Compare SIPP charges

With pension charges, less means more.

See if you could pay less in pension charges. Compare what you’re paying now to a Self-Invested Personal Pension and discover whether you could save more for your retirement.

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). If you’re unsure if a SIPP is right for you, please speak to an authorised financial adviser. Tax treatment depends on your individual circumstances and may be subject to change in the future.

Explore if you could save with an ii Personal Pension

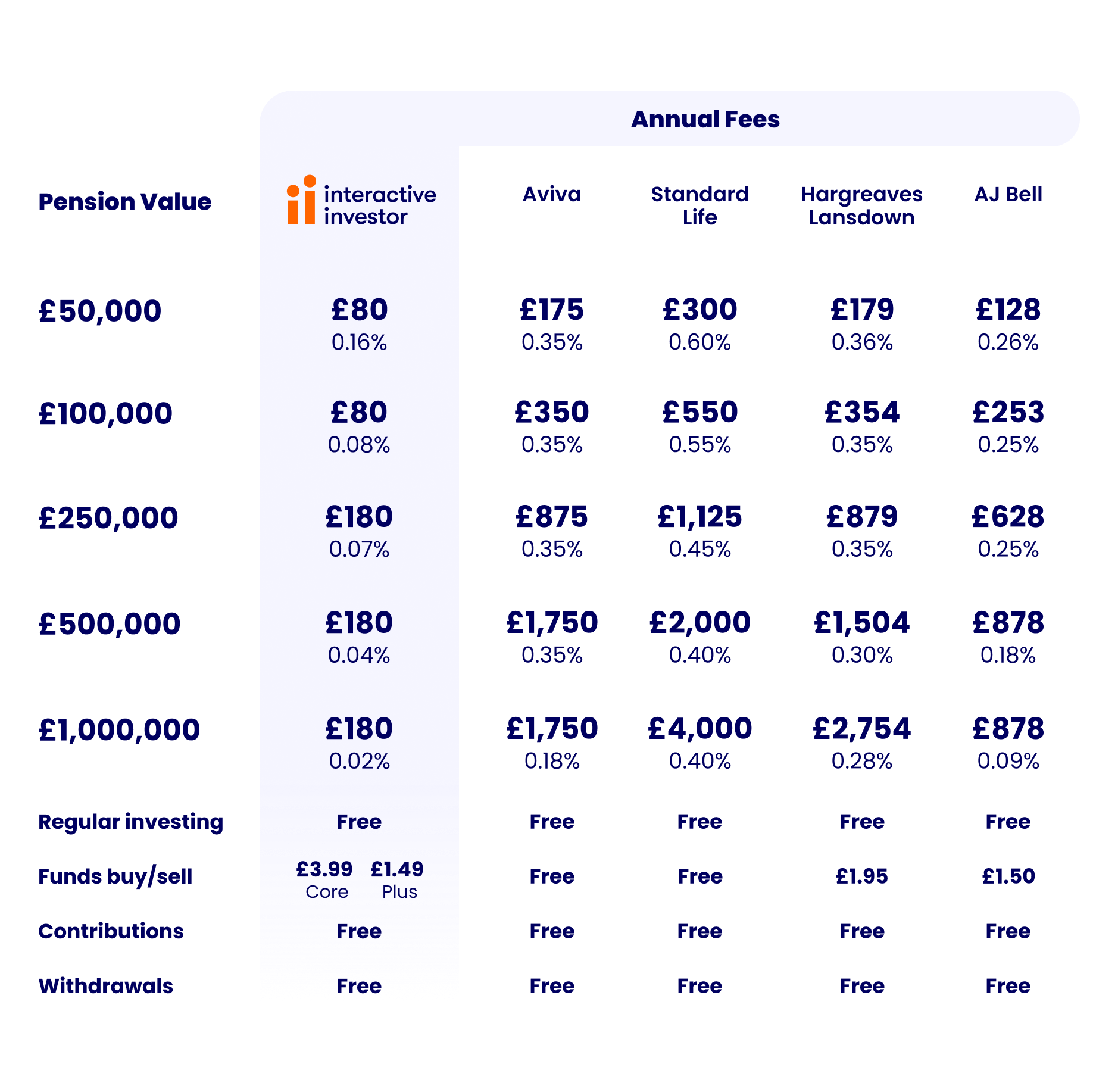

See how much you could save with our low, flat monthly fee Personal Pension compared to other SIPP providers that charge percentage-based fees.

