Stockwatch: can this AIM share continue to surprise on the upside?

With strong performance across its main income streams, analyst Edmond Jackson updates his view on this growth share against a backdrop of geopolitical turmoil and gold price volatility.

8th May 2026 11:43

by Edmond Jackson from interactive investor

It is rare nowadays for a company to be in the habit of upgrades each time it updates.

For AIM-listed Ramsdens Holdings (LSE:RFX), care is needed because gold prices fluctuating 40% to 50% higher than last year have boosted its precious metals buying side, and foreign currency sales could be affected by constrained jet travel this summer.

Yet after last Wednesday’s trading update in respect of its 30 September financial year, Ramsdens shares have risen 13% to 435p after profit expectations were yet again raised driven by strong performance across its main income streams.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Open a Trading Account

Yes, the precious metals purchase division (27% of interim gross profit) has benefited from strong gold, hence its revenue is 40% higher and the weight of gold traded is up 50%. But jewellery retail (29% of profit) revenue is also up, by 25%, and the pawnbroking loan book (23% of profit) is 24% higher.

Quite often with this type of operation balancing such activities, you might see, for example, pawnbroking trade inversely to jewellery retail, because in hard times, people pawn items and cut discretionary spending. That enables an operator such as Ramsdens to smooth earnings volatility although it makes strategic sense anyway to dovetail such activities.

High-margin foreign currency sales (19% of profit) slipped slightly but commission fell 9% due to a shift towards lower-margin online and currency card sales. Summer currency volumes are in line with last year, however management cautions that “recent reports around fuel shortages impacting flights over the summer, may also impact international travel and consequently our foreign currency sales”.

Yet the trajectory looks plenty good unless gold plummets - something I find hard to envisage given the high level of macro uncertainty persisting, even if a US/Iran compromise is hammered out. Management says that it is on track to open 10 to 12 new stores in the current financial year, in the context of 175 recently across the UK.

Fathoming the forward price/earnings (PE) is a bit nebulous and needs care given consensus expects that the September 2026 year will prove exceptional , while 2027 will see a 10% decline in revenue, and an even greater 38% decline in earnings per share (EPS). But the 12-months’ forward multiple could anyway be a tad less than 10x and the yield over 5%, hence the rating is still cautious anyway.

