Bond Watch: how fixed income is faring as Iran war grinds on

Most bonds have failed to act as a safe haven as disruptions pushed energy prices sharply higher. Alex Watts looks at performance, and considers the differences compared to the 2022 bond market sell-off.

27th March 2026 10:51

by Alex Watts from interactive investor

As the war in Iran continues and flows through the Strait of Hormuz have been curtailed, falling oil exports (among other resources) have sent energy spot and futures prices higher.

Brent crude oil has spent much of the past two weeks above $100 dollars per barrel, only softening now as the market digests conflicting and often incoherent talks of a wind-down of tensions.

- Invest with ii: Investing in Bonds | Free Regular Investing | Open a SIPP

Against this potentially inflationary backdrop, most bonds have failed to act as a safe haven as disruptions have pushed energy prices sharply higher - forcing yields upward and price downward. As markets have scaled back projections for imminent policy easing, yields at the front to mid-part of the yield curve have reacted most acutely to changing central bank challenges, but yields have drifted higher across maturities, disproportionately weighing on prices of longer-dated bonds.

How have fixed-income markets performed?

Government bonds suffered as markets repriced policy paths, with near-term rate cut expectations quelled. Last week, the Federal Reserve and Bank of England, which were on easing trajectories, as well as the European Central Bank and Bank of Japan, held rates.

The Bank of England’s Monetary Policy Committee noted “a larger or more protracted shock […] would require a more restrictive policy stance” but that easing likely would continue if the shock is short-lived, while Federal Reserve chair Jerome Powell and members of the Federal Open Market Committee balanced the struggle of both tariff, and now energy-induced inflation, with weak job creation.

For corporates, rising input costs compress margins and threaten credit quality and spreads - in this case referring to the yield premium of corporate bonds over government bonds of the same maturity, which typically widens as perceived credit risk increases. Sectors particularly at risk include energy-intensive sectors, such as utilities, transport, manufacturing, mining and chemicals.

- Five things to know about bonds amid current geopolitical volatility

- How to trade the greatest late-cycle bull market in history

Fixed-income returns have been weak since the first US aggressions at the end of February. Over the past month, there have been declines across government and corporate bond indices, with virtually nowhere to hide outside of cash-like money market funds.