Here's a look at our flat monthly fees:

- £5.99 a month for pensions up to £100,000

- £14.99 a month for pensions over £100,000

With ii, you will always pay a low flat fee - helping you keep more of your money invested for the future.

Comparison information - Annual charge comparisons based on published SIPP charges on 01/02/2026 for Aviva SIPP & Standard Life SIPP (Level 2 Investment Options). Hargreaves Lansdown SIPP charges based on new pricing plan effective 01/03/2026. The calculator compares SIPP charges only – other types of pensions may have lower or higher charges. For ii charges you'll start on our Core plan for £5.99 a month and move to our Plus plan for £14.99 a month if your account goes above £100,000. Verified as accurate by The Lang Cat.

Assumptions: 100% holding in funds - choosing other assets such as shares and ETFs, may result in lower charges. Two fund purchases/sales. Pension charges only, excludes fund manager charges. Read more about our analysis.

Are you in the dark about your pension charges?

According to the Financial Conduct Authority (FCA), almost a third of UK adults paying into a Defined Contribution pension don’t know how much they’re being charged. 55% of people don’t even realise they have charges.

You could be paying more than you need to. But it’s never too late to check your pension charges and see if another option – like a Self-Invested Personal Pension (SIPP) - could be right for you.

You might be surprised just how much lower your fees could be. And the more you save today, the more your pension can compound and grow.

How does the ii SIPP compare to other SIPP providers?

Choosing the right SIPP provider could mean thousands more pounds for your retirement. Dig deeper into how the ii SIPP compares to some of the other SIPPs on the market.

ii vs Hargreaves Lansdown

Compare the ii SIPP to Hargreaves Lansdown.

ii vs Aviva

Compare the ii SIPP to Aviva.

ii vs Standard Life

Compare the ii SIPP to Standard Life.

Investing in your pension made simple

The benefit of a SIPP is it allows you to decide how you want to invest for your retirement. But that doesn’t mean it has to be complicated.

There are plenty of options specially selected by experts to help you get started. These are designed to get you investing in your pension quickly, with a range of low-cost funds you can choose from based on the level of risk you’re comfortable with.

Summer’s brighter with our special offers

Summer’s in full swing - make it your time to invest with our latest special offer.

Open an ii Personal Pension (SIPP) and enjoy £100 to £3,000 cashback when you deposit or transfer a minimum of £20,000. See more details on this offer.

Offer ends 31 August 2026. New customers only. Terms and fees apply.

Important information: It’s important to take your time before transferring your pension. Make sure to consider what the best option is for you. Don’t transfer just to qualify for the offer, and don't rush any decision to meet the offer deadline. We periodically run offers, and there will likely be other opportunities in the future.

Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions.

See how Mark pays less for his pension with ii

“With a lot of providers’ charges, it’s this plus that plus that. Whereas with ii, it’s straightforward. What I pay is what I pay – ii’s fees are just so much cheaper. That’s why I’m with ii.”

Mark, 47, was frustrated with the fees he was paying with his old provider. With ii’s low flat fee, he now gets to retire earlier.

Keep more of what you make

Other providers usually charge a percentage of your pot. That means the more your pension grows, the more they’ll take. The ii SIPP is different. With our simple flat fee, you can keep more of what’s rightfully yours.

Which? Recommended SIPP Provider

As a Which? Recommended SIPP Provider for the fifth year running, we offer one of the widest ranges of investments on the market. That doesn’t mean more complexity, though. We have options for all types of investors.

Trust in our top-rated support

With our Boring Money Best For Customer Service support team here in the UK, you can count on us. There’s a reason we’re rated 4.6/5 on Trustpilot, with more 5-star reviews than two of the other biggest providers combined.

Flexible pension withdrawals with ii

At ii, there are no charges for taking an income from your pension. It’s all covered by your flat fee.

Enjoy the flexibility of withdrawing your money your way. Choose to take tax-free cash, drawdown or lump sums - all at no extra cost.

How can Pension Wise help?

If you’re thinking about retiring soon and want to understand your options, make sure you speak to someone at Pension Wise.

Pension Wise is part of the government’s Money Helper service, offering free and impartial pension guidance to the over-50s. They can also help you decide if transferring your pension is the right choice for you.

Thinking about a Self-Invested Personal Pension?

Our free Essential Guide to SIPPs has everything you need to know to help you get started. It covers what a SIPP is, how it works and whether it’s right for you.

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.