Top tips to minimise your tax bill for this tax year and the next

A 10-point checklist outlines how you can up your tax-efficiency game as the end of the tax year nears.…

5th March 2020 08:56

by Sam Barrett from interactive investor

A 10-point checklist outlines how you can up your tax-efficiency game as the end of the tax year nears.

Medieval accounting practices coupled with a switch to the Gregorian calendar have left us with a tax year that starts on 6 April. That date may not have quite the same cachet as 1 January, but it’s one that’s well worth remembering, as many allowances are linked to the tax year.

This 10-point checklist straddles the tax year end to remind you of the tasks you need to do before the clock strikes midnight on 5 April, and those you need to focus on in the new tax year.

- How should the wind-up of Woodford Equity Income be treated for tax purposes?

- Ask Money: why no consideration of the 14-year rule?

1) Make use of your Isa allowance

It’s sensible to hold any savings or investments you have in tax-efficient Isa wrappers. There are four main types for adults: cash, stocks and shares, Innovative Finance and Lifetime Isas. You can invest up to £20,000 across these in the 2019/20 tax year. “If you already hold shares, move them into an Isa wrapper if you can,” says Jeannie Boyle, a chartered financial planner at EQ Investors. “Don’t forget your spouse’s allowance, and even your kids get an annual allowance of £4,368 (2019/20) in a Junior Isa.”

If you’re aged between 18 and 39, consider a Lifetime Isa. These allow you to pay in up to £4,000 of your annual allowance. The government will top that up with a 25% bonus, as long as the Isa money is used to buy your first home or is not taken until at least age 60.

Jamie Jenkins, head of global savings policy at Standard Life, says investing in an Isa is a good way to supplement retirement income, as withdrawals are taxfree. He explains: “By taking income from different sources, rather than just your pension, you can potentially reduce the amount of tax you'll pay.”

- Six tips for Isa investors in a volatile market

2) Pump up your pension

It’s also worth thinking about your pension pot, as annual pension allowances are tied to the tax year. “You can pay in up to £40,000 a year with tax relief, providing you have sufficient earnings,” says Anna Murdock, head of wealth planning at JM Finn. “You could also use ‘carry forward’, which allows you to soak up unused allowances from the previous three tax years. This sets the maximum at £160,000.” Carry forward can be done via your tax return.

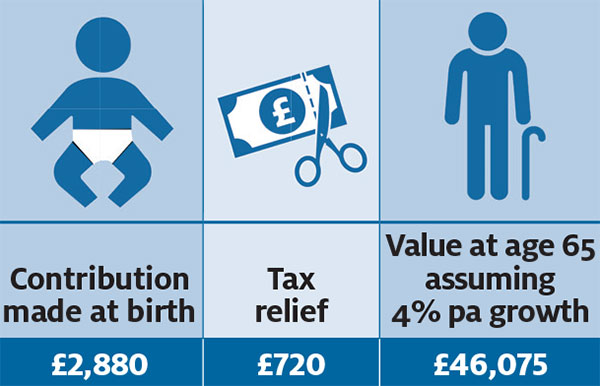

Even without earning, you can still pay in £2,880, which will be topped up to £3,600 by the government. While this can be a handy option for a non-earning spouse, David Jamieson, a financial adviser at Gee 7 Wealth Management, suggests setting up pensions for children and grandchildren too.

“It’s a really tax-efficient way to give them a financial head-start,” he says. “And seeing how their pension investments grow can be a catalyst for a lifetime of good money management.”

- Steve Webb: the essentials on saving a pension for your children

3) Make capital from your gains

Even if you’re not planning to cash an investment in, it’s worth casting an eye over the gains your investments have made. These could be liable to capital gains tax (CGT) at the rate of 10% (20% if you’re a higher-rate taxpayer or the gain pushes you into the higher-rate tax band) when they are sold.

Eddie Grant, divisional director for professional development at St James’s Place, advises taking advantage of the annual allowance (£12,000 in 2019/20) if you can. He says: “Many investors fail to use their CGT annual exemption. You can’t sell shares and buy them back within 30 days, but you could purchase alternative holdings, make a pension contribution or invest in an Isa.” Capital withdrawals can also be used as income.

- 10 little-known tax traps and how to avoid them

4) Minimise your estate

Tax-efficient estate planning is best done in small but frequent steps, especially as the tax-exempt allowances haven’t been updated since the 1970s.

