ii Winter Portfolios: A defensive seasonal strategy

A better end to the month repaired some of the damage, and one of our portfolios proved more resilient.

3rd April 2020 09:00

by Lee Wild from interactive investor

A better end to the month repaired some of the damage, and one of our portfolios proved more resilient.

When we updated you on the performance of the interactive investor Winter Portfolios on 23 March, following the worsening of the coronavirus pandemic, it turns out many share prices were at or very near their low point. The FTSE 250 index had fallen as much as 42% in 2020 and the FTSE 100 around 36%, but we are glad to say things have got better.

Shutting pubs, bars, cafes and schools, getting as many people working from home, mothballing building projects and social distancing has made it impossible for many businesses to function. And we still don’t know precisely how long this situation will last.

There have been many very significant corporate losers in the past month, but there have also been winners. Some online retailers are doing business like it’s Christmas, supermarkets are booming and companies involved in hygiene or anything to do with Covid-19 have been chased higher.

- ii Winter Portfolios: Coronavirus update

- Discover how we do it by clicking here

- Find out more about interactive investor’s winter portfolios on our dedicated hub page

The ‘winter’ period - 31 October to 30 April for the purposes of our seasonal portfolios - is historically the most profitable period to own equities.

But it was inevitable that our two baskets of shares would get caught up in the panic. Both have fallen sharply as the drivers which typically make the portfolios work - greater flows of money into the market and ISA season buying – break down.

With very little idea how long the lockdown will last it has become impossible to accurately value shares. There will be a significant economic impact, but how much? Corporate dividends have been suspended, so income investors are wondering where to move their cash.

In the six years since we launched our winter portfolios, the consistent basket of shares - five FTSE 350 stocks with the most reliable returns over the past 10 years - has typically returned less than the higher-risk aggressive portfolio. However, it is times like these that the reliability of its constituents is of great benefit to investors.

While we hadn’t anticipated a major health scare would disrupt our portfolios, that our 'consistent' shares are down significantly less than the FTSE 350 benchmark index is testament to the quality stocks within it.

Our Consistent Winter Portfolio fell 14.7% in March, less than the FTSE 350’s 15.2% decline. The portfolio is now down 14.3% since the six-month portfolios were launched on 31 October 2019. The FTSE 350 is down 22.2%.

It’s been tougher for the Aggressive Winter Portfolio, which relaxes the entry criteria only very slightly in return for much higher potential returns. Its five constituent stocks are high-growth companies and are priced as such.

But it’s these growth stocks that have been hit hardest in the market rout as Covid-19 begins to have a devastating impact on global economic growth. The aggressive portfolio lost over 30% in March, twice as much as the benchmark index. For the first five months of this year’s six-month strategy, the portfolio is down just under 31%, but just two weeks ago it was down almost 50%. Things change very quickly in this market.

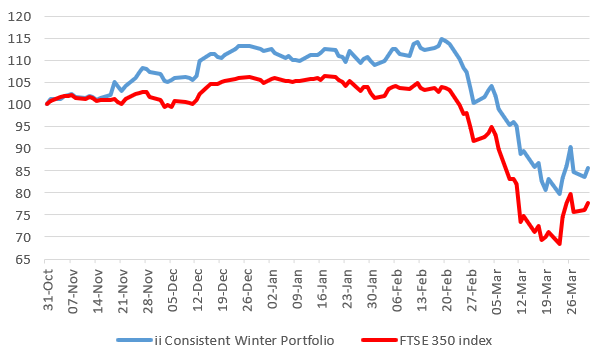

interactive investor Consistent Winter Portfolio 2019-2020

Source: interactive investor, Morningstar data up to close of business 31 March 2020 Past performance is not a guide to future performance

Technology conglomerate Halma (LSE:HLMA), in its maiden year as a winter portfolio share, is the only constituent across both portfolios to register a gain for the five months since October – up 2.5%.

FTSE 100 speciality chemicals firm Croda International (LSE:CRDA) fell only 6% in March and is now down a comparatively modest 11.3% since this season’s portfolio launched. Howden Joinery (LSE:HWDN) had been flying before the crash and, despite a 19% loss last month, is also down 11.3% for the winter so far.

Two stocks have done real damage to the consistent portfolio - Holiday Inn and Crowne Plaza owner InterContinental Hotels (LSE:IHG) and motorway barriers firm Hill & Smith (LSE:HILS). The former was one of the first to wobble – its shares had begun falling late February as travel restrictions and the worsening pandemic was a clear threat to business – but the selling accelerated and by 19 March the shares had lost nearly half their value since this season’s winter portfolios launched in October.

While InterContinental was plumbing the depths, Hill & Smith was still in positive territory for this winter portfolio. Its decline was less dramatic than others, but the shares still fell 29% in the final two weeks of the month as it scrapped the dividend and warned that its French and Indian operations had been disrupted.

It has also shut half its UK business. All US stores remained open at the time, although Covid-19 was still working its way across the States.

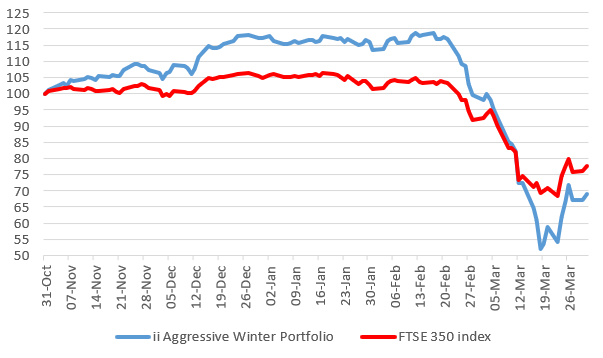

interactive investor Aggressive Winter Portfolio 2019-2020

Source: interactive investor, Morningstar data up to close of business 31 March 2020 Past performance is not a guide to future performance

Equipment rental firm Ashtead (LSE:AHT) and chemicals company Synthomer (LSE:SYNT) were down heavily, like most other stocks, but the main culprits behind the aggressive portfolio’s massive losses were workspace provider IWG (LSE:IWG), high street sportswear chain JD Sports (LSE:JD.) and heat treatment firm Bodycote (LSE:BOY).

Though it had given up its 19% profit achieved by mid-February, the portfolio was still flat heading into March. There were steep losses in the first part of the month, but the most significant damage was done between 11th and 18th March. During those few days IWG plunged 61% and JD 54%.

Bodycote took a day longer to bottom out with a 33% seven-day loss. At their worst, the trio were down 70%, 61% and 40% respectively since the portfolio began in October.

But these are volatile times and, since hitting their low point mid-month, IWG has risen 51%, JD 56% and Bodycote 30%. Since the winter portfolios launched at the end of October the trio are now down 55%, 40% and 21% respectively.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.