Lands of opportunity: trusts looking beyond America

A Kepler analyst explores investment opportunities in major equity regions outside the US.

20th March 2026 13:46

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

The term “Bakumatsu” refers to the final years of the Edo period in Japanese history, during which the Shogunate — the hereditary military government — came to an end. For nearly 700 years, the military ruler, known as the Shogun, held actual political power in Japan, while the emperor was largely a symbolic head of state.

However, a combination of geopolitical and societal changes gradually undermined the Shogunate’s authority. These pressures ultimately culminated in the Boshin War, a civil conflict that pitted the Shogunate, which sought to preserve the existing order, against the imperial court, which aimed to restore governing authority to the emperor. The defeat of the Shogunate in this conflict brought an end to a system that may once have seemed immutable.

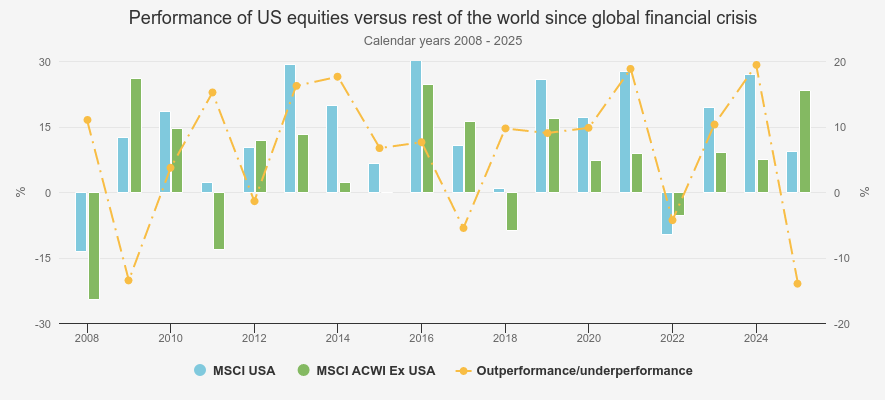

Arguably, the Shogunate’s seven-century-long rule over Japan may be reminiscent of the dominance of US equities over the rest of the world, particularly since the global financial crisis. Since 15 September 2008 — when Lehman Brothers filed for bankruptcy — the MSCI USA Index has returned 815.5%, more than three times the 260% return of the MSCI ACWI ex USA Index.

In addition, between 2008 and 2025, US equities outperformed the rest of the world in circa 72% of calendar years, as the chart below shows.

In our view, the reasons for this strong outperformance include the dominance of technology-related stocks — which are strongly represented in US equity indices — supportive monetary and fiscal policies, cheap energy from shale, and the strength of the US dollar.

CALENDAR-YEAR RETURNS

Source: Morningstar. Past performance is not a reliable indicator of future results.

However, we believe there are signs that US hegemony in global equity markets may be coming to an end. Investors have shown greater interest in equity markets outside the US since last year, driven by concerns over the health of the US economy, the erratic behaviour of the Trump administration, and more attractive valuations in other regions.

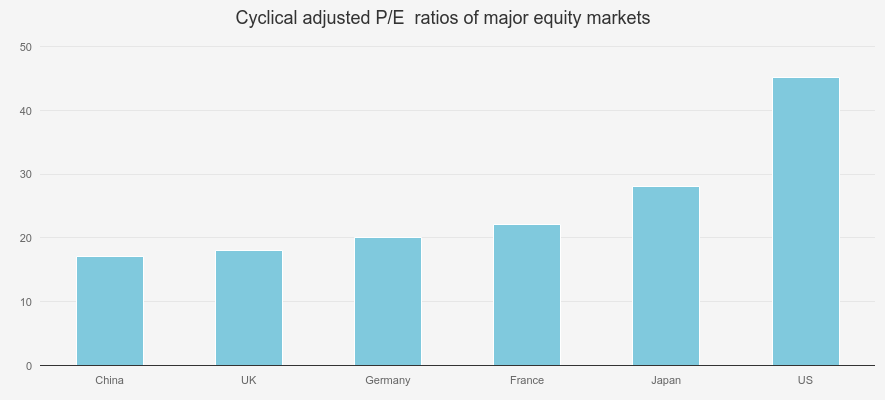

As the chart below shows, US equities stand out as particularly expensive compared to other major equity markets when measured by the cyclically adjusted price-to-earnings (P/E) ratio. As a result, investors may opt to rotate out of US equities on valuation grounds.

CYCLICAL ADJUSTED P/E RATIO

Source: Ruffer, GFD CAPE data, adjusted for subsequent daily price changes data to January 2026.

