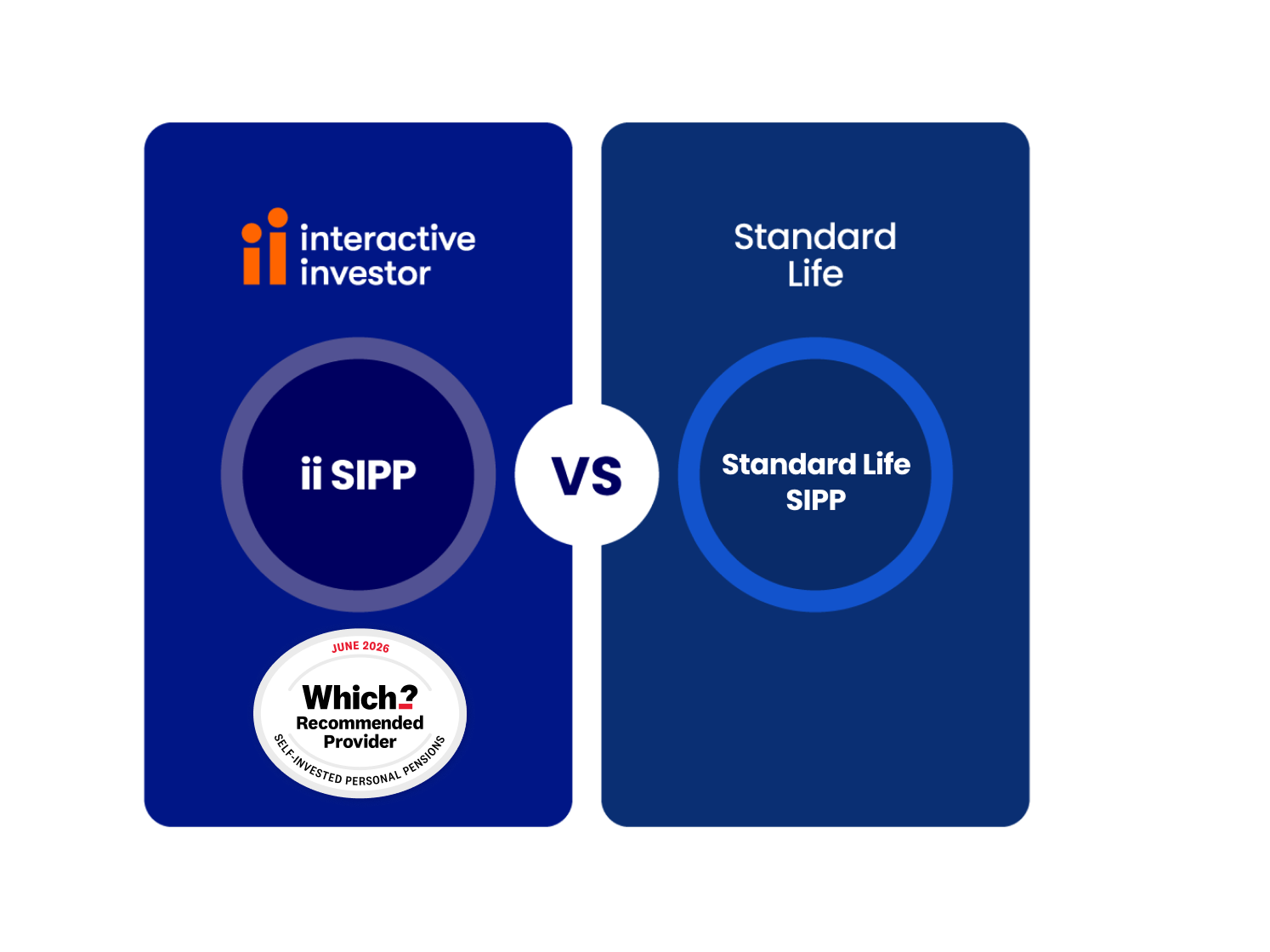

SIPPs compared: ii vs Standard Life

A personal pension that cuts costs, not choice

With a broad investment choice, ii’s Personal Pension (SIPP) is a low cost, flat fee alternative to Standard Life.

No narrowed fund lists. No rigid structures. Just a pension that lets you invest for your retirement your way.

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. Tax treatment depends on your individual circumstances and may be subject to change in the future. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

Flat fees vs percentage fees: why it matters

Standard Life pensions typically charge a percentage of your retirement pot. For smaller pensions, a percentage-based fee may seem low - but as your pension grows, so do your fees.