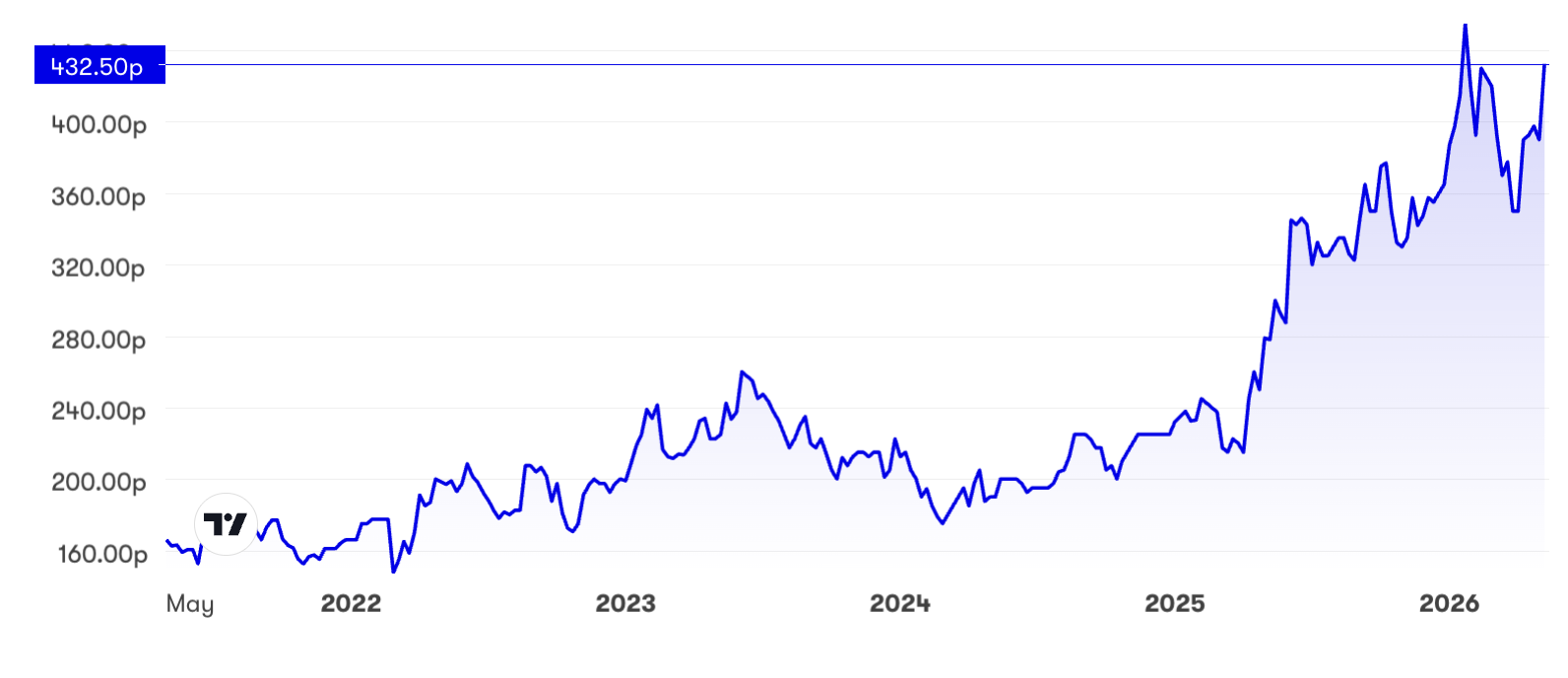

The five-year chart remains strong and a February-March drop has been quickly recouped:

Source: interactive investor. Past performance is not a guide to future performance.

That the shares have risen despite wider market volatility in response to on/off hopes for a US/Iran settlement that re-opens the Strait of Hormuz, suggests investors are attuned to scope for Ramsdens to continue to appreciate despite the currency sales’ risk.

Obviously, there is the contrarian question as to how long high gold prices will keep flushing out sales, from which Ramsdens can benefit, but pawnbroking ought to be supported by the higher cost of living.

Delivering quite as H&T Group did before takeover

Last May, I drew attention to Ramsdens as a “buy” at 300p after peer company H&T Group – a long-time favourite – was taken over at a 90% premium to its January 2025 market price.

While its US acquirer, FirstCash Holdings Inc (NASDAQ:FCFS), identified strategic benefits for UK/European expansion – potential synergies to justify paying significantly over the market price – my recollection of H&T was its shares similarly averaging a 10x PE and 5% yield. Not to argue explicitly for Ramsdens’ takeover potential but [consider] a private buyer identifying value greater than the market, which would fret periodically if one or two divisions lagged others.

Ramsdens is not the UK leader like H&T but it has a similar strategy of dovetailing pawnbroking with gold trading, plus jewellery/watches and foreign currency. I took comfort from how both companies shared the exact same 13% operating margins over the last three financial years, plus good dividend growth with over twice earnings cover. Ramsdens’ prospective yield was around 4.5% as dividend payout expectations rose over 13p per share.

- Share Sleuth: how I decided which firm to trim to raise cash

- Tony Blair Institute’s radical proposal to overhaul state pension

While H&T was valued by the market at around £190 million then bought for near £300 million, Ramsdens was valued at £97 million a year ago, which has since grown to £140 million. This still trails consensus for £144 million sales as consensus for its year to 30 September 2026, although as yet the expectation is for a 10% decline to £129 million in 2027, with a greater 38% fall in EPS to about 38p based on £12.4 million net profit.

Figuring a 12-month prospective EPS around 45p on such a basis, the PE is a modest 9.6x – and similarly for dividend per share (DPS), a payout of 23p implies a 5.3% yield. Mind you, (for what consensus is worth) the expectation is for a 70% rise in DPS to 23p in respect of the September 2026 year followed by a decline to 16p in September 2027.

Notwithstanding scope for earnings volatility, Ramsdens’ quality of business is such that it enjoys mid-teen operating margins and had delivered return on capital over 20% in the last two financial years. It employs negligible net debt. The pawnbroking operation makes it an obvious share to own, should a recession ensure.

