on bonds, making them less attractive. This forced investors to seek higher returns in equities, even during times of uncertainty. However, the central banks were still busy buying bonds providing artificial support. The global economy ended up in a position where both asset classes went up in tandem, with the key driver being central bank policy.

- DIY Investor Diary: why I’m ‘all in’ on this volatile gilt

- Is inflation beaten? The impact on stocks and bonds explained

So, is that the new status quo? We don’t think so. Over the last couple of years, inflation has risen dramatically and so central banks have been increasing interest rates to try and bring it down. That has put pressure on households and businesses as they have had to deal with higher costs. It has been painful, but effective, at least in terms of bringing down inflation. The Bank of England has already reduced our interest rates and it looks as though the Federal Reserve will soon follow suit. However, it’s unlikely that rates are going to drop to anywhere near where they were for most of the last 15 years. The central banks are also keen to offload the assets that they have accumulated after more than ten years of quantitative easing.

We could now be heading back into a situation where the old inverse relationship between equities and bonds is restored. We have certainly seen that in the last few weeks.

Equity markets did not have a great start to August and some of the falls were quite brutal. A few weeks ago, no one was predicting that the Japanese Nikkei 225 would go down by more than 12% in one day.

Although there was quite a strong recovery last week. Most of the key stock market indices that we track are still showing month-to-date losses. The FTSE 100, which is often more resilient than most when markets crash, still ended last week down 0.7% so far this month, while the FTSE 250 had lost 2.6%.

Over the channel, the Paris CAC 40 was down 1.1% and the Frankfurt DAX had fallen by 1%.

The situation was a bit more mixed in the US. The Nasdaq, which initially suffered the largest fall, bounced back and went into the weekend 0.2% ahead of where it was at the end of last month, the S&P was up 0.6%, but the Dow Jones Industrial Average was still down 0.4%.

In Asia, the Shanghai Composite was down 2%, the Indian Sensex was down 1.6%, and the Nikkei 225, despite a remarkable comeback, had still lost 2.7% during the course of this month.

- Benstead on Bonds: stock market wobble shows why we own bonds

- How professional investors reacted to market turbulence

Last week, when we reviewed our latest fund analysis, most sectors were showing four-week losses, particularly those with exposure to the equity markets. This was not surprising, considering that most stock markets had also been falling.

