How to trade the greatest late-cycle bull market in history

Conflict in the Middle East has tipped many global stock markets into the red for 2026, leaving investors unsure of how to proceed. Analyst John Ficenec discusses what they should do now.

25th March 2026 11:48

by John Ficenec from interactive investor

Investors suffering from a severe case of whiplash from financial markets in the past few weeks should strap themselves in because volatility is a classic sign of a late-cycle bull market, and there are some important techniques for preserving wealth during the turmoil.

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Bull spotting

First, we need a quick definition of terms to explain the current investment landscape. A bull market being a 20% increase, that once satisfied can continue onwards and upwards for years. The evil twin, or the yin to the bull market’s yang, is the bear market which is classified as a 20% fall lasting longer than two months, with a correction being a drop in prices of over 10%.

I would strongly argue that we are currently in the longest bull run in stock market history. The reason for this is because I would exclude the last 20% drop during the Covid-19 pandemic. Yes, stock markets around the world fell by 20% after the World Health Organisation (WHO) declared an emergency on 20 February 2020, but they recovered rapidly. In the UK, the blue-chip FTSE 100 index spent only two months and two weeks in a bear market, and in the US the S&P 500 never qualified as prices recovered above the 20% threshold within the two months.

The other important factor was that the global pandemic was a non-financial external shock, and not part of the normal cycle. Previous bear markets have been caused by the inner financial workings of a market cycle, such as excessive loans for the 2008 banking crisis, speculative valuations for the 2000 dotcom bubble, and excessive valuations in the run up to Black Monday in 1987.