Ramsdens Holdings - financial summary

Year end 30 Sep

| 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 46.8 | 76.9 | 40.7 | 66.1 | 83.8 | 95.6 | 117 |

| Operating profit (£m) | 6.6 | 10.0 | 1.0 | 8.8 | 10.9 | 12.5 | 17.1 |

| Net profit (£m) | 5.2 | 7.1 | 0.4 | 6.6 | 7.8 | 8.3 | 11.9 |

| Operating margin (%) | 14.1 | 13.0 | 2.6 | 13.4 | 13.0 | 13.0 | 14.6 |

| Reported earnings/share (p) | 16.7 | 23.1 | 1.2 | 20.9 | 24.0 | 25.7 | 36.0 |

| Normalised earnings/share (p) | 16.9 | 15.7 | -1.8 | 20.9 | 24.0 | 25.7 | 36.1 |

| Operational cashflow/share (p) | 5.0 | 51.1 | 3.5 | 9.3 | 10.2 | 36.8 | 18.5 |

| Capital expenditure/share (p) | 12.7 | 6.6 | 5.3 | 9.0 | 8.4 | 8.0 | 2.8 |

| Free cashflow/share (p) | -7.7 | 44.5 | -1.8 | 0.3 | 1.8 | 28.8 | 15.7 |

| Dividend per share (p) | 7.2 | 2.7 | 1.2 | 9.0 | 10.4 | 11.2 | 13.5 |

| Covered by earnings (x) | 2.3 | 8.6 | 1.0 | 2.3 | 2.3 | 2.3 | 2.7 |

| Return on total capital (%) | 20.9 | 23.4 | 2.4 | 17.7 | 19.4 | 20.1 | 24.3 |

| Cash (£m) | 13.4 | 15.9 | 13.0 | 15.3 | 13.0 | 15.8 | 15.4 |

| Net debt (£m) | -8.2 | -6.8 | -4.4 | 1.1 | 5.1 | 2.3 | 1.7 |

| Net assets (£m) | 30.9 | 35.6 | 36.1 | 41.8 | 48.2 | 53.6 | 62.9 |

| Net assets per share (p) | 100 | 115 | 115 | 132 | 152 | 168 | 194 |

Source: company accounts.

Possibly gold prices are in a consolidation phase

While gold is liable to remain volatile like it always has, such is the extent of macro uncertainty nowadays that it may support volatility at relatively high prices.

After price spikes of over $5,000/ounce in late January and early March, gold dropped to a support level of around $4,400, trading in a range up to $4,800. At around $4,700 currently, the price is 47% higher than $3,200 a year ago with the chief rally happening from last August to $4,300 by year-end. The late-January spike ahead of the US/Israel attacks on Iran in late February, has fully reversed, as if a major de-rate is unlikely should some kind of “peace” settlement get hammered out.

While I don’t suggest Ramsdens’ earnings scenario can buck consensus for a 29% decline in 2027, if gold remains broadly supported, then the company may continue to “surprise on the upside” in the sense of a less serious EPS drop.

Admittedly, this disqualifies the shares from the PEG ratio (PE divided by the expected earnings growth rate), which requires consistent growth, and earnings volatility argues for a PE lower than the growth rate. But perhaps investors are seeing through this to recognise a good-quality business.

- My 10-point checklist for picking smaller company shares

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Ramsdens listed in early 2017 and its only chief downturn was a halving from around 245p in February 2020 when Covid struck. Otherwise the long-term trend has been steadily up, with acceleration from March 2025. Besides passing a momentum share screen, the shares also qualify for several classic growth filters, such as James O’Shaughnessy and T. Rowe Price, hence a nice balance of “growth and momentum”.

Interim results are due on Thursday 4 June when the CEO and CFO will give a live presentation and Q&A session from 5pm for existing and potential shareholders via the Investor Meet Company platform. Effective communication such as this could help sustain awareness of the story than more typical profit-taking when a share has risen ahead of results.

Broadly, I therefore maintain a long-term “buy” stance chiefly because I believe gold will be sustained high enough to keep good numbers flowing from Ramsdens’ trading side even if 2026 proves exceptional.

Pawnbroking should benefit from the cost-of-living crisis and mitigate near-term downside risk in currency, and also perhaps jewellery sales, in due course.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.