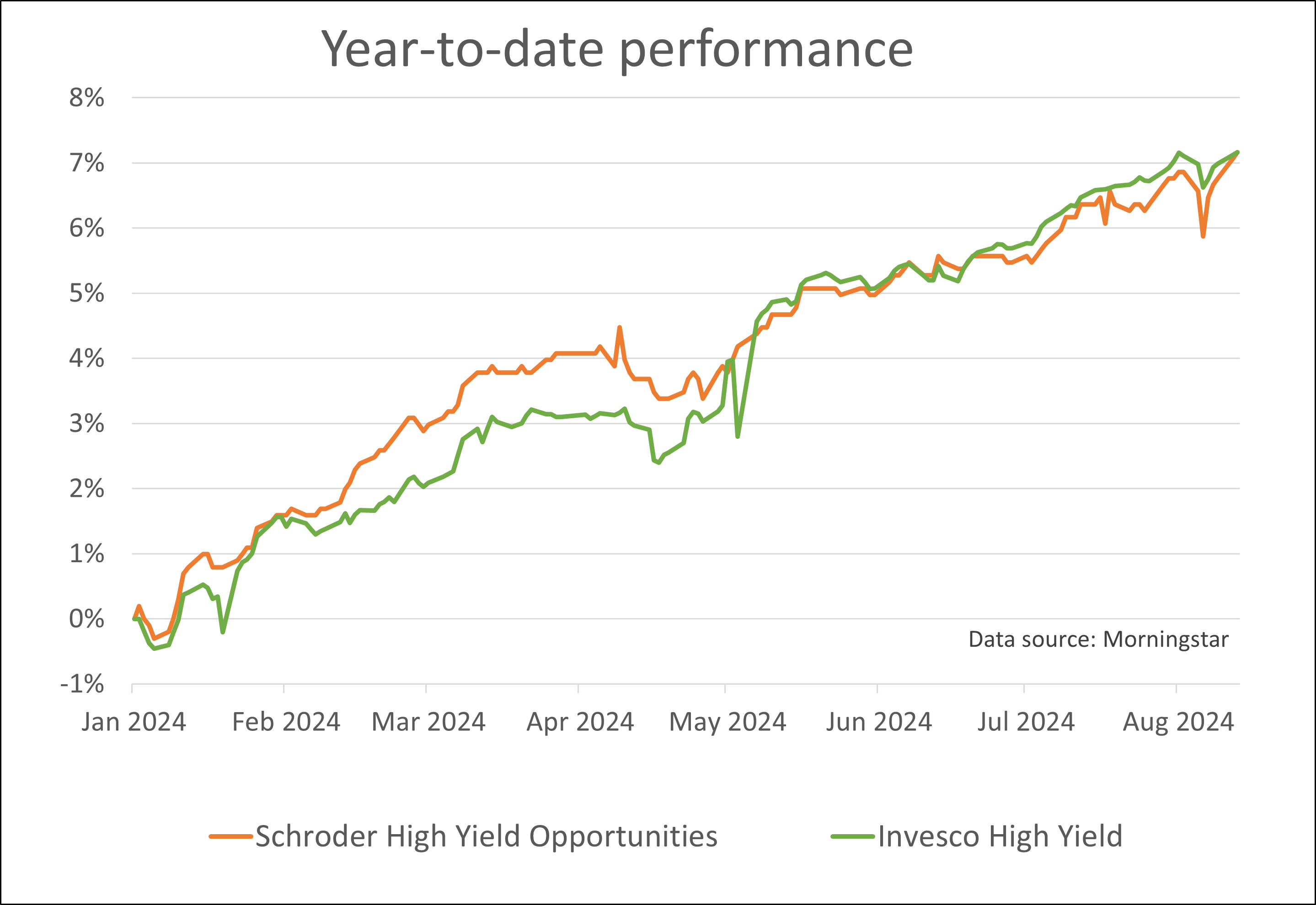

However, the sectors that were still showing gains were the ones investing in bonds and gilts. Funds from these sectors may not perform as well as the ones investing in equities when the markets are thriving, but they tend to be less volatile and can still provide reasonable returns. That is why we invested in two funds from the £ High Yield sector in September of last year. They both had a Saltydog "vindex" ranking of 1, making them some of the least volatile funds in our analysis, and yet they were doing better than the money market funds.

This graph shows how they had done so far this year.

They had both gone up by around 7% in just over seven months. There had been some ups and downs along the way, but their overall trajectory has been much smoother than we would expect to see in the funds exposed to the equity markets.

In our latest reports, only three out of the six sectors in our 'Slow Ahead' Group were showing gains over four weeks. They were £ High Yield, up 0.7%, £ Corporate Bonds, up 1%, and £ Strategic Bonds, up 1.3%.

