Compare our flat fee

The UK's #1 flat-fee investment platform

Let your wealth grow, not your charges. Save more money for your future with a low, flat fee and join over 500,000 investors today.

Important information: As investment values can go down as well as up, you may not get back all of the money you invest. If you're unsure about investing, please speak to an authorised financial adviser. Tax treatment depends on your individual circumstances and may be subject to change in the future. Please note images displayed are for illustrative purposes only.

Welcome to thousands of new investors

Is it time you joined them?

The penny’s dropped for thousands of people up and down the country. They know they get better choice, value, and support with interactive investor and have transferred their investments.

Join over 500,000 investors and discover what flat-fee investing can do for you.

What's the flat-fee difference?

Most other investment platforms charge a percentage fee of your portfolio. The impact? The more your pot grows, the more they take.

But a flat fee is clear, transparent, and simple, and can help you keep your account costs low. What you save compounds, so your money has even more room to grow.

With ii, you get access to a Personal Pension, ISA, and Trading Account. And our Plus and Premium plans include free family accounts, so your loved ones can also make significant savings. For a full view of our benefits and trading fees, check our charges page.

Take care of all your investments, all on one platform, all for one low, flat fee.

Why other investors switched to ii's flat fee

Mark

“Being really blunt, ii was just so much cheaper. With other platforms, it’s this plus that plus that. Whereas with ii, what I pay is what I pay.”

Fang

“Once I heard flat fees, I jumped at it. I calculated all my fees and said ‘that’s really expensive compared to ii’. Why didn’t I do it earlier?”

Lisa

“I had everything in different places. I’ve moved it all to ii now, which was very simple. I thought it was going to be a nightmare, but it wasn’t.”

Monika & Lionel

“Since moving to ii – eye-opening. Clarity, power, decision, service and the app is fantastic. It’s freedom, in a way.”

Enzo

“My previous providers were Aviva and Scottish Widows. I had the realisation that the fees, compared to ii, didn’t sit too well with me.”

Chris

“It was easy to transfer to ii. Any interaction with customer support has been human, refreshing, and different to what I’ve experienced before.”

