Bond Watch: why currency hedging matters in fixed income

Alex Watts, senior investment analyst at interactive investor, explains how investors might minimise the effects of currency volatility on their fixed-income returns.

20th February 2026 10:48

by Alex Watts from interactive investor

Throughout the past year high-quality global bonds have been a good allocation for investors, supported by high starting yields and rate cuts across most developed markets.

While fluctuations in currencies can have outsized effects on an asset’s ultimate return - and 2025 certainly saw volatility in the currencies underlying these bonds - many retail investors will have been shielded from the effects of this volatility by the process of hedging.

- Invest with ii: Investing in Bonds | Free Regular Investing | Open a SIPP

Particularly I’m referring to changes in the relative strength of the US dollar given that it accounts for near to half of the currency exposure within global high-quality bond indices such as the Bloomberg Global Aggregate index.

It is because of this currency volatility – which has the potential to greatly surpass the volatility of the underlying bonds - that many active and passive investors will see it fit to hedge their currency exposure when investing in fixed income, rather than take on the foreign exchange risk between overseas and their own domestic currencies.

Why was 2025 significant for the US dollar?

Throughout 2025, the US Dollar index (which tracks the strength of the dollar versus a basket of other major currencies) fell by more than 9%. Sterling strengthened from $1.22 to $1.35. There’s a myriad of reasons for this, including:

- First, falling growth and interest rate expectations in the US. Meanwhile, UK growth expectations were already relatively low.

- Second, the perception of the dollar as a safe-haven currency being challenged by both mounting fiscal concerns (stoked by President Trump’s Big Beautiful Bill)

- Third, we may have seen a peak dollar allocation unwind as a more protectionist trade policy and more aggressive foreign policy have seen assets move elsewhere.

How do hedged classes work and why are they useful for bond investors?

Investors looking for a core bond allocation will typically be seeking to reduce risk.

Outside the realms of more niche and adventurous bond exposures, in normal years investors might expect bonds to deliver single-digit returns.

However, even major Fiat currencies (as we saw with the dollar and Japanese yen in 2025) are capable of substantial moves, while emerging market currencies can bring even more volatility.

- The Analyst: defence – how to play the new tech sector

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

While the same principle applies for equity funds - and has certainly been a factor recently for British investors buying US stocks - the relative importance of currency fluctuations is generally lower given the higher long-term expected returns (typically) on offer from equities compared with fixed income.

Why this matters

As a sterling investor, if you buy an unhedged class of a global bond index, you are effectively taking a long position in global bonds and in the foreign local currencies within versus your domestic currency.

Your return therefore will be the underlying bonds’ returns, plus (or minus) the foreign currency return. A strengthening of sterling relative to these currencies will therefore dampen your return while, all things the same, a weakening of sterling will do the opposite.

What a currency hedged class does is seek to neutralise the effects on returns of exchange rate fluctuations between the currency of the underlying bonds and the currency of the hedged class. This is done by engaging in forward contracts to lock in a future exchange rate – aiming to deliver you close to the underlying bond return.

- Bond Watch: what’s the market impact of Trump’s Fed chair choice?

- Are high fees chipping away at your investment returns?

While that is the basics of it, it’s worth noting that hedging itself can also add (or detract from) a fund’s overall yield, as well as levying costs both embedded in returns and sometimes reflected in different ongoing costs (often marginal) of share classes.

How can hedging affect investors’ returns?

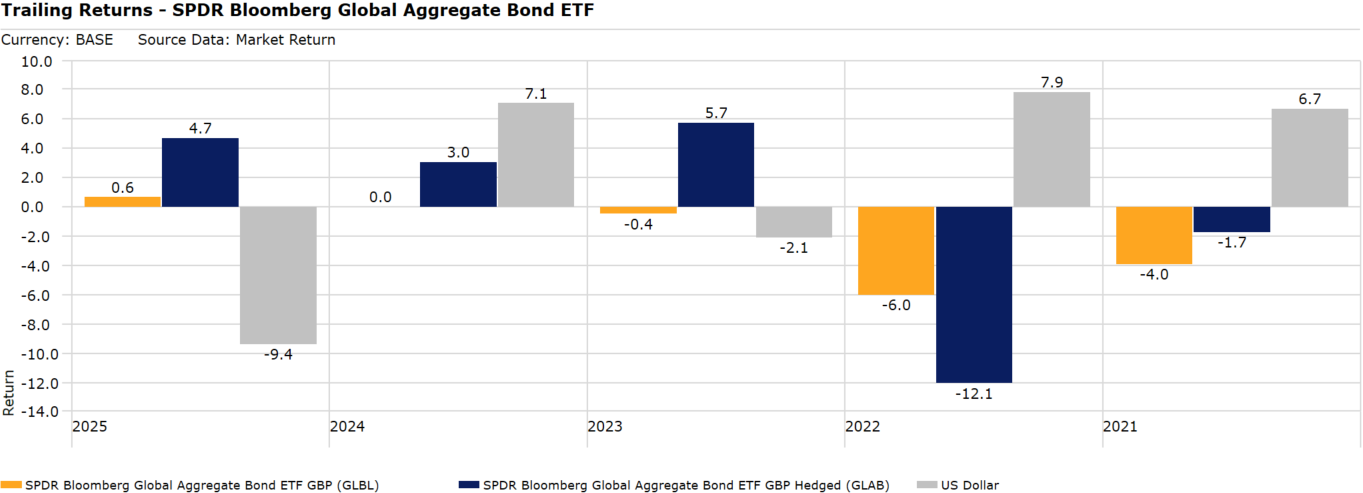

To give a simple example, in 2025 global bonds generated positive returns in their local currencies.

Using the Super 60’s SPDR Bloomberg Global Aggregate Bond ETF GBP H GBP (LSE:GLAB) as a proxy, we see that global bonds delivered a positive 4.7% return for investors in the sterling-hedged class (GLAB).

However, as the dollar – which I refer to given that it is the dominant currency in the global aggregate index – weakened (including versus sterling), investors in the unhedged class (SPDR Bloomberg Global Aggregate Bond ETF USD GBP (LSE:GLBL)) had their returns near neutralised, returning a meagre 0.6%. Both classes have the same low ongoing charge of 0.1%.

On the flip side, in 2022, bonds had an historically poor year as interest rates rose. However, as the dollar strengthened versus most currencies (and crucially for us UK investors - versus sterling), currency appreciation offset losses for unhedged investors (losing 6%). Meanwhile, sterling-hedged investors were exposed to the full 12% drawdown.

Source: Morningstar Market Returns in base currencies (GBP). Past performance is not a guide to future performance.

How is this be applied to a portfolio?

For investors not wishing to take an active position regarding currency movements, sterling-hedged share classes suit the purpose of reducing the effects of foreign currency fluctuations on returns when investing in non-sterling assets.

Of course, as seen in 2022, hedged share classes can underperform their unhedged counterparts at times as currency dynamics can support the unhedged investor.

However, for many investors seeking a core, diversified exposure to investment-grade global bonds – such as the low-cost SPDR Bloomberg Global Aggregate Bond ETF GBP H GBP (LSE:GLAB) mentioned above - minimising the effects of currency volatility on their fixed-income returns will be the desired outcome.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.