- Stockwatch: a FTSE 100 stock to play end of Iran war

- AIM market winners and losers since Iran war broke out

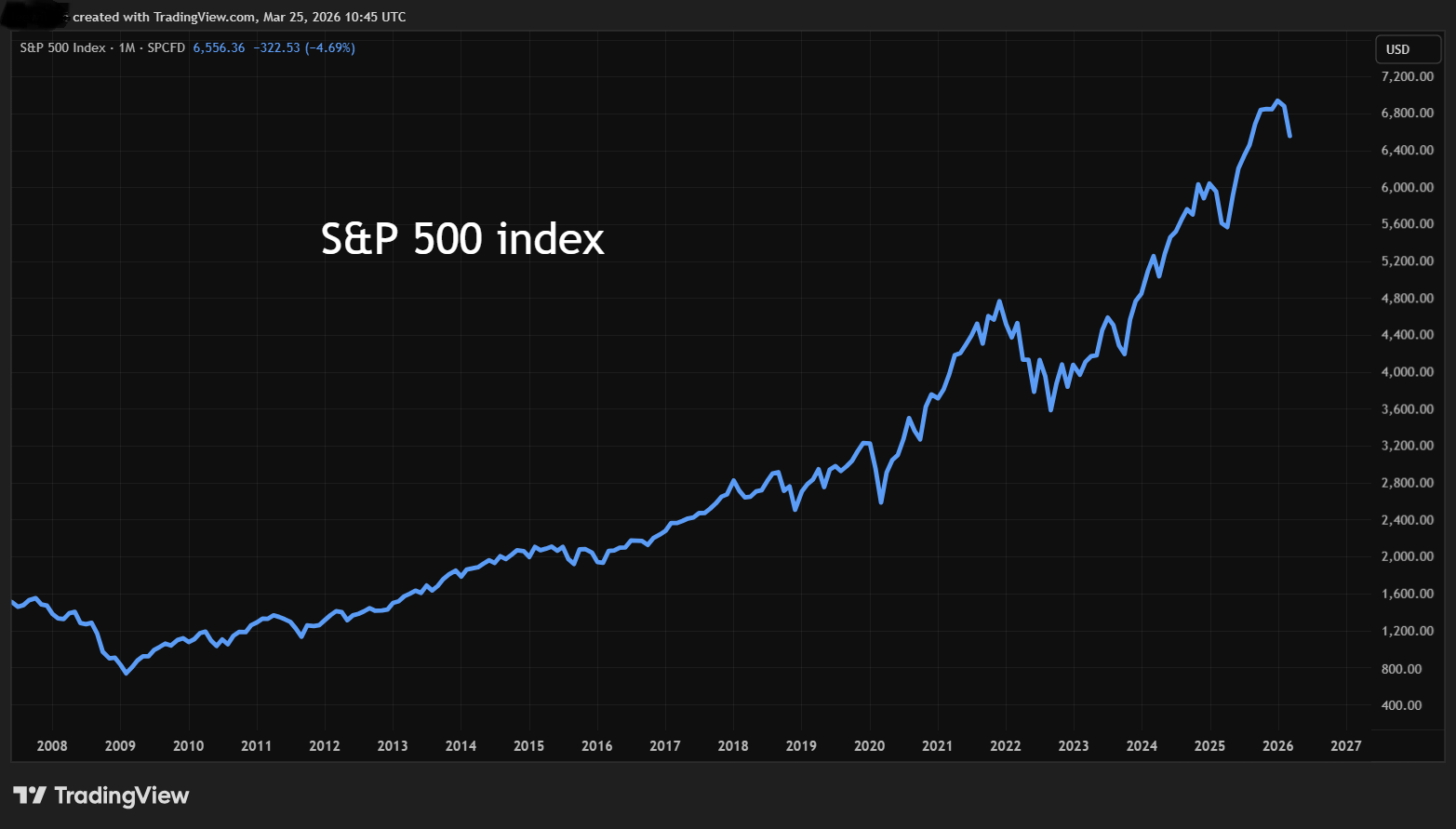

So, adjusting for the short sharp dip caused by Covid-19, this grand old bull is now entering its 18th year. The FTSE 100 is up 190% from its low of 3,460 on 3 March 2009, and the S&P 500 is up 880% from its low of just under 667 on 9 March 2009. The characteristics of this market have been low interest rates, loose money supply, and governments always on hand with a bailout.

Source: TradingView. Past performance is not a guide to future performance.

Late-cycle landscape

There are other reasons why the financial markets are demonstrating all the hallmarks of being in the later stages of its current cycle. A bull market starts not with a bang, but a steady accumulation by investors. Share prices don’t rocket up, they slowly and steadily rise.

The next phase is momentum as more buyers enter the market. This is arguably the most boring, and lucrative phase for investors, the classic “buy the dip” period as prices relentlessly march on upwards.

The final phase is the distribution, or blow out, and it increasingly looks like what we have today. The volatility in markets starts to increase as more and more money chases smaller returns. The thrill and excitement picks up, as any corrections are quickly recovered and there is euphoria that a new paradigm has been reached.

As money that has been made elsewhere during the bull market looks for a new home, there is what increasingly looks like the fluid dynamics concept of slosh. Vast sums of money, with the fear of missing out, or FOMO, piling into asset classes chasing returns.

