Stockwatch: a FTSE 100 stock to play end of Iran war

Despite exchanging more missiles, hopes of a de-escalation of the Middle East conflict have improved. Analyst Edmond Jackson names a stock he likes right now.

24th March 2026 13:24

by Edmond Jackson from interactive investor

US President Donald Trump beside Air Force One this week. Photo: Roberto Schmidt/Getty Images.

Perhaps it shows how ingrained a “buy the drop” approach has become since 2008, if not 1987, that risk assets roared back after US President Donald Trump’s latest shouty upper-case post about how Iran and the US are productively discussing “TOTAL RESOLUTION OF OUR HOSTILITIES”.

It looks very much as if Trump has blinked first amid the economic cataclysm unfolding and awareness of how his threat last Saturday – to obliterate Iranian energy facilities – would mean escalated retaliations. Oil prices took off, which would destroy Republicans at mid-term elections.

- Invest with ii: Open a Stocks & Shares ISA | Top ISA Funds | ISA Offers & Cashback

Iran remains in a strong position. It retains control of the Strait of Hormuz as leverage over the US and its allies, forcing the US to recalibrate. Clearly, Trump’s prime objective is no longer regime change but to reopen the Strait. Did any of his advisers recall how the Suez Canal was shut for eight years following the 1967 Six-Day War?

Urgency was underlined just before this surprise turn of events by a chief of the International Energy Agency (IEA) declaring this crisis as “equivalent to the combined force of the twin oil shocks of the 1970s plus the fallout of Russia’s invasion of Ukraine on the gas market”. It would compromise “vital arteries of the global economy”, including petrochemicals, fertilisers and helium – an essential aspect for microchips and artificial intelligence (AI) besides hospitals.

While Iran’s foreign ministry and state media denied any talks, this probably was a show of strength to Iranians. I speculate that intermediaries had dialogue somewhere along the line.

Still, we should have learned how Trump’s posts have attracted allegations of insider trading and market manipulation. Some $580 million (£433 million) oil futures contracts were placed 15 minutes before yesterday’s post.

Maybe Trump is also buying time for US Marines to arrive from Singapore, hence his post cannily expanded US options besides discombobulating Iran as opponent. To his credit, it immediately reversed a financial horror show. Method exists within apparent madness.

- Shares for the future: upgrade makes this a top five stock

- AIM market winners and losers since Iran war broke out

The fact remains that at least 40 energy assets in the Gulf region have been badly damaged, so even a cessation of conflict will not promptly restore supply. Remembering “Red” Adair extinguishing Kuwaiti oil wells set alight by retreating Iraqi forces in 1991, it is going to take years to rebuild plants.

Investors would be wise to appreciate the situation remains fluid despite yesterday’s rebound. Versus the essential need to restore the free flow of shipping, tough concessions will be needed both from Iran and the US for any reliable “deal”. That there is no resolution to the war in Ukraine after four years demonstrates the dilemma.

A hint towards energy demand destruction

Note how early yesterday morning, oil & gas shares were mixed, no longer trading inversely to the market in response to an oil price spike.

It showed how traders are wise to the risk of how energy demand starts to get compromised beyond a certain price. This is relevant to judging to what extent oil & gas shares can serve as a portfolio hedge, although notably also renewables were affected in the early markdown.

Driving back through a town centre around noon last Sunday, after jogging in a park, I was taken aback at far less traffic than at the same time a week ago, despite it being a sunny day. Fuel pump prices had just risen around 7p a litre.