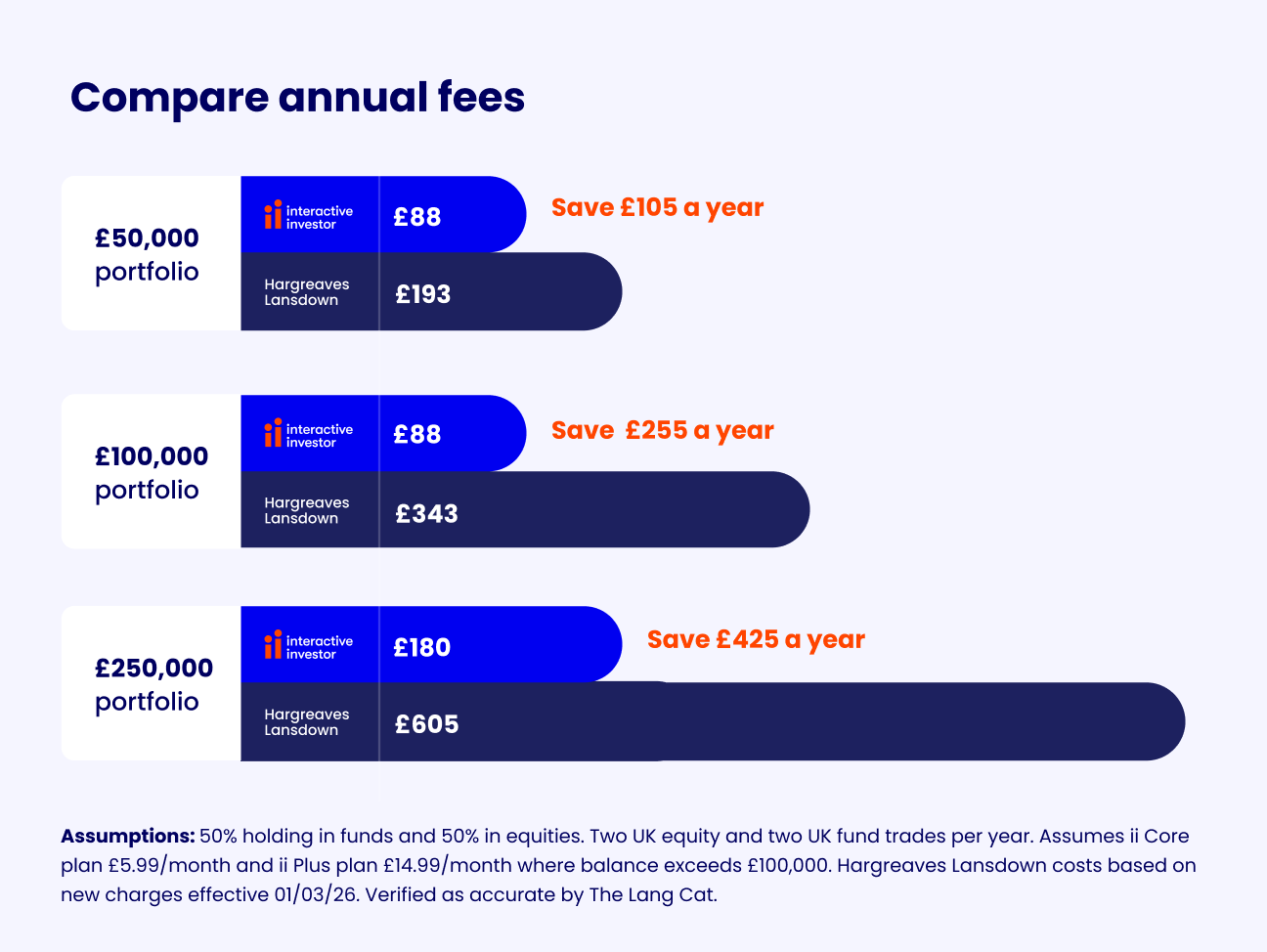

Compare your costs: ii vs Hargreaves Lansdown

See how our flat fee stacks up against percentage-based charges from Hargreaves Lansdown.

Discover how our platforms compare and why you could find better value with ii.

