Did strategic bond funds live up to their name during the market sell-off?

Some strategic bond funds stumbled in the recent market sell-off. Cherry Reynard surveys the aftermath.

26th May 2020 09:59

by Cherry Reynard from interactive investor

Some strategic bond funds stumbled in the recent market sell-off. Cherry Reynard surveys the aftermath.

The clinching argument for having strategic bond funds in a portfolio is that skilled active managers should be able to steer their portfolios to the right bond exposures at the right time. However, the latest market rout saw government bonds do well and anything with a whiff of risk – notably high-yield and emerging market bonds – collapse.

- Fund and investment trust tips for the post-pandemic ‘new normal‘

This isn’t necessarily the best environment for strategic bond managers. At the start of the year, government bonds looked very expensive and strategic bond managers who wanted to generate income had little option but to scout around among higher-risk markets. Gavin Haynes, an investment consultant at Fairview Investing, says most strategic bond funds had a high correlation to investment-grade and high-yield bonds.

This was in spite of some unappealing valuations. Kelly Prior, a fund manager in the multi-manager team at BMO Global Asset Management, says: “If you wanted to lend to companies, you were paid very little for the privilege – 2.7% for European high yield or 2.1% for UK investment grade is hardly the stuff of riches, particularly given the low economic growth environment that such companies were operating in and their ever-more stretched balance sheets.”

Managers’ bias to higher-risk bonds left many exposed when the rout happened. Eduardo Sanchez, a senior investment research analyst at Square Mile, says high-yield assets have suffered the largest losses, followed by emerging market debt. He adds: “Exposure to interest rates in high-quality developed government bonds has provided protection, as these assets acted as a safe haven during the market sell-off. The top-performing strategic bond funds in 2020 to the beginning of May were those that had higher exposure to developed government bonds, more sensitivity to interest rates and lower allocations to high-yield and emerging market debt.”

The hardest-hit funds were in many cases those with a ‘high income’ mandate where managers had been forced into higher-risk areas to deliver a yield. The weakest performers tended to be those funds that also included a smattering of stock market exposure alongside higher-yielding bonds, such as Artemis High Income and Axa Framlington Managed Income.

However, some funds fared notably differently. Investors holding the Allianz Strategic Bondfund, for example, will have been happy with their choice: it was up 18.7% over the three months to 6 May, according to Trustnet. Manager Mike Riddell’s cautious approach – more than half of his fund is in AAA-rated bonds and he takes a bearish view on corporate bonds – provided solid insulation against market disruption.

But the fund is an outlier and remains 14% ahead of any other fund in its sector. Only 12 funds have delivered a positive performance over the past three months, with the average fund down 4.1%.

Prior points to the Invesco Tactical Bond, Jupiter Strategic Bond and Janus Henderson Strategic Bond funds as other strong performers during this period. She says: “None of them predicted the impact of Covid-19, but – just by looking at the market and assessing the value on offer – they were positioned more defensively.”

Key question

The question now is whether those funds that have protected investments on the way down will be the right place to be on the way up. Certainly, those that have protected capital by staying in government bonds and remain invested there may not be the right option for investors. Government bond yields are now so low that it is difficult to see how they could go much lower. Moreover, in the longer term, inflation may be a consideration for strategic bond managers as the pandemic passes and vast stimulus measures come home to roost for the global economy.

Sanchez says: “With government bonds trading close to zero (or below in some cases) in developed countries, it is difficult to see the attraction of this asset class when you are expected to get close to nothing or even to pay to lend your money. But this is the situation that arises when economic growth is shrinking and governments need to take action to keep economies moving.

“Corporate bonds, meanwhile, offer more attractive valuations. Even after some normalisation in April, corporate spreads are trading at wider levels than for 80-90% of their history for both high-yield and investment-grade companies. But, of course, these higher yields on offer have to be tempered by the uncertain, but clearly higher, default rates expected.”

As a result, while it is tempting to pick managers that have performed well in the recent rout, investors need to be certain that these managers didn’t do well simply because they were ‘hiding’ in government bonds. Riddell, for example, performed strongly in the buoyant markets of 2019 and also the troubled markets of 2020. Sound top-down, macroeconomic analysis led him to his defensive positioning. What’s more, historically, he has opted for what would turn out to be higher-growth markets.

Prior points out that many managers have taken on additional risk as market prices have fallen. She says: “Since the dip in markets in March, we have seen active managers in this space take advantage of the opportunities that presented themselves. What is crucial to point out is that these managers are not taking a view on how the coronavirus will evolve or claiming to have epidemiological knowledge. They have looked at the quality of the companies they lend to, assessed the solvency of these businesses and made a mathematically based decision on risk and return.

“There are differences of opinion on whether financials are viable, and the desire to stretch down to the grubby, lower-rated bonds (below BB) is mixed, but that is what makes a market. We know defaults will pick up, but now investors are getting paid to take this risk.”

Sound choices

Haynes believes the Allianz Strategic Bond fund remains a sound choice. He says: “Mike Riddell has moved away from a very defensive portfolio in the first quarter of the year to increasing corporate bond exposure and has performed well in the recent rally. This is a good choice for a high-conviction, ‘go anywhere’ approach to bond markets.

“Other funds that have proved resilient, remain solid choices and take a flexible approach to bond markets include Jupiter Strategic Bond and Henderson Strategic Bond.”

The Covid-19 crisis has wrong-footed a number of managers in the strategic bond sector, particularly those who had targeted higher-income assets. However, a handful of strong managers have protect capital in the sell-off and profited in the subsequent rally. This is the real skill of a strategic bond manager.

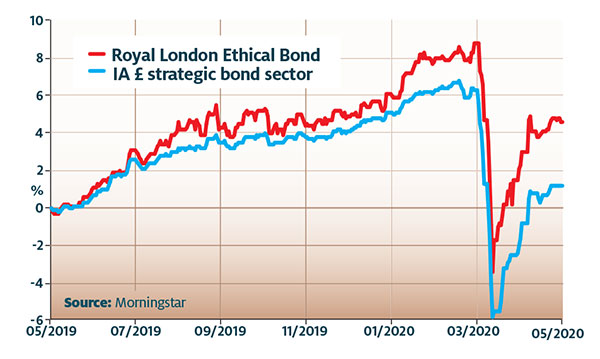

Spotlight on the Royal London Ethical Bond fund

Sustainable investing has come slowly to the bond market, and there remain few options for an investor who prefers a greener approach. However, sustainability is arguably highly important for bond investors, as good governance and the long-term sustainability of companies are key to the repayment of debt.

The Royal London Ethical Bond fund has been a decent performer through the recent crisis and over the longer term. The fund is down 3.1% over the past three months but up 4.6% over one year (Trustnet, to 7 May). It is first quartile over one, three and five years and has been one of the most consistent funds in the sector.

It is managed by Eric Holt, who also manages RLAM’s credit research process as well as the group’s Sterling Extra Yield Bond fund. He takes a stockpicking approach and much of the fund’s added value comes from stock selection. However, asset allocation, duration and yield curve management also play a role. The fund is predominantly invested inUK corporate bonds but also a selection of international corporate bonds.

The fund’s ethical policy means it does not invest in companies that derive more than 10% of their revenue from a variety of ‘unethical’ sectors, including alcohol, armaments, gambling, tobacco and pornography. It also avoids firms that have a high environmental impact and show no evidence of applying appropriate environmental management systems. Human rights abuses and animal testing are also included in the group’s screening process.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.