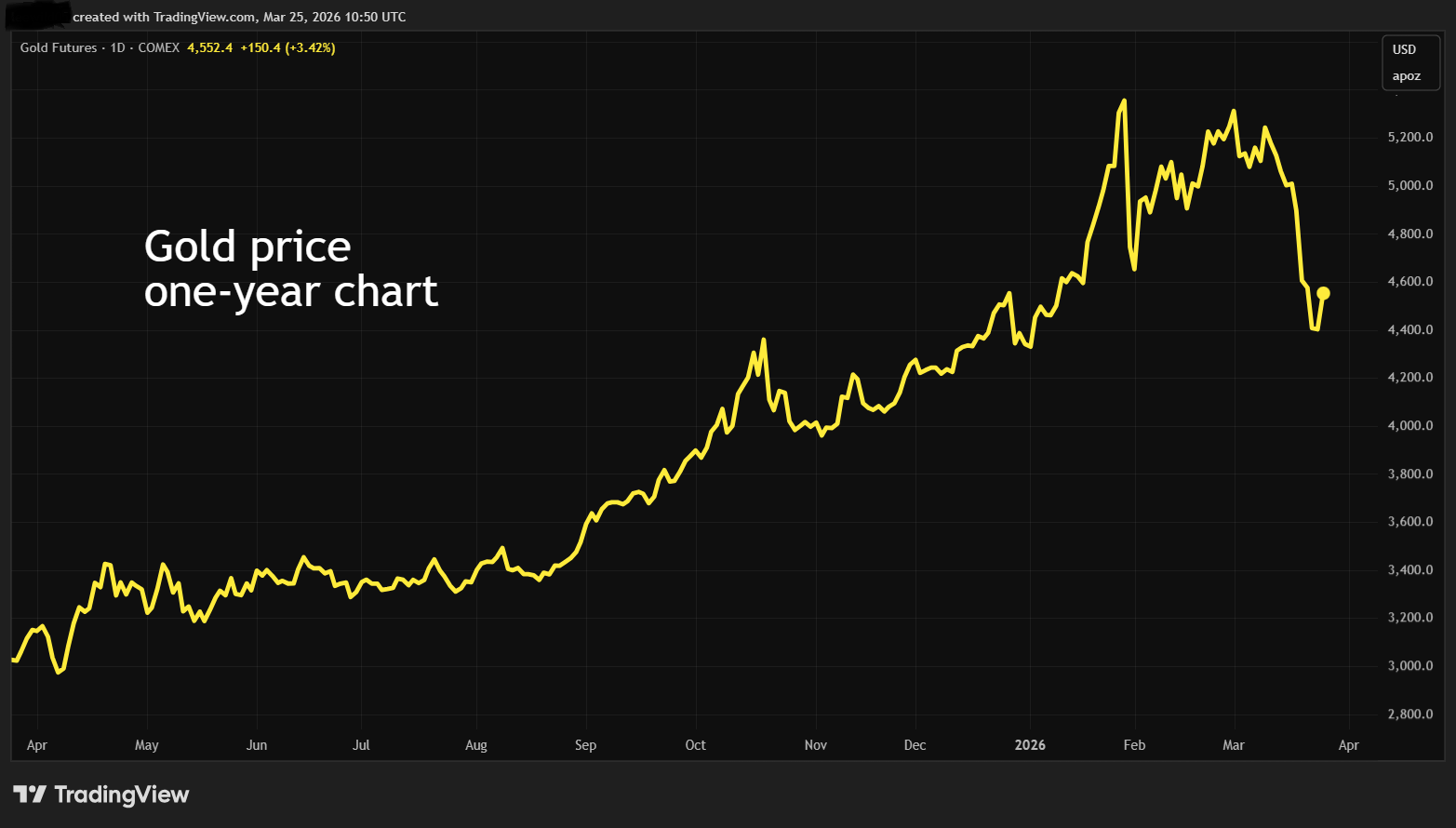

During the past 12 months this has been seen in a number of different places, such as gold which stopped being just inflation and monetary debasement protection, and became a speculative asset in its own right, doubling in price last year. Silver then became the next gold, and because it’s a smaller less liquid market, the price tripled in under a year. Bitcoin, the perennial speculators’ choice, also shot up to an all-time high in October of last year.

Source: TradingView. Past performance is not a guide to future performance.

Weaker pillars

The problem is that while exciting, the pillars supporting this late-stage bull are becoming somewhat shaky. Retail investors have been a key component, buying heavily after Trump’s Independence Day tariffs, initially driving a recovery and then taking it to fresh highs. The question is how much longer they can keep stepping in to support every sell-off.

Another area that is no longer as sure-footed as it was 12 months ago is the US tech sector and the artificial intelligence (AI) story. Backed by staggering spending announcements on AI infrastructure, chip makers such as NVIDIA Corp (NASDAQ:NVDA) soared, and any tech company linked to AI basked in the glory. Most of the 16% return of the S&P 500 in 2025 was driven by technology stocks, without them the return would have been a more modest 6%, according to RBC Markets. Once a surefire route to please investors, Amazon.com Inc (NASDAQ:AMZN)’s latest spending plan resulted in a sell-off. Even the mighty Nvidia saw a muted share price reaction to blockbuster profits and huge investment plans alongside its annual results last month.

- Unloved adventurous areas that warrant a closer look

- Want to pay less tax? Here are five allowances to use by 5 April

The US economy has repeatedly surprised with its resilience, but there are signs it is running out of steam. The US economy slowed to 1.4% annualised growth in the last three months of 2025, as the government shutdown hurt business, bringing growth for the year as a whole down to around 2.2% from 2.8% in 2024. The US jobs market is still weak, with non-farm payrolls falling by 92,000 in February and the unemployment rate increasing to 4.4%. The number of jobs on offer is still near a four-year low, the weakest job growth outside of a recession.