Meanwhile, AI spending has become an important contributor to the US economy, with hyperscalers such as Microsoft Corp (NASDAQ:MSFT), Amazon.com Inc (NASDAQ:AMZN), and Oracle Corp (NYSE:ORCL) having collectively invested several hundred billion US dollars in AI infrastructure.

In fact, AI-related capital expenditures accounted for 1.1% of US GDP growth in H1 2025. As such, a slowdown in AI spending could materially impact US economic growth and have ripple effects, notably on the job market, with fewer hires in IT services, hardware manufacturing, and construction roles, among others. This would also likely weigh on consumer sentiment, which is already low relative to historical standards. It is also worth noting that, while these investments could eventually boost profits, they may also reduce companies’ free cash flow (FCF) generation. In the short term, slower FCF growth could trigger negative market reactions, and the consequences could be more severe if these capex investments fail to meet long-term expectations. Finally, the US dollar is facing structural challenges, including de-dollarisation trends, while a high public deficit could erode confidence in the currency.

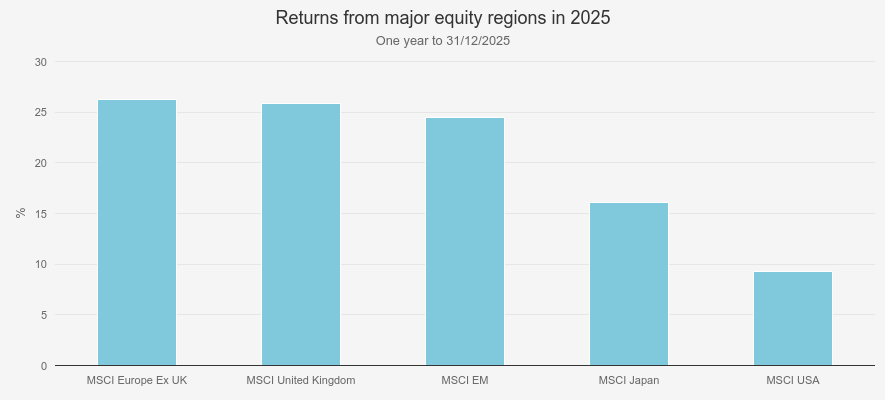

As a result, we believe investors should consider adding some geographical diversification in their portfolio, as US equities may be experiencing their own “Bakumatsu” period. In fact, US equities significantly underperformed the rest of the world in 2025 (in GBP terms) and are also lagging year-to-date (as of 10 March 2026). In this article, we explore investment opportunities in major equity regions outside of the US.

Europe

Investors have been allocating more capital to European equities since the beginning of the year. We believe this may reflect a shift in sentiment towards the region following its strong performance in 2025. In fact, Europe ex-UK was the best-performing major equity region last year (in GBP terms), as the chart below shows.

Moreover, while European equities are now expensive relative to historical levels, they are still trading at a discount to their US counterparts. This may be prompting investors wary of lofty valuations to favour Europe over the US on a relative basis. There have also been improvements in the macroeconomic outlook for the eurozone, such as falling inflation and interest rates lower than those in the US and UK, which may have caught investors’ attention.

Finally, we believe there are some clear investment themes that could sustain market returns in the region, notably Germany’s stimulus package, which particularly targets infrastructure and defence.

RETURNS IN 2025

Source: Morningstar. Past performance is not a reliable indicator of future results.

In our view, Germany’s €500 billion stimulus package represents a paradigm shift and may have the potential to be a game changer for Europe. Historically, Germany — Europe’s largest economy — prioritised balanced budgets and low public debt. In fact, the country has had a ‘debt brake’ enshrined in its constitution since 2009, which limits the federal government’s ability to borrow, although it was loosened in March 2025.

However, this approach has resulted in underinvestment, leading to crumbling infrastructure and a decline in industrial competitiveness. The stimulus package seeks to address these issues, which we believe could prove supportive for industrials and infrastructure-related companies.

The package also focusses on defence, a matter that has become crucial for Europe since the outbreak of the war in Ukraine in 2022, and has been compounded by questions around American commitments to European defence. EU member states have been ramping up defence spending in recent years, which is estimated to have reached €381 million in 2025 — a c. 63% increase compared with 2020. As Germany aspires to build Europe’s largest army, we believe this theme may have further scope to run.

