Does boom in share buybacks really signal market top?

23rd May 2018 09:32

by Tom Bailey from interactive investor

Share buybacks involve companies buying their own shares as a means to raise their price and provide returns to shareholders. While in the UK the favoured way for firms to give shareholders a lift is through dividend payments, in the US share buybacks are often preferred.

In the first quarter of 2018, US companies spent a record $178 billion in buybacks, beating the previous quarterly record of $172 billion, set ominously in the third quarter of 2007.

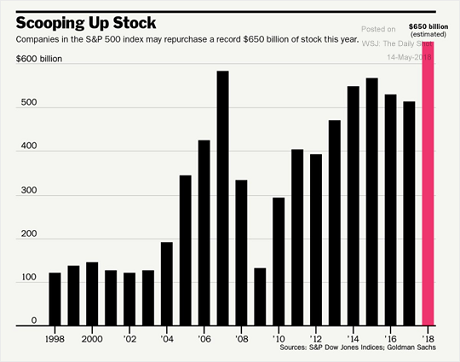

If buybacks continue at this pace firms in the S&P 500 are estimated to set a repurchase record of $650 billion dollars a year (see chart below), while total shareholder pay-outs from US firms (buybacks plus dividends) are on track reach a record $1 trillion.

Behind the flurry of buybacks is the US recent corporate tax cut. Strong economic growth would have provided profit for companies to put in shareholders profits via buybacks. However, the slashing of corporate tax rate from 35% to 21% has made US firms flush with cash, allowing them to reward shareholders.

Source: Barron's Past performance is not a guide to future performance

Bad for business?

Alongside the question of passive versus active investing, whether or not buybacks are actually good is one of the most contentious questions in finance.

If you are holding the shares that have been subject to a buyback, the resulting price rise is cause for celebration. That, however, may be short-termist. In the long-run, it may be undermining the company you're holding.

One major critic, Larry Fink, the CEO of BlackRock has made this argument, warning against businesses looking to "deliver immediate returns to shareholders, such as buybacks…while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth."

This argument is a typical part of the critique of 'shareholder capitalism,' where firms are accused prioritising earning per share each quarter over the longevity of their company, and by implication the economy.

If that really is the case though, whether that matters for your portfolio depends on your investing time horizon. If a company engaging in buybacks is a 'orphans and widow stock,' it may be troubling. If your time horizon for holding the company is shorter, from a purely investor perspective, buybacks undermining innovation may not matter so much.

At the same time, the idea that share buybacks came at the expense of business and economic health is not certain.

According to Jesse Fried and Charles Wang, professors at Harvard Business School, capital flowing to shareholders does not go down the economic drain.

The professors argue that shareholders use much of the cash to invest in smaller public and private firms, which in turn supports innovation throughout the economy.

At the same time, they argue, in a climate of growing share buybacks, corporate investment hasn't fallen. Looking at the US S&P 500, capital expenditure and research and development as a percentage of revenue has been rising over the past decade.

Harbinger of market turmoil?

However, in the wake of sudden and large market dips earlier in the year, some have started to fear buybacks may cause market instability. While firms carrying out buybacks aren't usually particularly price sensitive, they will try and buy when there is a dip.

That, writes Bloomberg columnist Stephen Gandel, "insulates the market against drops, which causes volatility to drop."

He adds: "Lower volatility causes humans to think stocks are safer than they are and computers to actually calculate that. Everyone piles into stocks, which lowers volatility further, until there's a big blow-off."

As the economist Hyman Minsky said "stability breeds instability."

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.