Stockwatch: a FTSE 250 company in buying territory

Buying by directors suggests confidence in the boardroom, but despite risks, there are a number of reasons why analyst Edmond Jackson likes this share.

12th May 2026 11:01

by Edmond Jackson from interactive investor

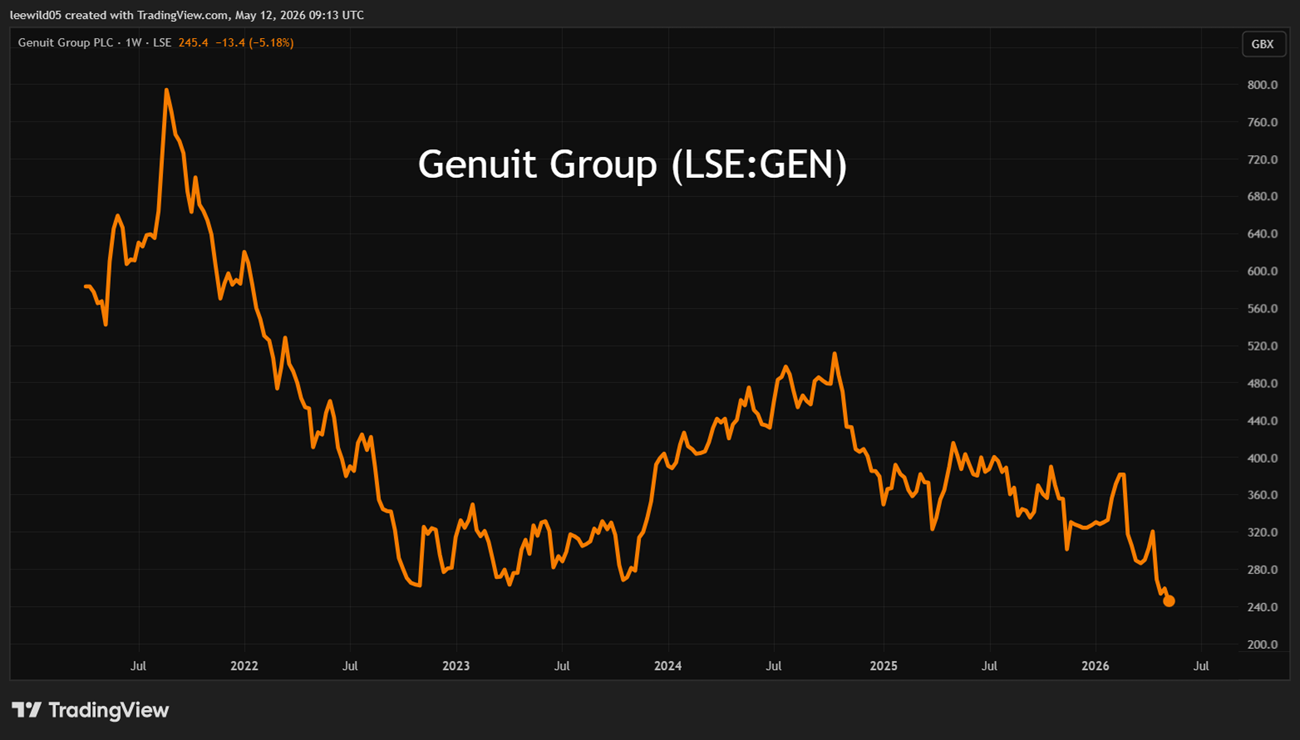

It is interesting to consider mid-cap stock Genuit Group (LSE:GEN) which, at 246p and lacking support, is re-testing a 2016 low around 230p having hit a 786p high in 2021 then failed to sustain a recovery rally in 2025.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

The shares are at the low end of their historic range amid concerns about UK economic weakness affecting construction. This company is the old Polypipe which founded in 1980 and floated in 2014 as a manufacturer of PVC piping and heating/ventilation systems, seen as closely tied to the housing market. Yet a new CEO since 2022 has arguably made the group stronger and more efficient, achieving synergies between what were sporadic acquisitions before his tenure.