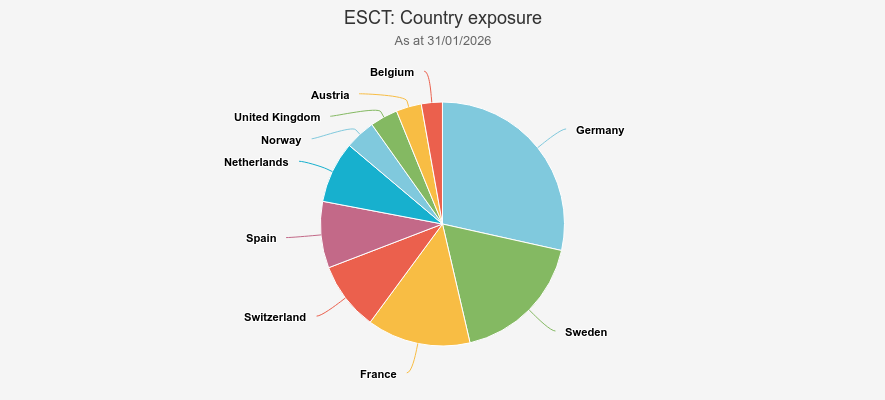

We think The European Smaller Companies Trust PLC (LSE:ESCT) could be well positioned to benefit from Germany’s stimulus package. German stocks account for approximately a quarter of the portfolio, as the pie chart below shows, with manager Ollie Beckett having identified opportunities linked to infrastructure and defence spending.

COUNTRY EXPOSURE

Source: Janus Henderson.

UK

UK equities delivered their best annual gains since 2009 last year. In spite of this, they remain out of favour with investors, with outflows from UK equity funds having continued in 2025. Moreover, while the FTSE 100 Index has rerated to its long-term valuation averages as a result, UK equities continue to trade at a discount to other developed markets, including the US, Europe, and Japan.

However, we believe the outlook for UK equities may be stronger than fund flows and valuations suggest. For instance, UK household balance sheets are in good shape, with low debt levels that could support a recovery in consumption. The balance sheets of UK corporates are also healthy, providing scope for credit expansion to fuel growth. In addition, the sectoral composition of the FTSE 100 Index, which is rich in energy-related businesses, could prove attractive going forward. Rising power demand from data centres could be a key driver, while higher geopolitical tensions may also be supportive, as countries seek to strengthen energy security. Finally, it is worth remembering that three-quarters of UK large-cap companies, as well as nearly half of mid-cap businesses, generate their revenues overseas, meaning they are not overly reliant on the domestic economy.

That said, we believe the best opportunities in the UK equity market are to be found in the small- and mid-cap (SMID) space. Unlike their large-cap peers, SMIDs are still trading at a discount to their historical averages, offering potential for rerating. In fact, the FTSE 250 ex Investment Trusts and the Deutsche Numis Smaller Companies ex Investment Trusts indices are both trading on a lower P/E ratio than the FTSE 100, which we view as an anomaly, since SMID indices typically command higher valuation multiples than their large-cap counterparts, reflecting their greater growth potential. Moreover, SMIDs are benefiting more from M&A activity, with both private equity firms and corporate buyers taking advantage of low valuations in this part of the UK equity market. In addition, interest rates in the UK have progressively fallen since 2024, reducing borrowing costs and making refinancing existing debt more affordable. Lower yields from risk-free assets may also increase the appeal of UK SMIDs.

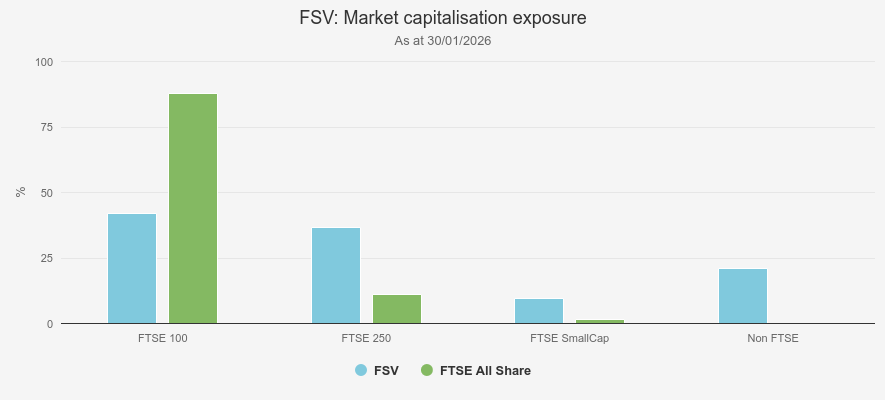

As a result, we believe that investment trusts taking an all-cap approach could prove attractive at this juncture, allowing investors to gain exposure to a potential rerating of UK SMIDs while maintaining allocation to the remaining opportunities within the large-cap space. We would particularly highlight Fidelity Special Values Ord (LSE:FSV), with managers Alex Wright and Jonathan Winton applying a contrarian approach, investing in overlooked and undervalued companies. Following the strong performance of the FTSE 100 Index in 2025, they have increased their bias towards SMIDs.