With ii’s flat fee, your costs stay low as your pension grows - so the larger your pot, the more you could save.

| Pension value | ii charges | Standard Life charges | Annual saving with ii |

|---|---|---|---|

| £50,000 | £80 0.16% | £300 0.6% | £220 |

| £100,000 | £80 0.08% | £550 0.55% | £470 |

| £250,000 | £180 0.07% | £1,125 0.35% | £945 |

| £500,000 | £180 0.03% | £2,000 0.4% | £1,820 |

| £1 million | £180 0.02% | £4,000 0.4% | £3,820 |

Charge comparison information: Annual charge comparisons based on published Standard Life SIPP charges on 01/02/2026. Assumptions: 100% holding in funds and two fund purchases/sales. Pension charges only, excludes fund manager charges. Based on Standard Life level 2 SIPP charges. Read more about our analysis. Verified as accurate by The Lang Cat.

Clear, simple, lower charges

With Standard Life’s percentage-based fees, the more you save, the more you pay.

At ii, we charge a low, flat monthly fee - giving you clear, predictable costs that won’t increase as your pension grows. Find out more about our charges and plans.

Wider investment choice

The ii Personal Pension offers a wide range of investment options, including many funds and shares that aren’t available to all Standard Life customers.

More choice doesn’t have to mean more complexity. Our Managed Portfolios or expert picks can do the hard work for you.

Trust in our top-rated support

Our UK‑based customer support team is here to help with everything from tracking transfers to adding cash to your pension

Whether you prefer to call or use secure messaging, you can speak to a knowledgeable team when you need support.

At a glance: ii Personal Pension vs Standard Life SIPP

Alongside our low, flat fee, investment choice and flexibility are often top of the list for people transferring their pensions from Standard Life to ii.

Use our table to compare key features to help find the right pension for you.

| ii Personal Pension (SIPP) | Standard Life SIPP | |

|---|---|---|

| Platform charge | Flat fee | Percentage of your portfolio |

| Which? Recommended | ✔ | ✘ |

| Whole of market investment range (including shares, funds, ETFs, investment trusts, bonds, IPOs and more) | ✔ | ✔ (Limited, some through advised SIPP only) |

| Managed pension investments | ✔ | ✔ |

| Free regular investing | ✔ | ✔ |

| Minimum monthly or yearly contributions | ✘ | ✔ (You need to make minimum payments to remain eligible for this SIPP) |

| Mobile app | ✔ | ✔ (Workplace pension only) |

| Free pension withdrawals | ✔ | ✔ (Free for level 1 and 2 only) |

| Flexible withdrawal options (includes flexi access drawdown or lump sum withdrawals) | ✔ | ✔ |

| UK based customer support | ✔ | ✔ |

Ways you can invest in an ii Personal Pension

Manage your own investments

- Build a diversified portfolio with shares, investment trusts, bonds and funds. Invest in UK favourites, like Lloyds and BP, or global names such as Apple and Tesla

- And while you manage your investments yourself, our expert insights are always there if you need them

- All plans enjoy free regular investing - a cost-effective way to build your pension

Leave it to the experts

- If you prefer a ready-made option, then our Managed Portfolios may be for you

- We’ll match you to an investment portfolio that reflects the risk level you’re comfortable with, then look after your investments for you

- Please note, our Managed Portfolios aim to grow your pension over the long term. That's why you'll need to be at least 5 years away from taking money out of your pension

It’s about making the right choice for you

The right choice depends on how you want to manage your pension, your pot size, and what fees you're comfortable with.

Transferring a pension to ii can be a good choice for many reasons. It can save you money, improve your investment options and give you greater flexibility with your retirement income.

But there are some important things to check and consider before you make your move.

Check 1: Will it cost you anything to transfer

It’s always free to transfer to ii from our side, and Standard Life don't usually charge exit fees or penalties.

Check 2: Will you lose any benefits by transferring?

Some pensions have protected benefits. Before transferring, make sure you won't lose any of the following:

- Guaranteed annuity rates

- Lower protected pension age

- Matching employer contributions

Check 3: Should you take pension advice before transferring?

If you’re unsure about transferring your pension(s), please speak to an authorised financial adviser who specialises in pensions. And if you’re over 50 and thinking about retiring soon, you can also book a free and impartial guidance session with Pension Wise, part of the government’s MoneyHelper service. They can help you understand your options and decide whether a transfer is right for you.

Have a question? Talk to our team

Call our award-winning UK-based Customer Support team on 0345 607 6001. You can reach one of our friendly SIPP specialists between 8am-4:30pm, Monday to Friday.