Source: TradingView. Past performance is not a guide to future performance.

Call it woke but Genuit has attempted to bury Polypipe in the sense it weirdly now insists it is simplified to two divisions – Water and Climate. That’s despite the legacy PVC piping business, now called Sustainable Business Solutions (SBS), constituting 40% of group revenue. Such semantic playing around – including the generic “Genuit” name-change that must have cost a bit – tempts me to strip it aside for the underlying numbers and substance.

Strong positions in relatively secure markets imply durability

Yes, there is near-term UK recession risk; for example, Barclays today cites households cut their spending at the fastest rate in 18 months as the Middle East crisis prompted cost-of-living fears and higher fuel costs required substitutions.

However, this group does have medium to longer-term legislative tailwinds in water and climate. It’s also stronger because some smaller manufacturers have withdrawn.

Its modern mantra is “a UK provider of sustainable water, climate and ventilation solutions” for addressing climate change and regulations, especially for the water industry.

SBS produces plumbing systems primarily for new-build construction, hence you can argue housebuilding is at near-term risk but has medium to longer-term recovery prospects. Genuit’s scale, for example ability to produce PVC pipe locally thereby avoiding expensive transport costs, is a competitive advantage versus smaller factories.

Water Management Solutions (WMS) at around 30% of group sales, produces storm-water drainage systems for civil and residential applications. This side should benefit from the UK industry’s eighth five-year regulatory cycle running from 1 April 2025 to 31 March 2030. Managed by Ofwat, it features a record £104 billion investment, a 75% increase over the seventh programme, focusing on upgrading ageing infrastructure, cutting leakage by 25% and reducing sewage outflows. Effects are said to manifest from the second half of 2026 onwards.

- Promising signs at Vodafone but Germany a thorn in the side

- Insider: directors pile into FTSE 100 stock at huge discount

Another 30% of revenue derives from Climate Management Solutions (CMS), supplying ventilation and heating systems for residential and commercial new builds. This side apparently should benefit from the Future Homes Standard and Awaab’s Law raising ventilation requirements in new builds and social housing.

Presently, the group has around 20% of unutilised capacity which is a concern but does position Genuit to benefit from a housebuilding recovery. It also has a significant cost advantage in procurement as one of the largest purchasers of polymer in the UK.

The new CEO from 2022 has undertaken streamlining such as closing seven facilities, reducing management layers and consolidating polymer purchasing. It’s why operating margin recovered from 8.5% to 10.6% in 2023 and was 11.6% last year, and management is targeting 20%. Admittedly, 2025 revenue was below 2022 despite acquisitions.

Genuit Group - financial summary

| Year end 31 Dec | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Turnover (£ million) | 399 | 594 | 622 | 587 | 561 | 602 |

