Great value alternatives to the most-popular funds

Last year's most-bought funds and trusts may be less successful in 2019, so here are some new ideas.

18th February 2019 09:10

by Marina Gerner from interactive investor

Last year's most-bought funds and trusts may be less successful in 2019, so here are some new ideas.

Over the past two years, investors have piled into global funds and trusts, many of which were focused on US technology growth stocks. However, the bull market now appears to be over – with market volatility having continued since October's correction – so now is a good time to consider how likely the highest-profile and most-bought funds and trusts are to continue doing well.

Many investors have been looking for value-oriented alternatives to their strongly growth-focused funds. Andrzej Borkowski, head of investment at wealth manager Arcrate, says:

"We are still happy to hold some of the most popular growth funds, as they have fared well in volatile markets compared with typical value funds."

Steve Wilson, director at Alan Steel Asset Management, says value investing tends to outperform investing in growth over the long term, but that "the journey tends to be more spiky and volatile". He favours a blend of styles rather than nailing his colours to a single mast.

- Invest with ii: Accumulation or Income Funds | Top Investment Funds | Open a Trading Account

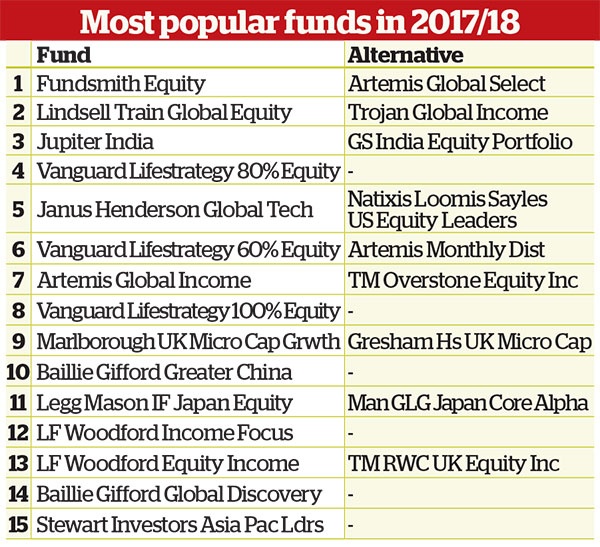

Here, we take a look the most-bought investments by clients of our parent, online broker interactive investor, over the past two years and ask some experts to suggest lesser-known alternatives with similar investment philosophies that are worth considering as alternatives.

Fund switches

The undisputed king of the most-bought fund list is Terry Smith's Fundsmith Equity: the fund has performed splendidly. However, Adrian Lowcock, head of personal investing at Willis Owen, warns that it is unlikely to do well in all market conditions.

As an alternative, he suggests Artemis Global Select. The fund's managers seek out quality firms trading at attractive valuations that are set to benefit from "identified long-term secular growth trends". Lowcock says these businesses benefit from high barriers to entry to their markets, sustainable cash flows and "limited exposure to external factors". He adds: "The managers follow a disciplined valuation approach and can hold up to 20% in cash."

The second most-bought fund on ii is Lindsell Train Global Equity. Wilson says: "As is typical of Lindsell Train funds, it is concentrated, with 10% positions in many stocks." He adds that an alternative to this favourite is a much smaller and significantly less concentrated fund, Trojan Global Income. It also has a "focus on quality names that also pay a good dividend".

Next on the list is Jupiter India. Darius McDermott, managing director at FundCalibre, says a good alternative is the Goldman Sachs India Equity Portfolio. It might be worth swapping, he suggests, as the latter has "much better performance and greater diversification", as well as a presence on the ground in India and Singapore. It has a bias to small- and mid-caps "but manages to be an all-weather fund fit for any environment".

Janus Henderson Global Technology, the fifth most popular fund, is highly focused on the US tech giants, which some fear are running out of steam. Wilson says the fund could be replaced with Natixis Loomis Sayles US Equity Leaders "if you still believe tech has room to grow", as it too is heavily invested in US tech. He praises the manager's strong buy/sell discipline.

The passive multi-asset fund Vanguard LifeStrategy 60% Equity is next on the list. In a downturn, active funds that can mitigate the full impact of market falls are likely to outperform passive ones. The suggested active replacement, Artemis Monthly Distribution, is "a lot more expensive and likely to hold less in equities," says Ben Willis, head of portfolio management at Chase de Vere, but it provides "a much higher yield and access to two of Artemis's most experienced managers, James Foster and Jacob de Tusch-Lec". He says it is popular with investors because of its track record, but it is still only a fifth of the size of the Vanguard fund.

Another popular fund is Artemis Global Income. This fund is very large and investors might prefer a smaller alternative. A good substitute here "with more of a value focus" would be TM Overstone Equity Income, says Wilson. Being a small fund, with assets of just £85 million, it is more nimble than the Artemis fund, he adds.