MARKET CAP EXPOSURE

Source: Fidelity International

Emerging markets

For the first time since 2020, emerging markets outperformed their developed market peers last year. We believe this outperformance could be sustained in the near term, as emerging markets may benefit from tailwinds such as lower US interest rates, a weaker US dollar, and attractive valuations relative to developed markets. In fact, as the table below shows, emerging market equities are currently trading on lower forward P/E ratios than their US and other developed market peers, while offering stronger earnings growth expectations over the next 12 and 24 months.

VALUATIONS & EARNINGS GROWTH EXPECTATIONS

| Index | MSCI EM | MSCI World ex USA | MSCI USA |

| P/E (forward to the end of 2027) (x) | 10.6 | 14.6 | 18.9 |

| P/E (forward to the end of 2028) (x) | 9.3 | 13.6 | 16.8 |

| Earnings growth (1-yr forward) (%) | 21.4 | 10.4 | 15 |

| Earnings growth (2-yrs forward) (%) | 28.1 | 7.5 | 11.4 |

Source: Bloomberg, as at 10/03/2026.

Over the long term, we believe emerging markets could benefit from powerful structural growth themes, including rising living standards, the reshaping of global supply chains, and rapid technology adoption, among others. On the technology front, it is worth highlighting that many companies in emerging markets, particularly those listed in Taiwan and South Korea, are deeply embedded in the AI supply chain, while China is viewed as the closest competitor to the United States in terms of AI developments. Interestingly, the team at Ruffer Investment Company (LSE:RICA) prefers to gain exposure to the AI theme through Chinese companies, which trade on lower valuations than their US peers. We published a new note on RICA last week.

Moreover, companies across emerging markets have made efforts in recent years to improve shareholder returns, notably through increased share buybacks and higher dividends. This includes South Korea, which launched its ‘value-up’ programme in 2024, emulating Japan’s corporate governance reforms. Meanwhile, many Chinese companies, including those traditionally focussed on capital appreciation such as Alibaba Group Holding Ltd ADR (NYSE:BABA), have distributed more of their FCF to shareholders via dividends and share repurchases (see our recent strategy article). These changes in attitude towards shareholders may enhance the appeal of emerging market equities and make them more accessible to dividend-seeking investors, allowing them to benefit from their growth potential without compromising income objectives.

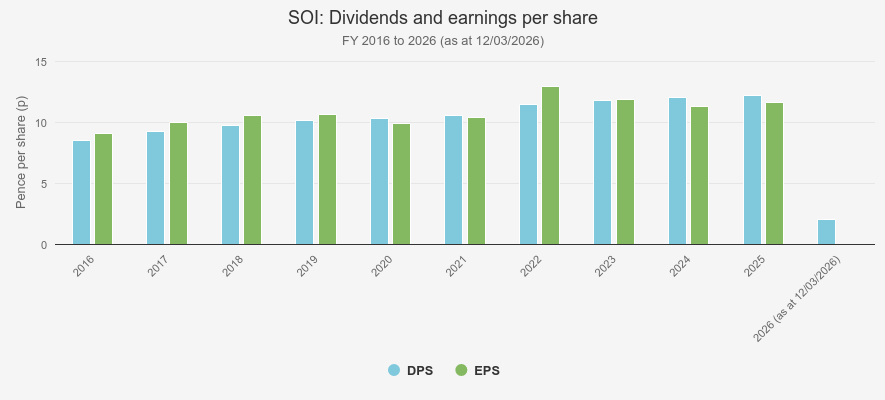

We view Schroder Oriental Income Ord (LSE:SOI) and JPMorgan Emerging Markets Div Inc (LSE:JEMI), both of which pay a ‘natural’ income, as attractive vehicles to capture the growth potential of emerging markets while benefiting from improvements in dividend culture across these regions. SOI boasts a 19-year track record of dividend increases and currently offers a historic yield of c. 3.2%. In contrast, JEMI offers a historic yield of c. 3.5% and currently trades at a slightly wider discount — c. 6.8% versus c. 4% for SOI — offering somewhat more rerating potential.

DPS & EPS

Source: Schroders.