| Operating profit (£m) | 30.4 | 67.1 | 53.0 | 62.0 | 59.2 | 69.7 |

| Net profit (£m) | 18.5 | 41.0 | 36.5 | 38.5 | 33.5 | 45.2 |

| Operating margin (%) | 7.6 | 11.3 | 8.5 | 10.6 | 10.5 | 11.6 |

| Reported earnings/share (p) | 8.4 | 16.5 | 14.6 | 15.4 | 13.4 | 17.8 |

| Normalised earnings/share (p) | 11.0 | 19.7 | 28.4 | 25.4 | 22.9 | 24.1 |

| Operational cashflow/share (p) | 24.2 | 30.2 | 34.7 | 39.2 | 41.9 | 40.5 |

| Capital expenditure/share (p) | 11.4 | 13.9 | 17.5 | 13.8 | 10.6 | 11.9 |

| Free cashflow/share (p) | 12.8 | 16.2 | 17.2 | 25.3 | 31.2 | 28.7 |

| Dividend per share (p) | 4.8 | 12.2 | 12.3 | 12.4 | 12.5 | 12.9 |

| Covered by earnings (x) | 1.8 | 1.4 | 1.2 | 1.3 | 1.1 | 1.4 |

| Return on total capital (%) | 5.2 | 7.6 | 5.9 | 7.3 | 6.9 | 7.2 |

| Cash (£m) | 44.1 | 52.3 | 50.0 | 17.0 | 43.6 | 44.8 |

| Net debt (£m) | 27.7 | 166 | 166 | 149 | 129 | 208 |

| Net assets (£m) | 501 | 618 | 627 | 637 | 643 | 663 |

| Net assets per share (p) | 219 | 249 | 252 | 255 | 258 | 264 |

Source: company accounts

Mind how net debt rose last year from £129 million to £208 million in relation to £106 million spent on acquisitions, and the £11.5 million net interest charge took 16.5% of operating profit – the charge likely being higher this year albeit against profit measures 50% or more higher, for what consensus is worth.

Last March, management said: “Subdued market conditions in the fourth quarter have continued into the first quarter of 2026 as expected, albeit with some positive signs on order intake”. Prolonged wet weather had impacted construction site activity in January and February; also there was a general caveat about “the evolving situation in the Middle East” and its macro effects “difficult to assess at this time”.

Not surprisingly, the shares have been subject to stop-loss selling given no positive catalysts and investor de-risking.

Projected recovery with 12% earnings growth and 9% in 2027

The downtrend is at odds with broker forecasts anticipating around £70 million net profit this year (up 54%) and £75 million in 2027, although it’s unclear how realistic this is even if acquisitions prove earnings enhancing.

Such a scenario implies a forward price/earnings (PE) ratio of 9.1x, easing to 8.3x, and with the dividend yield also expected to rise from 5.5% to 5.8% (assuming a share price of 246p per share) with twice earnings cover both years.

Mind the longstanding adage how some of the riskiest shares are cyclicals apparently offering value ahead of a downturn.

Buying into Genuit now therefore hinges on what extent you think its legislative tailwinds can offset near-term risk in housebuilding.

The last trading update came with the 10 March annual results, before Barclays warned of a hit to consumer spending. How might that affect home buying, especially if interest rates have to rise versus inflation?

Sensitivity to macro was made clear after Genuit enjoyed a promising first half of 2025, only for its businesses to be impacted by uncertainty surrounding last October’s Budget, especially in the fourth quarter.

Yet management proclaimed exposure to “higher growth market segments” mitigated softness in UK construction, such as cooling systems for multi-occupancy residential developments, and also “blue-green” roofs for water attenuation. Legislation on heating and ventilation (anti-mould) plus two acquisitions around £50 million each are said to offer scope to leverage sales.

Is this enough to buck potential wider market weakness? One construction industry interview I recently heard on the radio alleged a better return from bank deposits currently than building projects.

That said Genuit shares are trading around 1x annual sales and a small discount to 264p net asset value per share, if you are willing to recognise the goodwill element on acquisitions that constitutes 102% of net assets.

When Polypipe floated in 2014 it was said to take advantage of a UK construction recovery. No new capital was raised, but rather to help a second private equity owner (2005 and 2007) sell down. I am still inclined to think the current market valuation is well into the region of what a private buyer would be prepared to pay.

Also, the table shows the record of free cash flow per share as plenty strong relative to earnings, hence supportive of a buyout even though net debt is already significant.

Directors buy into Genuit’s de-rating

Last March, three directors bought a total £61k worth of shares at 281p to 285p. The market price is now 13% lower.

There is a pattern of buying: nearly £120k worth by four directors last November at 300-313p, and in December 2024 three directors bought £43k worth around 290p. There has been further annual buying especially around the 250p or so levels reached in late 2022/early 2023.

- The Income Investor: prospects for Taylor Wimpey and Persimmon

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

A sceptic might say that while it’s good to see directors make quite regular share purchases rather than rely on risk-free options, their trading is not exactly a reliable guide to timing. Yet implicitly they have backed their sense of value.

I apply a medium to longer-term “buy” rating with an obvious qualification about risk of further UK construction weakness.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.