Why Bhupinder transferred from Standard Life to ii

By combining his pensions with ii, Bhupinder got clearer fees, more choice, and full control over his investments.

“I would recommend ii, because it’s got a very simple pricing structure and it has a really easy to use app.”

Your pension, in your pocket

Wherever you are, you can stay in control of your pension with the ii app.

- View all your ii accounts in one place.

- Add cash and invest in UK and international markets quickly, easily and securely.

- Make smarter investment decisions with exclusive research tools and expert insights.

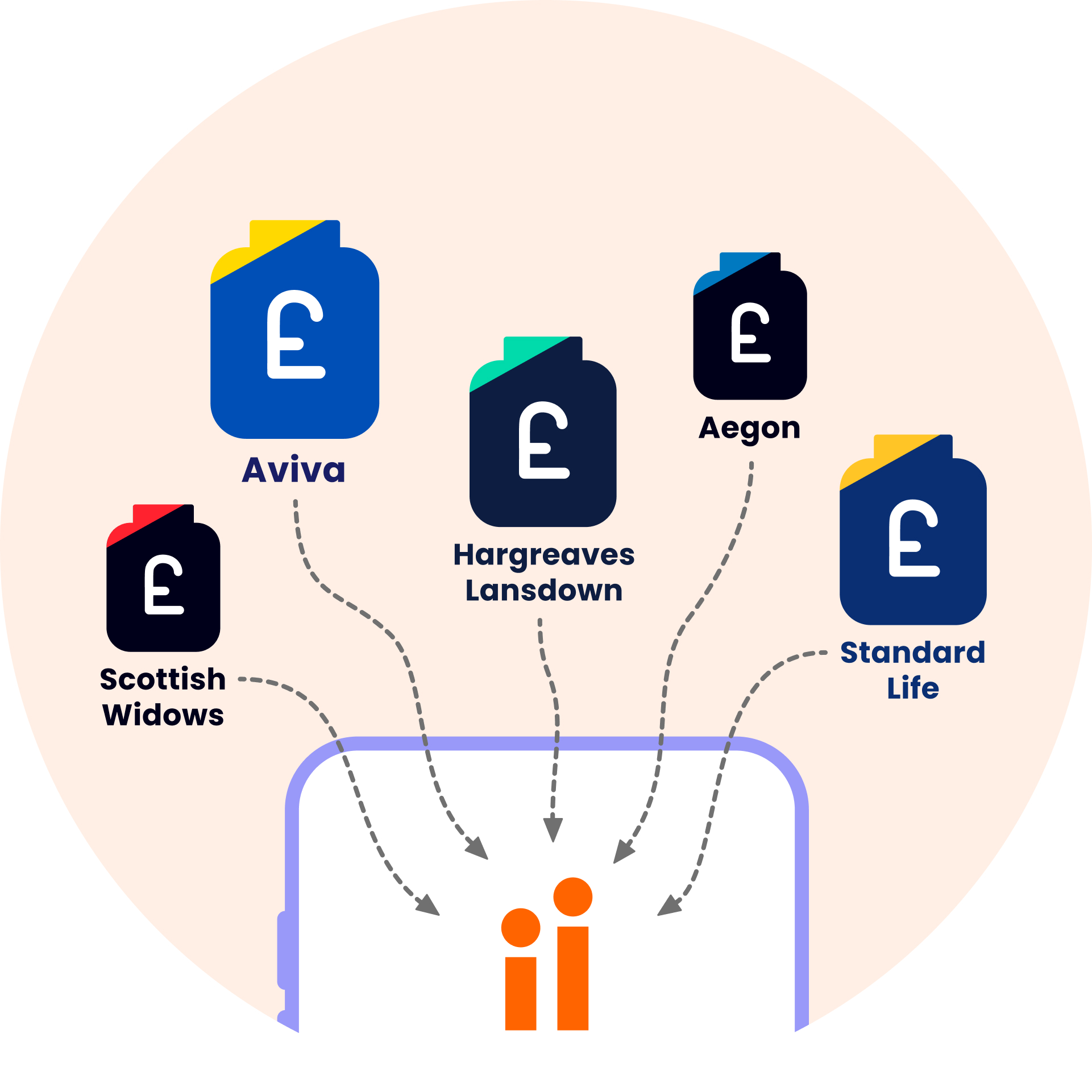

Do you have old pensions with high fees?

It's easy to consolidate your pensions with ii. From old workplace pensions to SIPPs, even with traditional pension providers like Standard Life, transferring to ii gives you more control over your money and, possibly, lower fees.

You can do this entirely online once you open an ii Personal Pension.

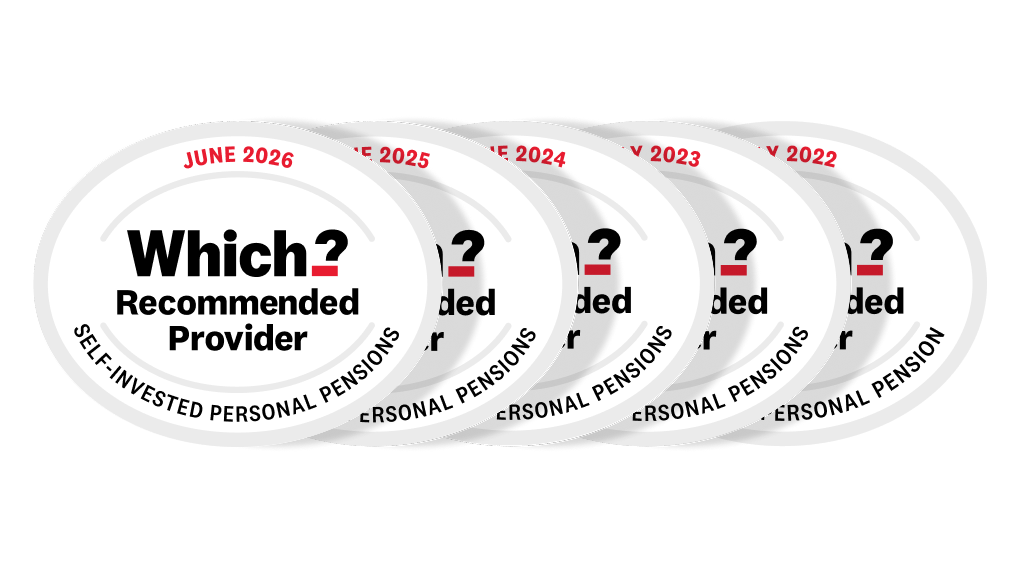

Switch to a five-time Which? Recommended SIPP

For the fifth year in a row, independent analysts at Which? have recognised the ii Self-Invested Personal Pension for its industry-leading choice, support and value.

Join over 500,000 ii investors and start prioritising your pension with our award-winning, low-cost SIPP.

ii vs Standard Life FAQs

You can start your transfer in a few minutes when opening your ii Personal Pension.

If you’re already an ii customer, you can start a transfer at any time from your account — just go to Portfolio > Transfers > Transfer in.

This depends on the make-up with your portfolio with Standard Life. Funds, ETFs, shares, and other assets that are also offered on the ii platform can normally be transferred across.

Standard Life-branded funds, like the Future Advantage range or the sustainable multi asset investment options, and other investments aren’t available through ii. If you’ve invested in these funds you will need to sell your holdings and use the cash to make similar investments on our platform.

There are no charges from us when you transfer to ii from Standard Life. However, it’s always best to check with Standard Life that you won’t be charged any exit fees or lose any pension benefits.

Yes, you can transfer pensions in drawdown to the ii Personal Pension.

What to know before transferring a pension in drawdown:

- You may not be able to take an income from your pension during your transfer.

- If you want to transfer a pension in drawdown, the entire drawdown (crystallised) pot must be transferred, as partial transfers of drawdown funds are not permitted. If you have both a drawdown (crystallised) pot and a non-drawdown (uncrystallised) pot, you can transfer either pot separately or both together to interactive investor.

- If you hold both drawdown and non-drawdown pots in your ii Personal Pension, they are managed using notional split. This means that the value of each pot will change in line with the overall performance of all the investments held in your SIPP, read more about how the ii notional split works.

We will process your transfer as soon as possible. Transferring a pension usually takes 2 to 6 weeks to complete for a cash transfer, going up to 8 to 12 weeks if you’re transferring your investments.

Last year, the average pension transfer from Standard Life took 29 days to complete.

You will need to provide us with your pension's scheme and policy number. These can often be found on your statement or online account.

We’ll also need to know your National Insurance number, which you can find on your payslip or P60.

You can view the progress of your transfer securely at any time within your ii account. Our transfers team will also provide you with key updates via Secure Messaging and email throughout the process.

Once the transfer process is finalised, your balance will update.

You can easily get in touch with our UK-based support team for any questions you have. If you're already a customer, feel free to send a secure message from your account page or mobile app.

The best number to reach us on is 0345 607 6001. Or, if you’re calling from abroad, +44 113 346 2370. Our lines are open 7.45am to 5.30pm (GMT), Monday to Friday.