Next up, Marlborough UK Micro Cap Growth focuses on smaller companies. However, it is highly diversified; given the uncertain environment in the UK, investors might prefer a higher-conviction portfolio. McDermott says Gresham House UK Micro Cap is a strong and quite different alternative. He says it is "much more concentrated and only focuses on a few specialist sectors where it has expertise".

Investors keen on Japan have been buying the Legg Mason IF Japan Equity fund. This fund has its largest weighting in industrials, which are exposed to wider trade tensions. As an alternative, Lowcock suggests Man GLG Japan Core Alpha, a "larger-cap, value-orientated fund" that has its largest weighting in financials. Manager Stephen Harker is a contrarian who focuses on the largest 300 Japan-listed companies.

Despite being plagued by troubles, Neil Woodford's LF Woodford Equity Income remains ensconced on the most-bought list. Willis suggests replacing it with TM RWC UK Equity Income.

"The managers have more of a value tilt than Woodford's fund, will not invest in unquoted companies and always aim to deliver a yield higher than the market provides."

Trust substitutes

Table-topping Scottish Mortgage (LSE:SMT) is "heavily weighted to global consumer growth", says John Ditchfield, a partner at Castlefield, but it's "not strong on secular themes". One alternative would be the Impax Environmental Markets (LSE:IEM), which invests in companies focused on energy, water and waste management, and provides diversification from general consumer growth stocks.

Ditchfield says:

"Over the past six months many consumer-driven trusts saw their share prices fall in value, but Impax delivered a positive return, illustrating the diversification benefit of maintaining some exposure to environmental infrastructure."

The second most-bought trust was City of London (LSE:CTY). This trust is huge, and could be replaced with one just a third of its size, JPMorgan Claverhouse (LSE:JCH). This trust would be an alternative for UK equity income exposure, says Charles Cade, head of investment companies research at Numis Securities. He adds that performance has been strong "through a bottom-up, stockpicking approach with an emphasis on quality, momentum and value". The trust yields 4.1% and has grown its dividend for 45 consecutive years.

Witan's multi-manager global trust is fourth on our list. Multi-manager alternative Alliance Trust (LSE:ATST) is worth considering as a swap, as it's currently (10 January) trading at a wider discount of 4.6%, says Cade. "It is managed by Willis Towers Watson, which also advises Witan, with the portfolio management delegated to eight underlying managers."

Fidelity China Special Situations (LSE:FCSS) is the sixth most-bought trust. Cade likes it, but suggests investors consider exposure to Vietnam via VinaCapital Vietnam Opportunity (LSE:VOF). He says: Vietnam has "healthy economic growth of about 7% a year, supported by positive demographics". The trust focuses on domestic consumption and infrastructure growth, and it is trading at a discount to NAV of 16%, representing "considerable value".

Baillie Gifford Shin Nippon (LSE:BGS) has long been an investor favourite. Rob Morgan, investment analyst at Charles Stanley, says: "It has a distinct growth and smaller-company style, and I would not expect the extent of outperformance in recent years to continue. I rate the fund and the team highly, but the 5.3% share price premium seems a bit rich." He adds that Coupland Cardiff Japan Income and Growth isn't that well-known, but its management is "high quality and it’s a more rounded portfolio of dividend-paying companies".

The popular F&C Investment Trust (LSE:FCIT) is very growth oriented and could therefore be replaced with British Empire (LSE:BTEM), says Morgan. "At this juncture it may be wise to reconsider some top-value orientated trusts that have had a tough time but could pick up the baton." He adds that the trust has historically held a combination of family controlled companies and trusts, but that increasingly value opportunities are being identified in other areas, especially in Japan. Besides, its 9% discount "stands in contrast to those of better-known global funds".

Ultra-defensive RIT Capital (LSE:RCP) was the 10th most-bought trust on the list, but it is on a 9% premium. Morgan says Personal Assets (LSE:PNL) "is more defensive and trades much closer to NAV". It "makes a good core long-term holding with a genuine wealth preservation mindset".

TR European Growth (LSE:TRG) had a terrible year, so Morgan's choice in the European smaller companies sector is JPMorgan European Smaller Companies (LSE:JESC). He says it has done better, has a similar discount to NAV and boasts a strong management team. However, it's "high octane and while it should perform well in rising markets, it is susceptible to sharp drawdowns in periods of weakness".

As ever, there are opportunities for brave investors when markets are volatile and uncertain. However, not everybody sees merit in fund switches at this point. Brian Dennehy at FundExpert says that it's crucial to have higher cash positions than usual – "our clients are towards 50%" – and he recommends a stop-loss to protect capital value.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.