China can no longer do the heavy lifting either. In 2006, the Chinese economy was worth around $2.79 trillion, and as it increased tenfold to end 2025 at $20.65 trillion, it dragged the global economy with it. The Chinese economy has seen GDP growth slow from an average around 10% in 2006 to 4.5% in the last three months of 2025, and the growth target has been set at between 4.5-5% in the five-year plan, its lowest level since early 1990.

Trading tactics

So, presented with increasingly wild market swings and an uncertain outlook, what are the options? There could be a temptation for investors to look at insulating losses through buying exchange-traded funds (ETFs) such as Xtrackers FTSE 100 Short Daily Swap ETF 1C (LSE:XUKS). What this does is seek to offer the opposite performance of the FTSE 100 index, so if the index falls by 2% one day, then the price of the ETF gains 2%.

Investors must be very careful and clear that far from buying insurance or protection, it is just additional risk within their portfolio. Because now they hold a long position in companies within their portfolio, as well as an additional bet against the FTSE 100. With the UK blue-chip index being heavily weighted towards oil and gas, they could find themselves losing money on shares and watching a short FTSE 100 ETF lose money as well, just compounding the problem they were trying to avoid.

- Stockwatch: hedges and opportunities amid the crisis

- Funds worth watching as Middle East conflict grinds on

This scenario is similar to what famously happened to credit funds during the 2008 crash. Back then, funds that were holding billions in what they thought were low-risk loans to investment-grade companies, sought to protect themselves from losses by shorting, or betting against low-quality junk bonds in the belief that they would fall first and fastest in a market downturn. Actually, the opposite happened, there were no buyers for junk bonds, so the prices didn’t fall by as much, whereas the more liquid market for investment-grade debt saw prices collapse. The investment professionals lost on both sides of the position, causing funds to collapse.

With that in mind, it becomes more important to consider what stage you are at in your investment outlook and what your end goal is from the portfolio.

Young investor building a portfolio

A big risk here is to go chasing fads such as gold, silver, AI, and buying near the top. The painful experience of losses could put you off investing at the most important stage. To ward against this, the best approach is to spread any investment over time, or pound cost averaging. If, for example, £100 is invested in one go it can lock in one high price, but if it is split £50 first and then £50 in a month or two, it averages to a lower price if the market is falling.

The other essential approach is diversification across sectors and asset classes. While technology stocks can look attractive, it’s just as important to ensure there is exposure to mining, oil and gas, industrials, pharmaceuticals, insurance, banking and consumer staples.

Middle-age building pension pot

Here it becomes tricky as there are likely to be substantial gains in some areas. The key here is not to panic and sell, or try and lock in gains by raising cash. The starting point should be that nobody knows where markets are headed. If there are 20 years left till retirement that is more than enough to ride out any falls. It should also be the period of increasing pension contributions.

Approaching what looks like the later stages of a bull market, the best approach is to ensure the portfolio is balanced and check nothing has gained too much and has grossly increased its weighting. If so, there is nothing wrong with raising a bit of cash and sitting and waiting.

- What interest rate decision means for your retirement income

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The shopping list is the most powerful tool in this situation. Build up a list of companies that have attractive returns and then sit and wait. Slowly monitor the list and deploy cash over a period through pound cost averaging.

Approaching or already in retirement

This is one of the trickiest times psychologically as there is the fear of losing what has been put aside over a lifetime of work. Recent market movements highlight some very common errors though. Imagine selling shares and investing in a defensive asset such as gold just as the price collapses.

Another risk would be to sell shares and buy fixed-income like UK gilts. The problem is that since the start of the year yields on the benchmark 10-year gilt have risen sharply, meaning prices have fallen on fears of higher oil prices impacting the UK economy. So, again, attempting to protect your pension could expose you to losses.

Realistically, and taking the UK state pension age of 66, most people still have an investment horizon of over 20 years. The best approach would be to do nothing at first, given making a panic decision could just expose you to losses. If the investment horizon is over five years, you can ride out the worst of any falls.

It is painful to watch any investment fall in value, but it perhaps needs to be put in perspective. The later stages of a bull market will result in some wild swings. As Trump has proven time and again, it is impossible to anticipate how his policy will impact market. But it is important not to lose sight of what has returned most of the gains in the portfolio for most investors - holding for the long-term dividend income and capital gains, not short-term speculation.

John Ficenec is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.