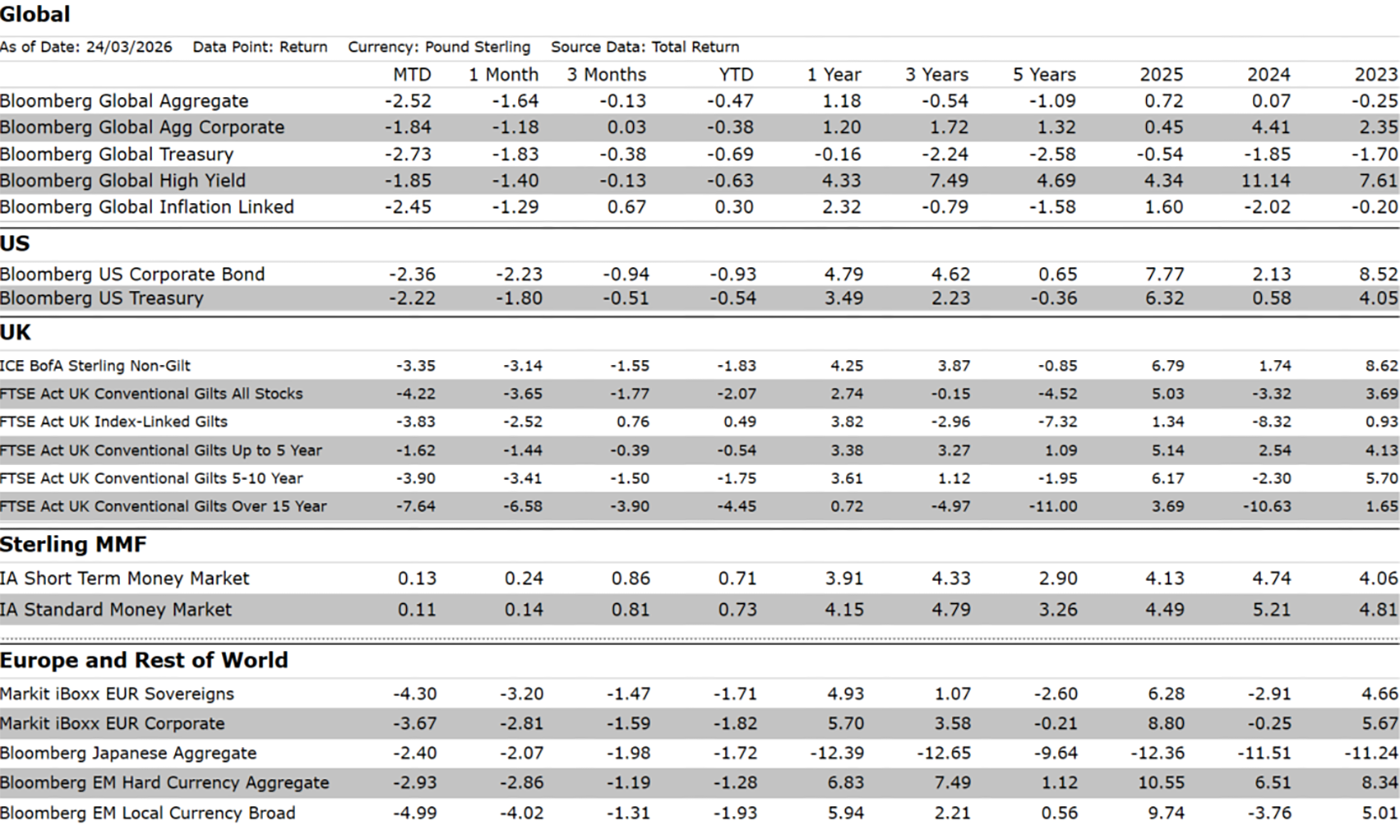

Throughout the month to 24 March, the Bloomberg Global Aggregate fell 2.5%, with government bonds underperforming (-2.7%). Longer maturities, prices of which are typically more volatile, have generally performed worse as 20-year Treasuries and gilt yields touched 5% and 5.6% this week, but even 1-5 year issuances have delivered negative returns on aggregate.

Notably the sell-off has been pronounced in the UK where conventional gilts fell by 4.2% and inflation-linkers by 3.8%. Unlike the US, the UK is particularly exposed due to weak energy security. Reliance on imports and limited storage mean global price shocks quickly pass through into domestic inflation.

Will this play out like the 2022 bond meltdown?

While current bond volatility may feel reminiscent of 2022, the underlying drivers and the likely responses from central banks are fundamentally different. It’s worth remembering that monetary policy is typically more effective at tackling demand-induced inflation rather than supply-side.

The 2022 bond (and equity) sell-off saw interest rates rise significantly from very low levels as imported inflation from the Ukraine war met overheating Western economies. During the last time the Federal Reserve and other developed market central banks were tightening, the world was unwinding from Covid. For example, UK unemployment had fallen below 4%, PMI (the Purchasing Managers’ Index) and economic growth had rebounded, and CPI was rising to reach a double-digit year-over-year reading. The picture in the US was comparable.

Now, demand is more fragile. We may have the threat of resurging supply-side inflation owing to higher oil, gas and other energy costs but now it’s alongside sluggish economic growth prospects (in the UK especially), rising unemployment (5.1% and 4.4% in the UK and US respectively) and, crucially, a base of quite restrictive monetary policy, with UK interest rates now much higher than 2021 levels.

- What March’s interest rate decision means for your retirement income

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Central banks may be less likely to attempt to tackle this inflation by strangling excess demand that doesn’t exist – doing so would exacerbate recession risk. So, while yields across the curve in the US and UK have shifted upwards - and despite the war in the Middle East adding a new dimension to Federal Reserve and Bank of England rhetoric - markets are only pricing a 6% probability of any increase in interest rate in the US in April.

Unlike 2022, when the Ukraine shock catalysed a full hiking cycle from near-zero rates, the current sell-off likely reflects a late-cycle repricing, implying a disruption to easing expectations but not a full-blown hiking cycle. While bonds have struggled as a hedge so far, investors can still navigate the volatility strategically.

If energy prices stabilise or inflation moderates, yields may plateau, offering opportunities to lock in attractive returns. Allocations to high-quality government and investment-grade corporate bonds remain prudent, while shorter-duration bonds can help mitigate interest-rate risk in the near term.

While term premium may continue to rise alongside uncertainty, exposure to duration could be considered once inflation signals show signs of peaking and the situation in the Middle East appears clearer. Sectors less sensitive to energy costs, or corporates with strong balance sheets, may provide relative stability within credit portfolios.

Overall, disciplined, high-quality positioning can help preserve capital and benefit when bond markets regain their traditional defensive role.

Source: Morningstar. Past performance is not a guide to future performance.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.