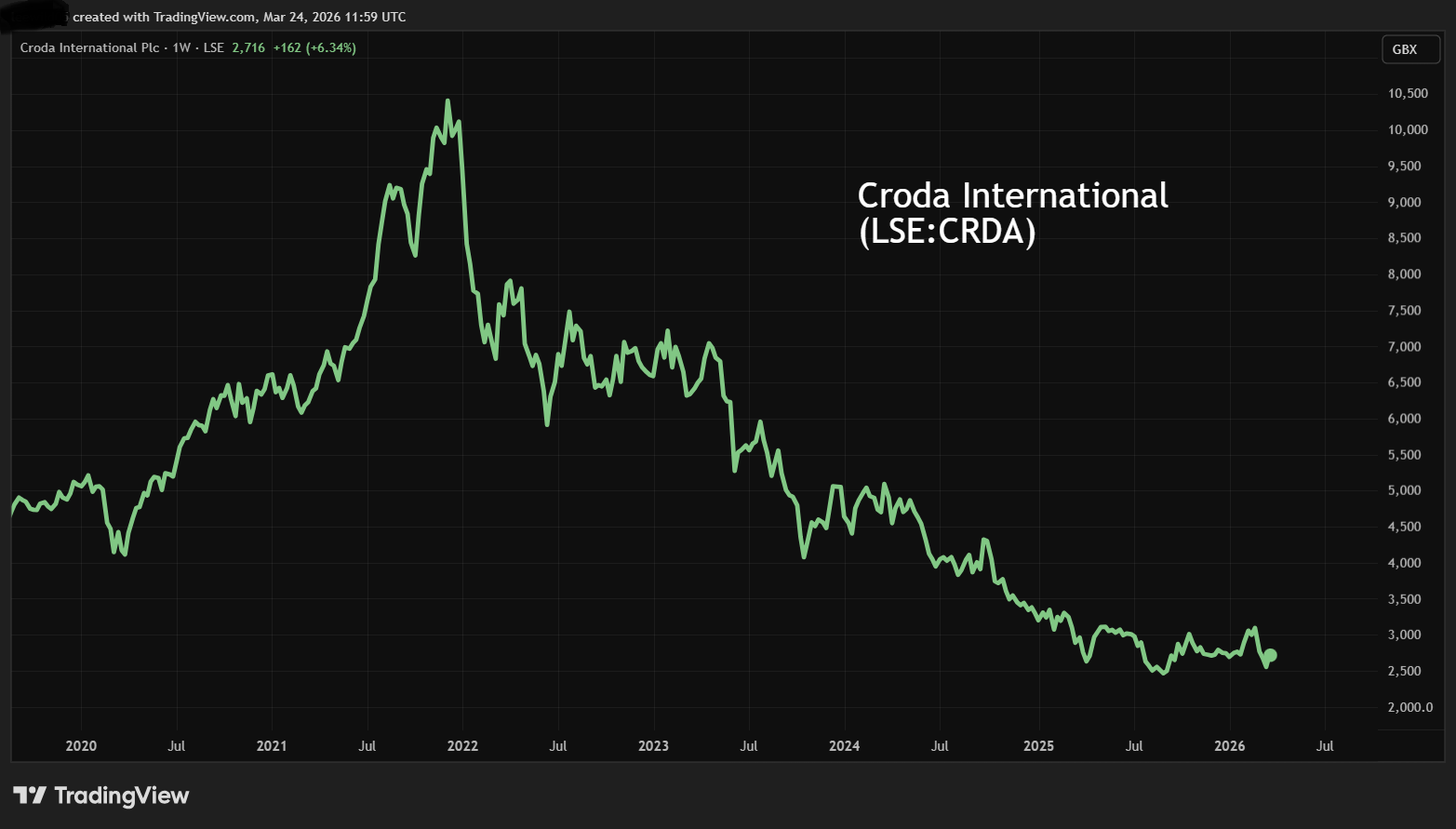

Has Croda International finally hit an inflection point?

Croda International (LSE:CRDA), a FTSE 100 specialty chemicals company, was one of the strongest rebounders from about 11.15am yesterday – up around 8% before closing up 5.6% near 2,700p. While petrochemical prices and availability are an obvious factor, there was a boost from Goldman Sachs that coincided with the oil price turnaround, upgrading from “sell” to “buy” and raising its 12-month target from 2,800p to 3,200p.

I have occasionally wondered whether to engage Croda given that it has some strong market positions, although the premium goods involved could be compromised by economic slowdown. This 101-year-old firm makes a wide range of products such as surfactants for cosmetic lotions, dietary supplements such as omega-3 oils and fatty acid amides used so plastic bags can be peeled apart.

It enjoys significant patents and high barriers to entry, yet its medium-term revenue growth trend has been volatile, and the reported operating margin declined from 23% to 6.5%. Premium products can be economically sensitive.

- ii view: Croda issues sales beat and new growth targets

- Insider: directors buy two stocks at ‘attractive entry point’

Croda is therefore of seemingly mixed appeal but, if a four-year bear market has flushed out most sellers, then, technically, a reversal could “climb a wall of worry”. Might Goldman’s volte-face mark an inflection point?

This analyst team’s original “sell” was April 2025 at 2,632p, late in Croda’s bear market and since which the shares have only traded volatile-sideways. Goldman says that it did not expect the product breadth and magnitude within a 7% 2025 group revenue rise. An operating margin of over 20% by 2028 is now seen as “increasingly achievable”.