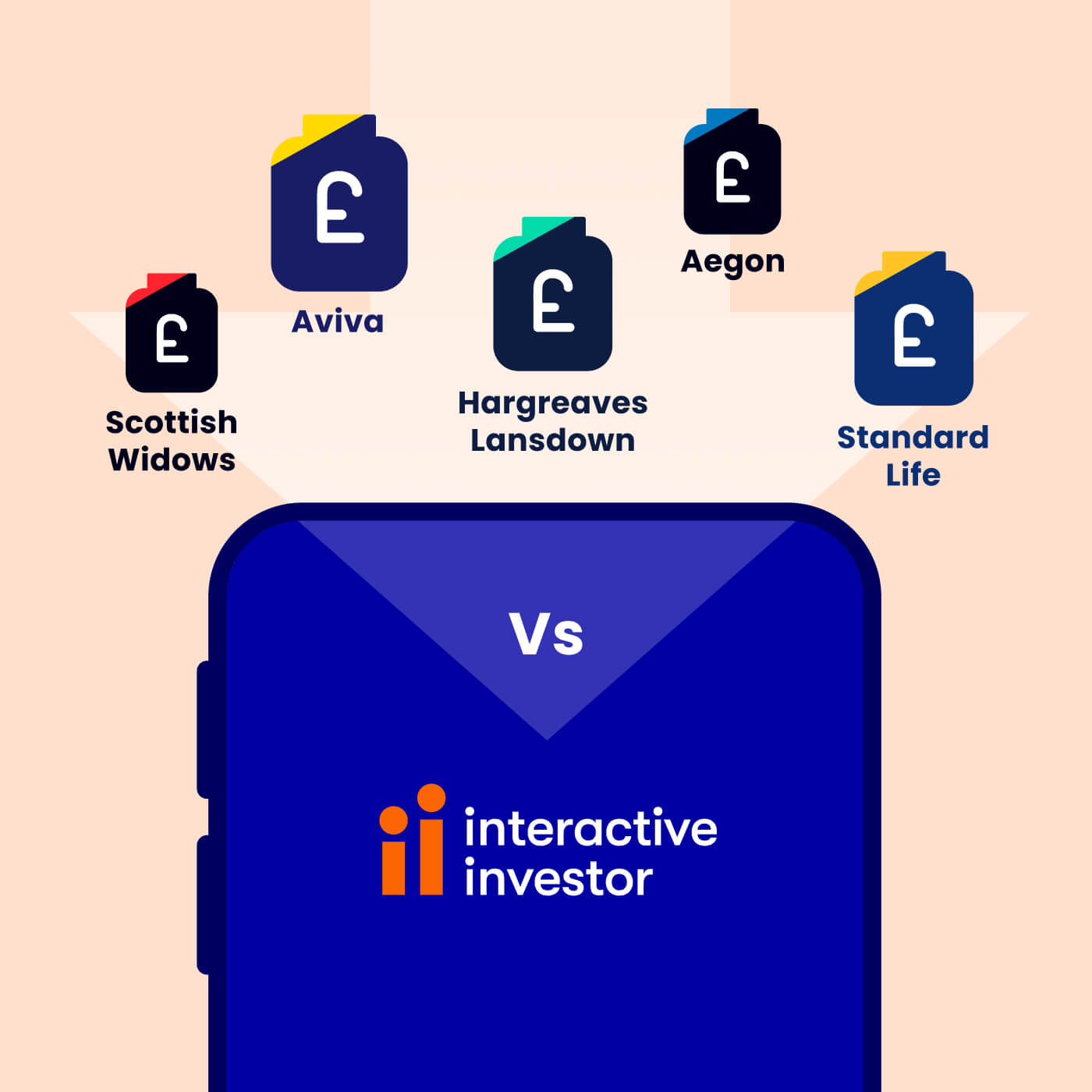

Your dream retirement starts with a flat-fee pension

Over 100,000 pensions worth billions have already been transferred to ii.

See how the ii Personal Pension compares to some of the biggest pension providers around, like Aviva and Standard Life.

Why Bobby transferred his pension to ii

“I would recommend ii because it’s a much better option. You can transfer funds in really easily, can see what’s happening with your money in real time, and have the upside of all the choice. That’s why I’m with ii.”

Bobby transferred from Aviva because he wanted a platform with a simpler fee that gave him the control and investment options he was looking for.