Japan

Similar to other regions, Japanese equities outperformed their US peers last year. We believe ongoing corporate governance reforms will be a key driver for this outperformance to continue. While large-caps have largely rerated since 2023, as discussed in a previous article — with the TOPIX now commanding a higher multiple than most major developed markets outside the US — we think this theme may continue to unfold in the smaller end of the market-capitalisation spectrum. Many smaller Japanese firms are lagging in their plans to improve shareholder value and still hold substantial cash on their balance sheets. It is in this segment of the market that AVI Japan Opportunity Ord (LSE:AJOT) seeks opportunities. The team applies an activist, engagement-led approach, focussing on balance sheet inefficiencies and governance improvements to unlock shareholder value.

However, we think Japanese equities could also benefit from further tailwinds beyond corporate governance reforms. This includes the revamping of the NISA — Japan’s equivalent of the UK ISA — which, combined with the return of inflation, could incentivise retail investors to move out of cash and deploy capital into equities. In addition, Japan is one of the largest providers of foreign direct investment worldwide, meaning that some capital could potentially be repatriated and reallocated into domestic assets. This could result from improvements in the investment environment in Japan, for example. In addition, the landslide election victory of Sanae Takaichi in February 2026 should enable the Japanese prime minister to implement expansionary fiscal policies without facing parliamentary friction, which could provide an economic boost. However, such policies may push JGB yields higher, particularly given Japan’s already elevated debt-to-GDP ratio (above 200%).

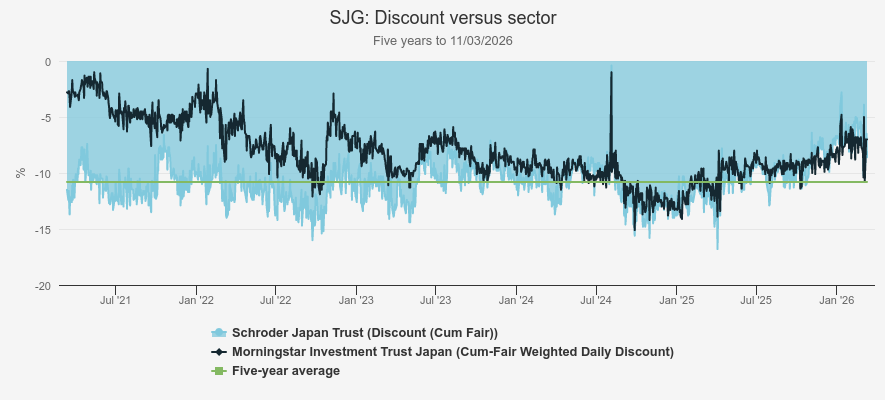

Given this backdrop, we believe Schroder Japan Trust Ord (LSE:SJG) could be attractive at this juncture. The portfolio is exposed to companies that may benefit from a steeper yield curve, such as insurers, as well as industrially linked businesses that could gain from government stimulus designed to spur the economy. In addition, SJG is overweight SMID companies, which are more exposed to the domestic economy and would be well positioned to benefit if expansionary fiscal policies result in stronger economic growth. The trust is also trading at a c. 9% discount, offering rerating potential. Interestingly, discounts remain wide in the AIC Japan sector compared with most other regional equity sectors. To us, this suggests a disconnect between investor sentiment and fundamentals, given the strong returns generated by Japanese equities and several sector constituents, including SJG, over the past five years.

DISCOUNT

Source: Morningstar.

Conclusion

The victory of the imperial forces over the Shogunate in the Boshin War led to the Meiji era, during which Japan embarked on a transformative period of reform and modernisation, adopting technologies, sciences, and other concepts from Western countries. This enabled the insular nation to develop rapidly and become a powerful modern state.

Just as the Japanese embraced change during the Meiji era, we believe investors should embrace change in their portfolios by introducing greater global diversification. We think 2025 demonstrated the merits of geographical diversification and reminded investors that compelling opportunities exist outside the US. While we do not suggest cutting exposure to the US to zero, as it remains the deepest and most liquid equity market in the world, we view the weight of the US in standard global equity indices — typically over 60% (c. 62% in the MSCI ACWI) — as too high, given the potential challenges the US is facing.

Of all the major equity regions we have reviewed, the emerging markets are, in our view, the most compelling, thanks to a combination of attractive valuations relative to developed markets, higher earnings growth expectations, and strong structural growth themes. We also see a strong case for UK SMIDs, which trade at a discount to both their large-cap peers and their long-term averages. To us, this suggests an anomaly that could correct over time, with supporting dynamics already in place, such as M&A activity and interest rates having come down since 2024.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.