Croda shares have, however, not been a long-term sideways-volatile trend. They delivered a bull run from 500p in 2006 to a 10,180p high in late 2021 before falling. Does this raise the odds of a buy-and-hold mean-reversion rather than temporary recovery?

Source: TradingView. Past performance is not a guide to future performance.

The current price level does essentially regain the range from last November to February, before a blip to 3,200p as war broke out. Achieving Goldman’s margin improvement depends on reopening the Strait of Hormuz.

While the revenue profile hardly depicts a growth company, dividend growth has been more consistent and a 4.4% prospective yield is expected to have around 1.5x earnings cover, potentially more so by cash flow where the record is strong:

Croda International - financial summary

Year-end 31 Dec

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£m) | 1,390 | 1,890 | 2,089 | 1,695 | 1,628 | 1,699 |

| Operating margin (%) | 20.8 | 23.0 | 38.2 | 14.6 | 14.0 | 6.5 |

| Operating profit (£m) | 289 | 435 | 799 | 247 | 227 | 110 |

| Net profit (£m) | 202 | 321 | 649 | 171 | 159 | 62.0 |

| Reported earnings/share (p) | 155 | 229 | 465 | 122 | 113 | 44.4 |

| Normalised earnings/share (p) | 172 | 233 | 227 | 155 | 132 | 182 |

| Operating cashflow/share (p) | 220 | 249 | 221 | 241 | 229 | 205 |

| Capital expenditure/share (p) | 93.1 | 114 | 109 | 135 | 130 | 85.9 |

| Free cashflow/share (p) | 127 | 135 | 112 | 106 | 98.5 | 119 |

| Dividend/share (p) | 91.0 | 100 | 108 | 109 | 110 | 111 |

| Covered by earnings (x) | 1.7 | 2.3 | 4.3 | 1.1 | 1.0 | 0.4 |

| Return on capital (%) | 10.8 | 15.3 | 25.6 | 7.6 | 7.2 | 3.7 |

| Cash (£m) | 107 | 113 | 321 | 173.0 | 167.0 | 173 |

| Net debt (£m) | 801 | 823 | 295 | 538 | 532 | 524 |

| Net assets/share (p) | 1,136 | 1,256 | 1,730 | 1,685 | 1,635 | 1,566 |

Source: company accounts.

According to consensus, the 2026 price/earnings (PE) ratio is around 17x, which looks pricey in the near term, given a likely 14% decline in earnings per share (EPS) but reflects confidence for a 13% recovery in 2027. Such a scenario, however, would be disrupted by substantially higher oil prices.

On 6 March, the non-executive chair of two years bought £20,900 worth of shares at 2,788p. Otherwise – if this roughly marks a low – director dealings have involved options-exercising, then selling shares to meet tax liabilities. That is a less strong indication of attractive risk/reward albeit reflecting the compensation culture nowadays.

Two hedge funds have disclosed short positions: Walleye Capital at the 0.5% disclosure threshold as of 9 March and AQR Capital Management raising its short 0.08% to 0.9% of this £3.6 billion company as of 16 March.

- Funds that provide shelter in a stock market storm

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Croda’s guidance for 2026 – before war broke out on 24 February – was for organic sales growth of 3-6%, with an improvement in operating margin driven by higher profitability in consumer care and life sciences, and also a transformation programme.

So, the rationale here is somewhat mixed, which is hardly a “conviction buy”, albeit with contrarian appeal and a sense of a classic “value” share that’s out of favour but has leading products enjoying strong market positions. Holders of Diageo (LSE:DGE) can, of course, retort that is a load of – well, fine words.

I am still going to broadly go with a “buy” stance on Croda, but it does require soaring oil prices and recession to be averted.

