Spring Statement 2026: IHT and CGT receipts to soar by 2031

The government’s raid on capital taxes is laid bare in the OBR’s fresh fiscal and economic forecast.

3rd March 2026 15:50

by Craig Rickman from interactive investor

Chancellor Rachel Reeves leaves No 11 Downing Street to deliver her Spring Statement. Photo: Rasid Necati Aslim/Anadolu via Getty Images.

The Spring Statement was a damp squib in terms of fresh policies, as expected and welcomed, but a sift through the Office for Budget Responsibility’s (OBR) Economic and Fiscal Forecast unearthed a rather worrying trend for investors.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

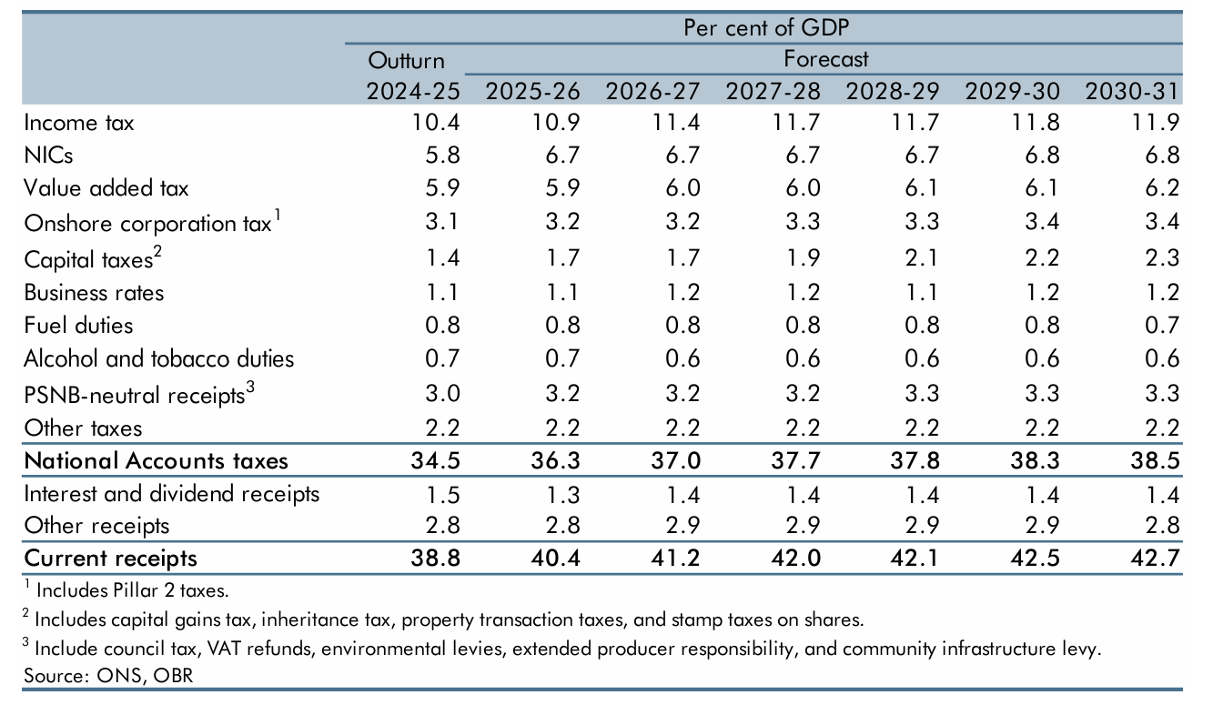

The document, which was published after the event as planned unlike the calamity we saw in the autumn, predicts that capital taxes as a share of gross domestic product (GDP) will rise from 1.4% in 2024-25 to 2.3% in 2030-31.

That’s an upwards revision from November and a leap over the six-year period of 64%, far bigger than the expected increases to any other tax or tax group. It means we’ll be paying much more in capital taxes – which include property transactions taxes, capital gains tax (CGT), inheritance tax (IHT), and stamp duty on shares - relative to the size of the UK economy.

By comparison, the next biggest expected climber, national insurance contributions (NICs), which saw unwanted reforms for employers at the Autumn Budget 2024, as a percentage of GDP are predicted to rise from 5.8% to 6.8% - a 17% uptick.

Source: Office for Budget Responsibility

What’s more, the effect of the policy measures since the Autumn Budget 2025 are expected to raise an extra £6 billion a year in capital taxes by 2030-31.

Why is this happening?

Capital taxes form a key obstacle when growing and preserving your wealth, and there are essentially three reasons to explain this unwelcome trajectory: policy reforms, frozen thresholds and rising asset prices.

- Policy reforms

The Autumn Budget 2024, the current government’s first fiscal event after winning power, saw sweeping proposed changes to the IHT system as well as increases to CGT.

