Why there's big potential upside for the airlines sector

After suffering significant share price declines, all the bad news is in the price for these carriers.

1st October 2019 14:23

by Graeme Evans from interactive investor

After suffering significant share price declines, all the bad news is in the price for these carriers.

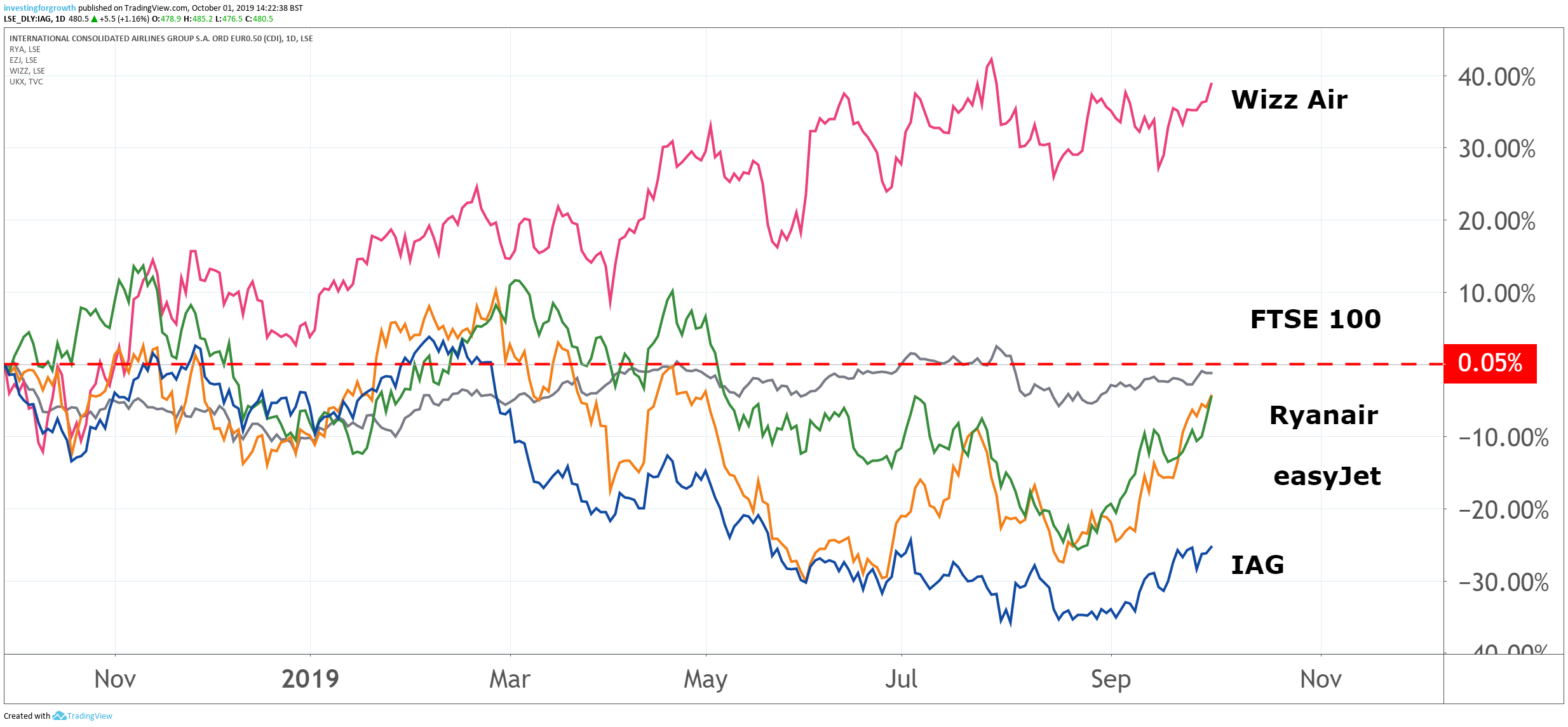

Shares in International Consolidated Airlines Group (LSE:IAG), Ryanair (LSE:RYA), easyJet (LSE:EZJ) and Wizz Air (LSE:WIZZ) have been cleared for take-off by a leading City bank after its analysts backed the European airlines sector to ride out the current Brexit and economy-related turbulence.

Bank of America Merrill Lynch's 'overweight' coverage of European airlines reflects its belief that the market has gone too far in pricing stocks for an outright recession on the continent. They don't subscribe to this economic scenario, meaning there's a big potential upside for the sector should key indicators turn positive as they expect in the coming months.

And with the basket of European airline stocks down by roughly 30% so far this year, the analysts regard now as an opportune time to gain exposure to high quality companies with strong balance sheets, such as British Airways owner IAG or Ryanair.

European airline price/earnings (PE) multiples are now 15% lower on average over the past year and trading at about 7.5x 2020 earnings — a discount to global airlines. The note said: "Although a worsening macro outlook is a headwind, we think this is reflected in shares with valuations at historical lows."

It's why the broker rates IAG, Ryanair and Wizz Air as a 'buy', with price targets of 660p (currently 482p), €13.5 (€10.91) and 4,100p (3,674p) respectively. Orange-liveried easyJet is rated 'neutral', with price target of 1,200p (1,172p).

Source: TradingView Past performance is not a guide to future performance

While the London-listed quartet face potential disruption in the event of a no-deal Brexit on October 31, Bank of America said the airlines had taken steps to ensure they maintain their EU operating licences by restricting ownership by non-EU nationals.

The bank notes that the UK represents the highest percentage of revenue for easyJet at 44%, followed by IAG at 32% and Ryanair with 22%. This makes them most exposed to a UK recession in the event of a no-deal Brexit, but a weaker pound is also likely to drive higher tourism to the UK and represent a positive for air travel demand.

Other Brexit factors to consider will be the translation of sales into euros, which will impact all but easyJet, as well as the potential disruption to travel trends caused by visa issues.

High fuel costs, which contributed to lower margins in the first half of this financial year, are expected to be less of a headwind in 2020. Brent crude and jet fuel market prices have declined this year, but high levels of hedging mean it is taking longer for European airlines to benefit.

Employee costs are the second-biggest outgoing, with these expected to increase modestly in the year ahead.

The potential for further sector consolidation should be another positive for the surviving European airlines after a record year of collapses in 2018 when seven carriers filed for bankruptcy. This trend has continued in 2019, with Thomas Cook the most recent airline operator to go under.

Despite these failures, Bank of America notes that the European market remains fragmented, with the top five carriers holding a 63% share of seats — up from 41% a decade earlier but still well below the US market.

It believes further Europe consolidation is inevitable but driven by airline failures rather than M&A activity. The bank quotes Ryanair boss Michael O'Leary as predicting that there will be four very large airlines in Europe by 2024.

Bank of America added: "Fewer industry participants mean fewer market share battles and less destructive pricing behaviour, which should help the airlines to deliver sustainable profitability."

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.