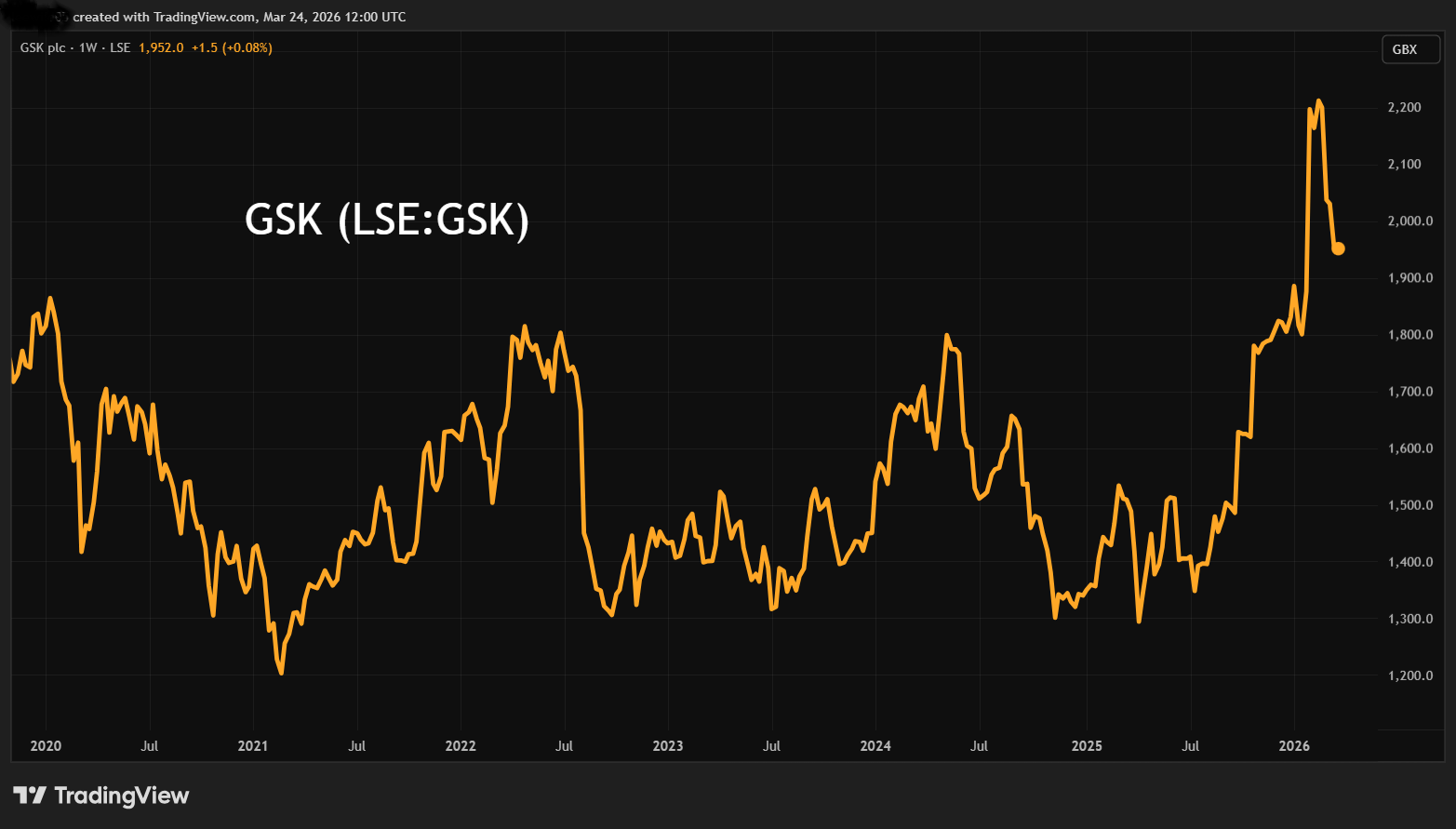

GSK is not quite as defensive as expected

Another upshot from recent volatility is this prime healthcare group not proving as defensive as one might expect – at least in share price terms.

Since 18 February, GSK has fallen over 14% from 2,268p to 1,943 and was up just 0.3% yesterday when risk assets such as banks, airlines and housebuilders benefited. The share is not altogether functioning as a hedge against “risk-off” nor performing when risk appetite recovers – although it has been better to hold than the likes of Barclays (LSE:BARC), which is down 22% over same period.

Source: TradingView. Past performance is not a guide to future performance.

Admittedly, it is a very short-term view, but a “defensive” share must prove so otherwise the concept is redundant in a major market decline. This is despite GSK having delivered much better product development news flow than in previous years.

In January 2025 at 1,360p, I retained a “buy” stance, and the shares rallied 67% to February’s high before dividends and are still up 43%. At around 1,950p, consensus forecasts imply a 12-month forward PE is 10.6x and a prospective yield of 3.7%.

In due respect of GSK’s corporate development, I consider “hold” is appropriate.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.