- Inheritance tax

From April 2026, eligible shares owned for two years in the Alternative Investment Market (AIM) will only attract 50% relief instead of 100%, while 100% relief on farms and businesses will only apply to the first £2.5 million with 50% available on anything above. Regarding the latter, the government initially proposed to lower the tax-free threshold to £1 million but changed tack with just months to spare after a fierce backlash from farms and businesses.

And from April 2027, unspent pensions will be clawed into the IHT net, which is expected to affect almost 50,000 estates with pension assets every single year.

These changes won’t affect every family or business enterprise, but for those that are impacted the tax bills could be steep.

- Capital gains tax

At the same event, Chancellor Rachel Reeves announced increases to the headline rates of CGT with immediate effect. The previous rates, which were 10% at the basic rate and 18% at the higher rate, were jacked up to 18% and 24%, respectively. There were fears things could’ve been worse, with early pre-Budget rumours suggesting rates could be aligned with income tax.

The impact of these hikes is already being felt. In the first month of 2026 - January is always a big month for CGT as people pay self-assessment – receipts totalled close to £17 billion, up from around £10 billion in January 2025.

Between February 2025 and January 2026, the total CGT take was £20.6 billion, a 44% increase on the same period last year.

- Rising asset prices

Rising asset prices, such as property and equity markets, are a huge driver of capital tax receipts. House valuations have struggled in recent years and have fallen in some parts of the country, but the outlook appears brighter.

Savills, the property adviser, expects property prices to rise 22% over the next five years, with Knight Frank predicting similar increases, which could help to boost stamp duty receipts.

Higher property prices can also beef up CGT payments for owners of second homes who decide to sell up. While no CGT is payable on your main residence, it is applied to any other properties you own. We should also note that buying a second home comes with a stamp duty surcharge set at a hefty 5%.

And it’s not just rising house prices that can help raise capital taxes. For those with holdings outside tax wrappers such as pensions and individual savings accounts (ISA), rising stock markets can increase investment gains and in turn push up CGT receipts when investors decide to cash in any profits.

We should also note that investors pay stamp duty reserve tax when purchasing UK shares, even those held within an ISA. The rate is 0.5% on trades worth more than £1,000.

- Frozen thresholds

A dominant tax theme in recent years has been fiscal drag, the economic jargon to describe the covert impact of keeping tax thresholds on hold. Essentially, as our incomes and asset valuations naturally tick up over time, more either trips into the tax net or faces higher tax rates.

The most well-documented example is income tax and NIC thresholds, which have been maintained at the same level since 2021-22, and these freezes will continue until 2030-31.

But other tax thresholds have been frozen too, some for particularly lengthy periods. The IHT nil rate band, the value of assets you can own before IHT becomes payable at 40%, has stuck at £325,000 since 2009, with no plans for it to budge until 2031.

This is already causing IHT receipts to rise year on year while, according to the OBR, the Autumn Budget 2024 reforms are predicted to push the take to £14.5 billion in 2031, a whopping 67% leap.

Further to this, the residence nil rate band, which can boost the amount you can pass on tax free by £175,000 if you own a home and leave it to children has been frozen since 2020 and isn’t scheduled to increase, either.

In some instances, the assault on tax thresholds has been even more brutal, with limits slashed rather than merely frozen. Back in 2023, the first £12,300 of asset gains were shielded from CGT, but this handy allowance has since been hacked to £3,000, capturing more investor profits in the process.

What could affect these forecasts?

As the OBR’s report notes, capital taxes are typically paid by a narrower base of typically higher-income taxpayers, and receipts often sensitive to behavioural responses to policy changes.

They are also highly sensitive to growth in asset values, such as stock markets, that are “particularly volatile and hard to forecast”.

Capital taxes can be easier to swerve than others. CGT is only paid once you sell something and doesn’t apply on death. IHT, meanwhile, was described as a voluntary tax, and while the remark was tongue in cheek, there are steps you can take to potentially mitigate the tax, such as lifetime gifts. Admittedly, the options have tightened significantly since the Autumn Budget 2024.

The government clearly views IHT and CGT as key targets to boost its coffers. The decision to end the stamp duty holiday on home purchase and refusal to end stamp duty on UK shares underscores the importance these, too.

For investors, the threat of CGT and IHT will only grow over the coming years. On the plus side, with some prudent planning, and seeking expert advice where possible, you can reduce their impact enabling you and your loved ones to keep more of your wealth.

Important information: Please remember, investment values can go up or down and you could get back less than you invest. If you’re in any doubt about the suitability of a Stocks & Shares ISA, you should seek independent financial advice. The tax treatment of this product depends on your individual circumstances and may change in future. If you are uncertain about the tax treatment of the product you should contact HMRC or seek independent tax advice.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.