Two Brexit share tips and an 11.6% dividend yield

18th October 2018 14:23

by Graeme Evans from interactive investor

These stocks have seen their valuation de-rated but earnings quality remain high or improve. Graeme Evans talks us through the 'buy' case.

The task of picking quality stocks suitable for Brexit Britain appears to be getting harder with every day that passes without an agreement with the EU.

While the Brexit narrative of relatively cheap UK domestic stocks is now well understood, there are still many tail risks posed by the type of EU settlement and resulting impact on the UK economy, currency markets and interest rates.

These were magnified in dramatic fashion by this week's warning that France's 'no-deal' planning involved a scenario where Britons would need visas to enter the country or hold permits in order to work there.

To find a partial offset to these tail risks, a note by UBS analysts has sought to identify UK focused businesses where the stockmarket valuation has de-rated but the earnings quality has remained high or is moving up.

Their focus landed on two stocks in particular, 'buy'-rated Howden Joinery and Taylor Wimpey.

The pair have seen their price earnings (PE) multiples drop by 28% and 32% respectively between 2016 and their 2019 calendar year projection. This is offset by growth of 17% and 22% in earnings per share (EPS).

Similar stocks with a PE fall greater than the UK median include 'buy'-rated Pennon Group and Derwent London. There's also Auto Trader, Shaftesbury and St James's Place, on which UBS has 'neutral' recommendations for all three.

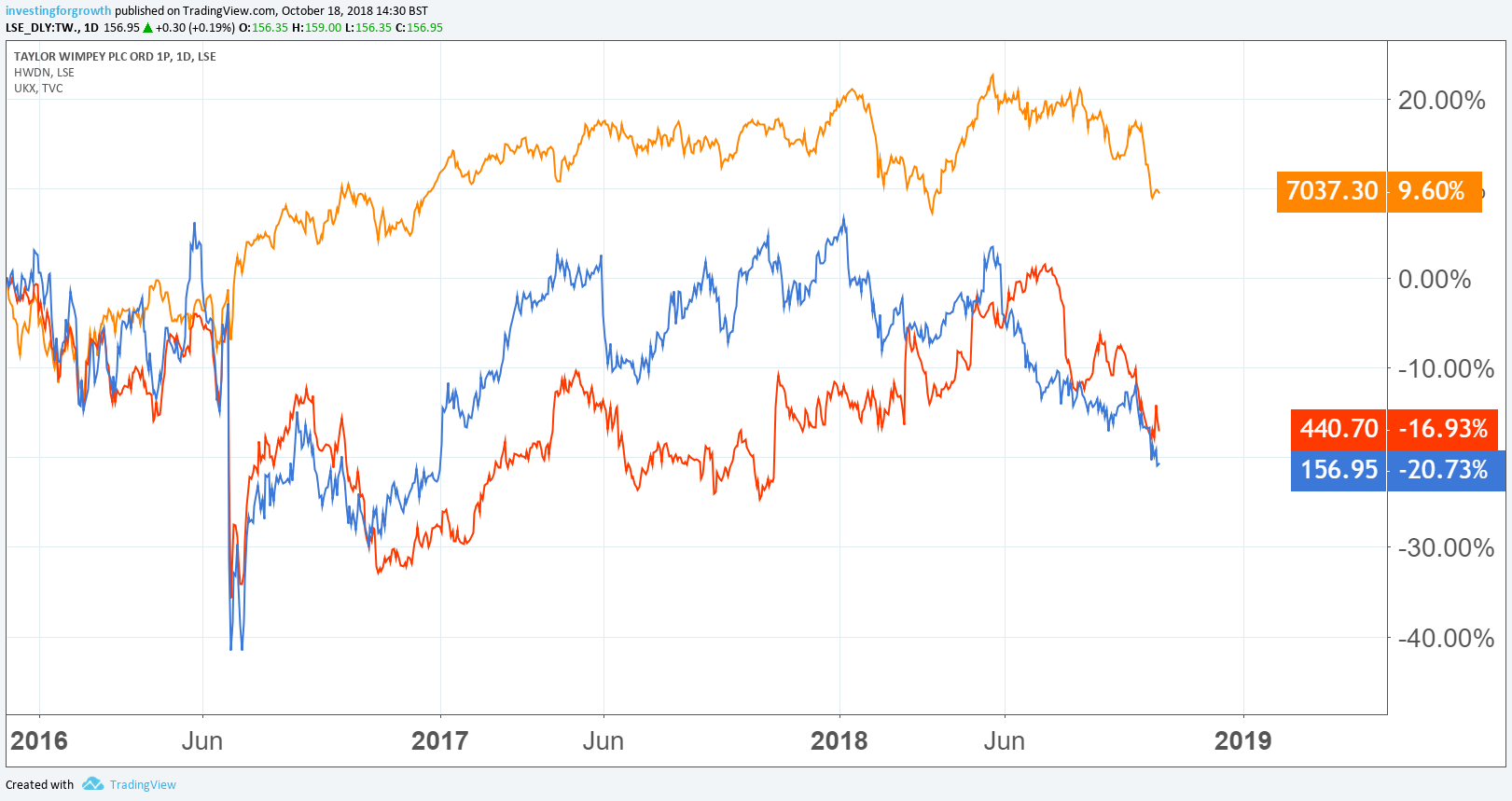

Source: TradingView (FTSE 100, orange; Taylor Wimpey, blue; Howden Joinery, red) Past performance is not a guide to future performance

In the case of Howden, UBS analyst Heidi Richardson points to the kitchen supplier's "high quality medium-term roll out story".

She added: "Near-term demand is uncertain but we see Howden as able to continue to outperform end market weakness. We see continued medium term upside potential from new depot openings, depot maturity, and price rises."

Cash generation is strong, and Richardson says this could result in further cash returns in the coming years.

Meanwhile, UBS analyst Gregor Kuglitsch thinks that Taylor Wimpey offers an attractive way to play the new build sector.

He said: "We think returns will be stable on high levels, despite some policy risk around potential changes to Help to Buy or Brexit, and be supportive of material dividends to shareholders."

UBS forecasts point to the shares offering a 2019 dividend yield of 11.6% and trading on a projected PE of 6.2x. Kuglitsch added: "We expect the group to remain in a net cash position, mitigating financial risk."

The Brexit note from UBS also screens London-listed stocks that have an international rather than domestic focus. The aim is to highlight those companies with falling quality metrics in the period between 2016 and 2018 but with a PE increase greater than the median.

UBS highlights two 'sell' recommendations in the form of Aggreko, where the EPS is down 15% but the PE is up 7%, and Meggitt following a 38% rise in the PE and 6% improvement in EPS.

On Aggreko, UBS says that the competitive advantage previously enjoyed by the temporary power supplier has been eroded in markets that remain weak.

This suggests continued downside to profits in the utility division, which is likely to outweigh a cyclical recovery in the rental and industrial divisions.

Meanwhile, UBS analyst Celine Fornaro is cautious about how Meggitt will fare in the civil aerospace parts market if rising oil prices increase the potential for a higher number of aircraft retirements.

Meggitt allayed some of these fears earlier this week when it posted an unscheduled trading update in which it upgraded revenue forecasts for the second time in four months. It has benefited from stronger demand among defence customers as well as in the civil aerospace aftermarket.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.