It’s possible – and worthwhile – to take advantage of inheritance tax exemptions such as gifts for weddings or civil ceremonies and small gifts of up to £250, but the annual exemption is the one to be mindful of in your tax year-end planning.

“You can give away up to £3,000 each year and it’ll be outside your estate,” says Emma Watson, head of financial planning at Rathbones. “If you didn’t do that in the past tax year, you can use that year’s allowance this year. A couple could give away £12,000 between them.”

5) Be charitable

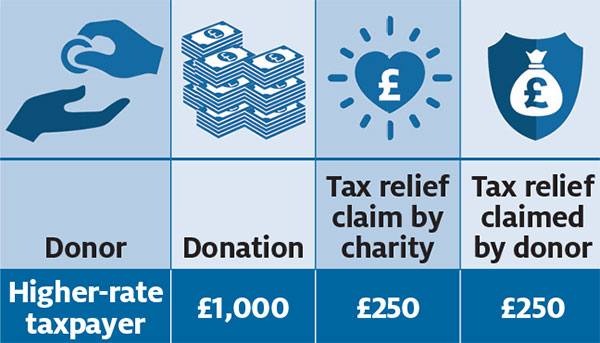

Giving to charity could also be part of your year-end tax planning. While a charity can claim Gift Aid on your donations – worth an extra 25p for every £1 you donate – if you’re a higher-rate taxpayer, you can claim the difference between the rate you pay and the basic rate on your donation. This will give you tax relief of 25p for every £1 you donate.

“Many people overlook this, but it’s easy to claim through your tax return,” says Boyle. “Giving to charity can make you – and your finances – feel good.”

- Sweet charity: how the principles of philanthropy can benefit donors and good causes

6) Mind the income thresholds

Earning more than £50,000 comes with a sting, and so does earning more than £100,000. Exceed £50,000 and your entitlement to child benefit is eroded at the rate of 1% for every £100 you earn – it hits zero when you earn £60,000. Earn £100,000 and it’s your personal allowance that’s at stake. Every £2 you earn beyond this will knock £1 off your personal allowance (£12,500 in 2019/20) until it disappears completely at £125,000.

If your earnings aren’t too far above these thresholds, Watson recommends making a contribution to your pension and/or a donation to charity to bring your earnings below the thresholds. She says: “It could boost your pension and it could also give you back your child benefit or personal allowance.”

7) Go specialist

Investment vehicles such as venture capital trusts (VCTs) and enterprise investment schemes (EIS) offer significant tax advantages for those wanting to take advantage of the annual allowances (£200,000 for VCTs and £1 million for EISs in 2019/20). Both VCTs and EISs offer upfront income tax relief of up to 30%, which can significantly cut your tax bill. In addition, VCTs offer tax-free dividends, and after two years your holding in an EIS will be outside your estate for inheritance tax purposes.

- Woodford woes not negatively impacting VCT fundraising

8) Get your tax affairs in order early

If you’re married or have a civil partner, Philpott recommends looking at how your finances are held. “If one of you is a lower bracket taxpayer than the other, it may be worth transferring any taxable savings or investments to them,” she says. “You could also consider sharing assets or investments where there’s a potential CGT liability, as this allows you to use both CGT allowances.”

9) Complete your tax return on time

Nearly half of us leave our self-assessment tax return until January; almost a million taxpayers missed this year’s deadline and will be fined at least £100, according to HMRC. To avoid a fine and mistakes made in haste, it’s worth doing it at the start of the tax year. Jamieson says: “You might have to wait for some paperwork, such as your P60, but if you’re a higher-rate taxpayer and you’re due pension tax relief, the earlier you submit your tax return, the earlier you’ll get it.”

- Pensions vs Isas - which is best for a lump sum at tax-year end?

10) Start using your allowances

Although many of us wait until the end of the tax year to use our allowances, Boyle recommends paying into your Isa and pension as early as possible: “As well as avoiding the last-minute rush, you’re less likely to end up investing in the latest hyped fund.”

Moreover, if you opt for a flexible Isa, paying in early no longer entails a long-term commitment. Murdock says: “You can withdraw money you’ve paid in during a tax year and, as long as it’s paid back in before 6 April, you won’t reduce your annual Isa allowance.”

If you haven’t already got £20,000 to put into an Isa, it may be worth setting up a monthly contribution. “If you invest regularly, you’ll be buying more stocks when markets are cheap and fewer when they’re pricier, taking advantage of pound cost averaging,” says Jenkins.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.