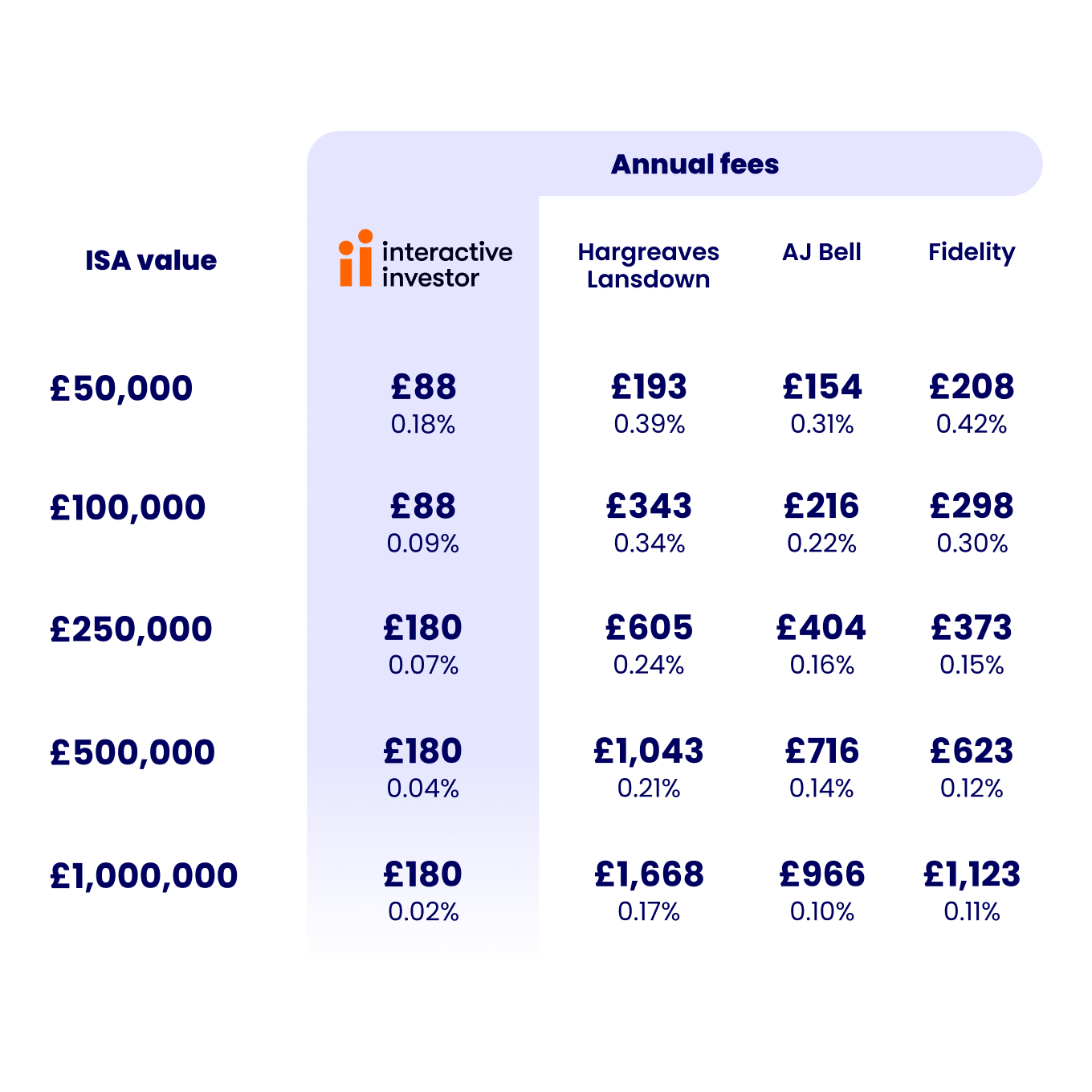

Investing that isn't taxing with a flat-fee ISA

Could you pay less for your ISA? Maybe with a flat fee.

Compare our Stocks & Shares ISA to other providers – such as AJ Bell, Hargreaves Lansdown, and Fidelity – and start keeping more of the money you make.

Comparison disclosure: We compared yearly charges of an ii ISA with other ISA providers. Results are based on published ISA charges as at 01/05/2026. Verified as accurate by The Lang Cat. Assumptions: 50% of ISA investments held in funds and 50% in equities, 2 equity and 2 fund trades per year. Other trading behaviours will result in different charges than those shown. This comparison covers a single year and does not account for investment growth or the impact of inflation over time. To ensure a fair comparison, fund manager charges have not been included. The information provided is for illustrative purposes only. For precise charges, we recommend contacting the ISA provider directly.

Why Nick transferred his ISA to ii

“I’ve been really happy with ii’s fees. It was the predominant reason I changed. It was just obvious. I knew I was going to get charged a flat rate and that’s what I was after. That’s why I’m with ii.”

Nick found his old provider’s percentage-based fees confusing. So he started looking elsewhere for a simpler, more cost-effective platform.

Simple plans with a simple fee

We have 3 plans with a wealth of benefits in each. Whichever plan you’re on, you’ll have everything you need in one place.

|

Core £5.99 per month Best for investors with less than £100,000 who want to access a wide range of investments and accounts. Portfolio limit up to £100,000 Benefits

|

Plus £14.99 per month Best for investors with over £100,000 who want access to lower trade costs and our most popular benefits - for themselves and their family. Portfolio limit No limit Benefits

|

Premium £39.99 per month Best for active investors who trade frequently and want the best features and rates available. Portfolio limit No limit Benefits

|

Choose your investment account

Personal Pension (SIPP)

Get pension peace of mind with our five-time Which? Recommended Personal Pension (SIPP). Invest yourself or let our experts handle your investments for you.

Stocks & Shares ISA

Get tax-free investing all wrapped up with our award-winning ii ISA. Take care of your own investments or let us manage them for you.

Managed ISA

Let us manage your ISA for you. Save time, leave it to the experts and feel confident in your investment goals - all for a low, flat monthly fee.

Trading Account

Invest in the markets you want and access a wide range of UK, US and international shares in a flexible account. It’s safe, secure and simpler investing.

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). If you’re unsure if a SIPP is right for you, please speak to an authorised financial adviser.

Summer’s brighter with our special offers

Summer’s in full swing - make it your time to invest with our latest special offers:

- £100 to £3,000 when you open a Personal Pension (SIPP)

- £150 free trades when you open an ii ISA or Trading Account

Offer ends 31 August 2026. New customers only. Terms and exclusions apply.

Important information: It’s important to take your time before transferring your pension. Make sure to consider what the best option is for you. Don’t transfer just to qualify for the offer, and don't rush any decision to meet the offer deadline. We periodically run offers, and there will likely be other opportunities in the future.

Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions.