Next shares up 50% in 2019 after second-quarter boost

Investors want quality stocks, and Next is showing the rest how it's done with a big results upgrade.

31st July 2019 13:03

by Graeme Evans from interactive investor

Investors want quality stocks, and Next is showing the rest how it's done with a big results upgrade.

A £10 million profits upgrade pushed Next (LSE:NXT) shares to a level not seen for a year and not far off prices last traded in early 2016, as the high street stalwart set an impressive industry benchmark on summer trading.

At a time when the gulf between retail success stories and the laggards appears to be getting wider, Next reported a bigger-than-expected 4% rise in full-price sales in the second quarter.

This was sufficient for chief executive Simon Wolfson to loosen his usual cautious stance on forecast guidance, with the company now expecting earnings per share growth of 5.2% in 2019/20 rather than 3.4%. Profits will be marginally higher than last year at £725 million.

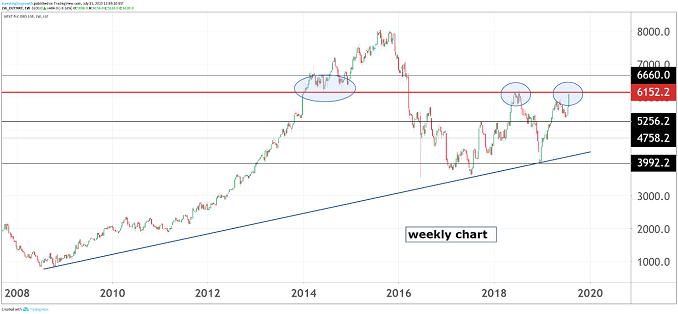

Next shares, which have a tendency to move sharply on the day of results or trading updates, surged by more than 10% to 6,150p at one point. The stock is now up over 50% in 2019, but 6,150p is a key level for technical analysts (see chart below).

Source: TradingView Past performance is not a guide to future performance

The rally ranks Next alongside the likes of Dunelm (LSE:DNLM) and Hotel Chocolat (LSE:HOTC) as 2019's retail star performers, whereas struggling Marks & Spencer (LSE:MKS) shares are down 11% in the year-to-date.

As this was only a trading update, Lord Wolfson kept analysts and investors guessing about what's behind the impressive performance. But it's safe to say that Next has been picking up market share as more retailers use company voluntary arrangements (CVA) to exit stores.

Next is committed to its sprawling shop estate, believing that the stores are far from a liability if they provide a point for online customers to collect and return their orders.

And while the CVA process has distorted the picture on rents against the likes of Next, today's update shows that its high street stores continue to have a big role to play in the company's ongoing success. Whereas analysts had expected retail store sales to be down by more than 10% in the second quarter, the actual figure was a more resilient 4.2% lower.

The powerhouse behind the strong trading, however, continues to be online. Sales were up 12% in the three months to July 27, compared with the 9.7% consensus forecast and building on growth of 11.8% in the previous quarter.

This is likely to have been aided by the expansion of Label, which now sells more than £400 million a year of third-party ranges from brands including Adidas (XETRA:ADS), Boohoo (LSE:BOO) and French Connection (LSE:FCCN). Online momentum may also reflect the influence of new projects using AI search engine intelligence or offering customers additional personalisation.

Overall, Next now expects sales for the full year to be 3.6% higher rather than the 1.7% rise previously forecast - the equivalent of a £70 million uplift. In May, Wolfson declined to boost guidance despite a strong performance in the first quarter.

He has based today's upgrade on the combined 3% rise in full-price sales seen during May and June, rather than this month's 6.8% improvement when the performance may have been distorted by comparisons with last year's end-of-season sale.

The recent surge in the Next share price has left the FTSE 100 stock trading with a forward price multiple of just over 12 times 2020 earnings. Jefferies said this was a 15% premium to other large-cap FTSE retailers and also represented an historical peak.

Upgrading forecasts by 2% and the broker's price target to 5,600p, the team at Jefferies added:

"Operationally driven earnings progress remains limited, and the premium valuation sizeable. But the newfound offline resilience is starting to intrigue."

Analysts at UBS have a price target of 6,300p, which now looks to be up with events.

Meanwhile, the retailer continues to return surplus cash to shareholders after £280 million of shares were bought back in the first half of the year. It has a target of £300 million for the year, with the dividend yield for 2020 also standing at 3.1%.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.