- Funds light on ‘Magnificent Seven’ that have delivered top returns

- Is inflation beaten? The impact on stocks and bonds explained

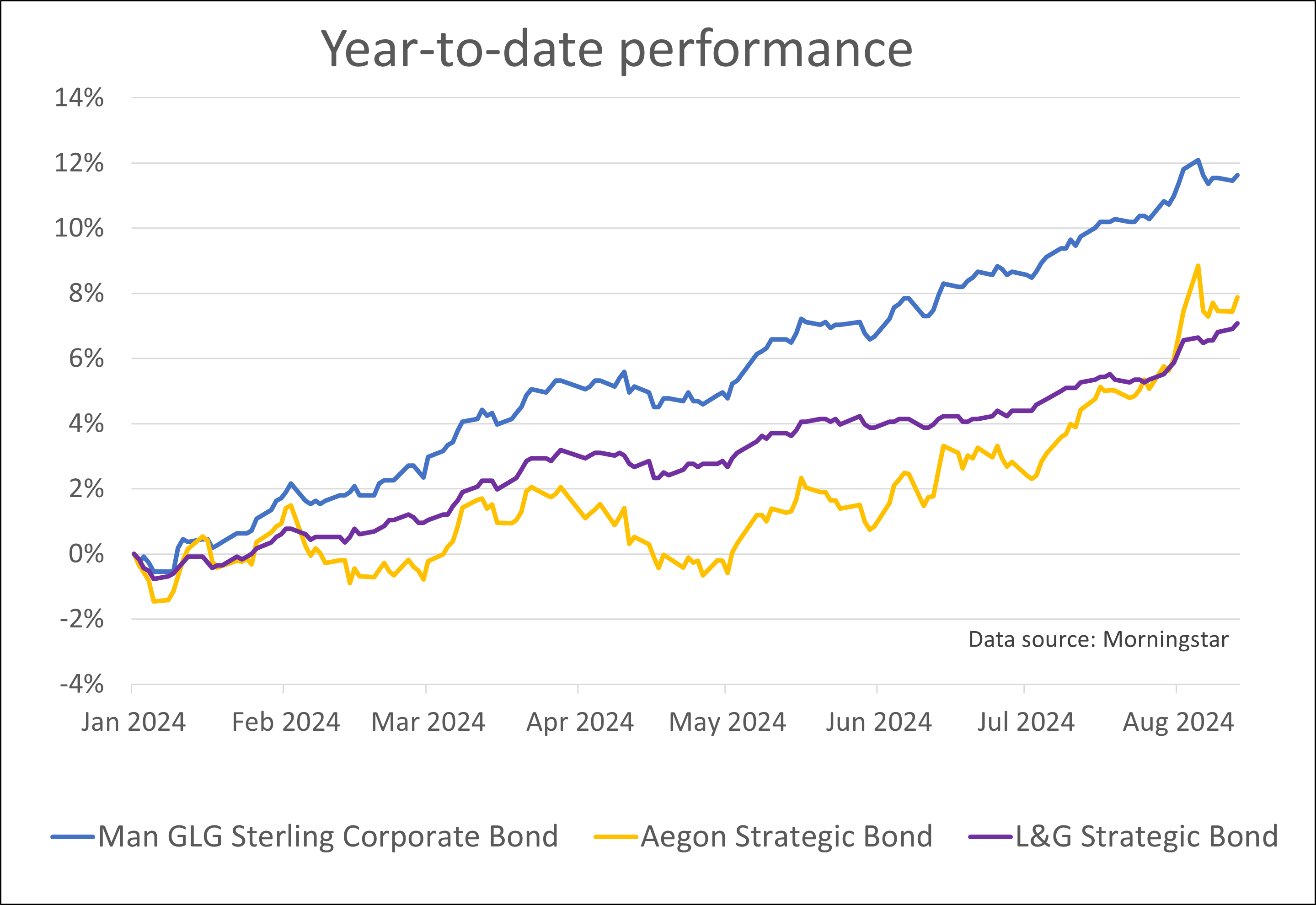

We had a look at the leading funds in these sectors and found three that have been in decile one over four, twelve, and twenty-six weeks. They were the Man GLG Sterling Corporate Bond fund, from the £ Corporate Bond sector, and the Aegon Strategic Bond and Legal & General Strategic Bond funds, both from the £ Strategic Bond sector.

Over the last twelve weeks, the Aegon Strategic bond was in vindex 2 and the other two funds were in vindex 1.

This was how they had done so far this year.

The Aegon Strategic bond had been the most volatile. The other two had been making pretty steady progress and generating much better returns than the money market funds. Over the same period, the Royal Money Short Term Money Market and L&G Cash funds had only gone up by around 3%, but they are less risky.

Last week our Ocean Liner portfolio invested in the Man GLG Sterling Corporate Bond fund and the Tugboat portfolio invested in the Legal & General Strategic Bond fund.

For more information about Saltydog, or to take the 2-month free trial, go to www.saltydoginvestor.com

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.