Final salary pensions: When you should consider transferring

Ceri Jones examines the pros and cons of final salary transfers following a boom in interest since 2015.

3rd May 2019 13:20

by Ceri Jones from interactive investor

Ceri Jones examines the pros and cons of final salary transfers following a boom in interest since 2015.

Around 100,000 final salary pension scheme members traded in a guaranteed income in retirement for a cash lump sum last year, according to the Financial Conduct Authority (FCA).

For many, the motivation is that a transfer out of an employer's final salary scheme allows them to take advantage of the rule allowing people aged 55 and over to take 25% of the fund tax-free – a tidy sum when the average transfer exceeds £250,000.

However, transferring out of a final salary scheme is not easy and is about to become even harder. The biggest difficulty is that anyone with a transfer value of £30,000 or more who wishes to switch is required to take professional advice from an independent financial adviser, and to all intents and purposes the transfer cannot go ahead unless the adviser agrees it is a suitable course of action.

In most cases, however, advisers do not believe the best decision is to transfer. People tend to underestimate the value of the guaranteed pension given up, because they do not appreciate the cost involved in inflation-linking the final salary benefits (potentially over decades), or dependents’ benefits.

The media has been full of warnings that transfers could become a mis-selling scandal in the years ahead, perhaps if people exhaust their funds too rapidly or fail to achieve the investment returns expected. Furthermore, much of the advice given by IFAs so far has been dodgy.

When the FCA investigated the market at the end of last year, it found that less than half the transfer recommendations reviewed were suitable. Nearly 5,000 transfers were carried out last year by enthusiastic advice firms that subsequently exited the market after the regulator exposed weaknesses in their recommendations.

Pension transfer values fluctuate month to month

Notes: This shows the XPS Pensions Group Transfer Value index since April 2015. The XPS PGTVI tracks the transfer value provided to a final salary scheme member aged 64 expecting a pension of £10,000 at age 65, increasing in line with inflation. The graph shows the average transfer value in recent years, and demonstrates how much your transfer value could fluctuate from one month to the next.

Complaints

As complaints and regulatory scrutiny rise, many reputable financial advisers are now reconsidering whether or not to advise on transfers at all. Professional indemnity (PI) premiums for advisers who conduct this business have also become exorbitant. Those relatively few advisers who offer advice on transfers will only be able to cope with a limited number of clients and will prefer to advise the more lucrative ones. Some only offer this advice to existing clients.

At the same time, demand for advice on transfers is growing as the choices on offer become more widely known, whereas most demand to date has come from finance industry professionals. With so many advisers fleeing the market and demand booming, it may be difficult to obtain independent advice at all.

"People with transfers at the lower end, such as £30,000 to £100,000, will struggle to find an adviser," says Craig Rimmer, policy lead for the Pensions and Lifetime Savings Association.

"There will be a limit to how many clients an adviser can service properly."

This difficult situation is exacerbated by regulations that prohibit an adviser meeting with you to give informal preliminary guidance. Even if it becomes obvious after 15 seconds that a transfer would be inappropriate, the adviser still has to go through the process of issuing a full individual report.

However, the situation is improving, points out Steven Cameron, pensions director at Aegon. "The very worst advice has been largely confined to four IFA firms that have gone out of business," he says. "From the customer's perspective, advice has fallen short and those people must be compensated, but we need to distinguish what happened in the past and the advice being given now."

If you do manage to find an adviser prepared to sanction your transfer, a typical charge would be 1% of the transfer value or a set fee of £2,500- £3,000. Some charge significantly more for new customers, frequently 2-3%.

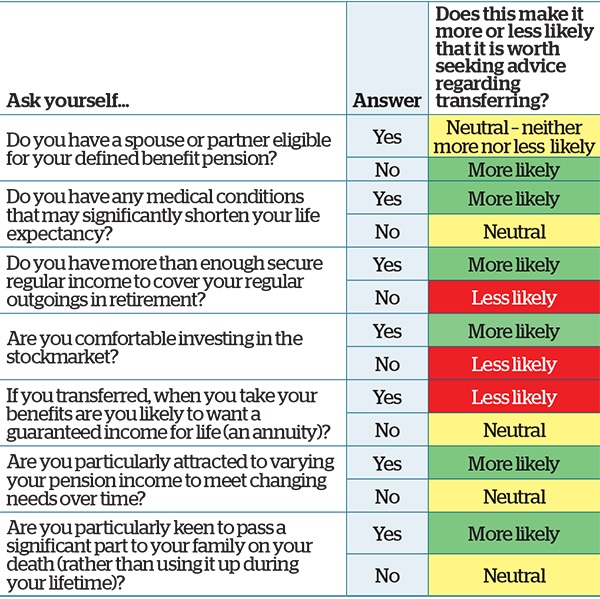

The table below should give you an idea whether a transfer might be in your best interests.

Many people find it useful to compare their individual life expectancy with the scheme average, by completing a personalised predictor such as insurance company Aviva.

One issue in the news is the viability of some occupational pension schemes in the light of massive deficits and high-profile collapses such as that of British Home Stores.

If your employer's scheme goes bust, then the Pension Protection Scheme will cover up to 100% if you are already drawing benefits, capped at £39,006 a year, or up to 90% of your pension if you were below your scheme's normal pension age when the employer became insolvent.

Should I seek advice on transferring?

These questions may help you decide whether you wish to seek advice on transferring from a final salary scheme. If your answers include a number of greens it may be worth exploring further. If you have one or more red answers, then it is probably less worth exploring.

Source: Aegon

Long-serving members

The compensation has recently been improved for long-serving pension scheme members, who were previously capped, but will now receive an additional 3% for each year above 20 years of scheme membership.

Payments relating to service from 6 April 1997 rise in line with inflation, subject to a maximum of 2.5% a year, but pensions relating to service before that date don't increase.

While the employer's strength, or covenant, is not generally considered a sufficient reason to transfer, it may be a consideration for members of very weak schemes who have built up very generous benefits and would therefore suffer if they fell back on the lifeboat fund.

The next, and perhaps most significant, challenge of the piece is that the cash sum transferred must be invested in a registered pension scheme to produce income, but investment returns going forward are unlikely to be as good as they have been in recent years.

Average US investment returns over the next 10 years are likely to be in the region of 3-5%, according to Vanguard. Factor in inflation – fortunately less than 2% – and the real rate of return could be under 3%.

This falls far short of what investors have become accustomed to in the bull market following the 2008 rout, with the world-dominating S&P 500 returning 22% last year. (Rattled by Brexit, the FTSE 100 unfortunately plummeted by 12.5% during 2018, wiping out more than £240 billion and demonstrating just how easy it is to lose money if you pick the wrong markets or investments.)

Many believe that the gargantuan transfer values on offer provide some leeway for error. A typical transfer is around 22-24 times the projected annual pension given up under the final salary scheme, but several other factors are involved and schemes' generosity varies wildly. Some offer 30 or 40 times the projected pension, while others give appreciably less.

Transfer value

This means someone giving up a guaranteed pension of £25,000 per year could potentially have a transfer value of £1 million. Even a relatively modest pension of £10,000 a year may prove more than a person's house, explains Alex Bates, a consultant at XPS Pensions Group, so it is little wonder that so many are looking to cash in their pension.

Transfer values also fluctuate in line with gilt yields, the measure used by the scheme's actuary to produce a figure that reflects the returns expected from the market in future.

Gilt yields have an inverse relationship with transfer values and have been at rock-bottom levels for a few years, making transfer values unlikely to rise much in future and much more likely to drop – worth bearing in mind, given that the transfer process can take a few months.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.