The myth of the ‘typical’ female retail investor

To mark International Women’s Day 2026, interactive investor’s Camilla Esmund explores whether the assumptions made about female investors stand up to scrutiny.

6th March 2026 13:10

by Camilla Esmund from interactive investor

interactive investor has launched a new Women’s Wealth and Investing hub with bespoke articles and educational insights to help inspire and inform.

The theme of International Women’s Day this year is “give to gain”, which is a powerful reminder of why we need a collaborative approach to tackling gender inequality. In the spirit of this, let’s change the way we all discuss the gender investment gap, and in doing so - move the agenda forward.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Why are we still labelling women as cautious? The problem with broad assertions is twofold: they’re inaccurate and they’re uninspiring.

This is the third year I’ve looked at this data and the message is consistent. Relying on inaccurate assertions impacts the way our industry is speaking to female investors. This means they may not be able to find the products suitable for them or that work towards their financial goals, or they could be put off investing altogether – perpetuating this divide.

The gap starts early and still isn’t budging

We know that fewer women are investing in the UK compared to men, and women are retiring with less financial security. If fewer women are investing, women are disproportionately missing out on compound growth over the years. Compound interest is an investment superpower; it should be supercharging women’s money and helping them build financial resilience.

Worryingly, Boring Money research found that young men are investing at double the rate of young women. Time is a great asset when it comes to investing, so these differences early doors mean bigger gaps down the line.

If investing isn’t on women’s radar as much as it is for men, especially at an early age – why is that?

It is not good enough to shrug and assume women are less interested in investing or more risk averse. The growth of the investment conversation between women (across various ages) on social media, for example, is case-in-point. There is appetite to invest. The reality is a lot more nuanced and there are major structural barriers which prevent women from investing, such as the pay gap and the so-called motherhood penalty.

Stereotypes about women’s approaches or attitudes to investing is not solving anything.

Let’s dive into the trends and truths behind women’s investment behaviours in the retail space, challenging long-held assumptions and unveiling how we can steer the conversation around women and investing into a more productive one.

Women don’t need more handholding

I polled investors about any barriers they found when it came to their investments.* Interestingly, both men and women cited “worrying about making the wrong decision” as their core barrier. This is illustrative of the fact that both men and women have similar fears when it comes to their investments; after all, investing in the markets always carries an element of risk.

And it’s not just our data that is showing this. Some thought-provoking research by The Wisdom Council** found that 21% of women asked about their investment approach self-certified as “a nervous investor” that struggles with investment jargon. 18% of men from their research sample said the same – only a 3% difference. 17% of women said they were “somewhat confident” but struggle with jargon, versus 23% of men. In this sample though, men were more likely to describe themselves as “confident” investors, who only occasionally struggle with jargon – 20% v 11% of women. That said, if you look across the range of responses in this research, you can see that men and women have similar approaches and concerns.

In this same Wisdom Council research, in response to this statement: “I feel confident handling my own financial affairs” very few male and female respondents strongly agreed or disagreed. In fact, most men and women in the research sample said they agree (73% of women, 77% of men). I’d argue this doesn’t point to a glaring confidence or capability gap. Similarly, over half of female respondents said they are “knowledgeable about financial issues and products”, which is encouraging.

Celebrating the success of female investors

I hope women at all stages of their investment journeys are inspired by this next point: women who are investing, are excellent investors. Both men and women on the interactive investor platform continue to invest very similarly, with very comparable portfolios yielding strong results.

Over the last six years, the average ii customer has seen their portfolio grow an impressive 48%, beating the aggregated performance of funds in the IA Mixed Investment 40-85% Shares sector (38.5%). Women’s average portfolio growth over that time has been around 46% on average - only 2% difference from the average male portfolio and still outperforming the IA Mixed Investment sector.

(Note – we use this IA sector as a comparator for private investor portfolios, given its mix of bonds, cash, and equities.)

6 years | 5 years | 4 years | 3 years | 2 years | 1 years | |

All ii investors | 47.7% | 43.1% | 26.6% | 39.3% | 27.8% | 15.7% |

IA Mixed Investment 40-85% Shares sector | 38.5% | 31.4% | 18% | 31.4% | 21.5% | 11.6% |

Performance data to 31 December 2025. Source: interactive investor/Morningstar. Past performance is not a guide to future performance.

Gender: performance comparison

6 years | 5 years | 4 years | 3 years | 2 years | 1 years | |

Women | 46.4% | 42.5% | 25.9% | 37.8% | 26.4% | 15.1% |

Men | 48.4% | 43.5% | 27.1% | 40.3% | 28.6% | 16.1% |

Source: interactive investor’s ii index Q4 2025.

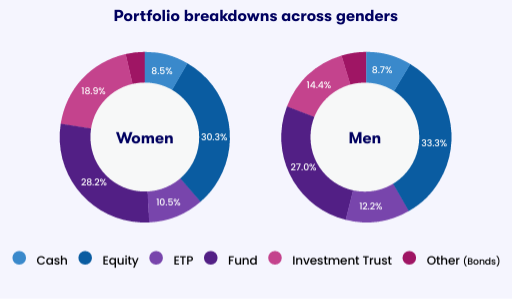

Portfolio deep-dive – spot the difference?

What’s driving this strong performance? Put simply, diversified and balanced portfolios, well-positioned to weather the inevitable ups and downs in markets. You can see in our data that portfolios between men and women are incredibly similar, invested across a range of assets.

There are minor differences: men have a slightly higher weighting to equities (33% versus 30%), where women will tend to allocate more to investment trusts (19% versus 14%). But the portfolio similarities are encouraging and show why we need to move away from any beliefs around differences in approach, and instead shout about how both men and women are staying invested and diversified – and it’s paying off.

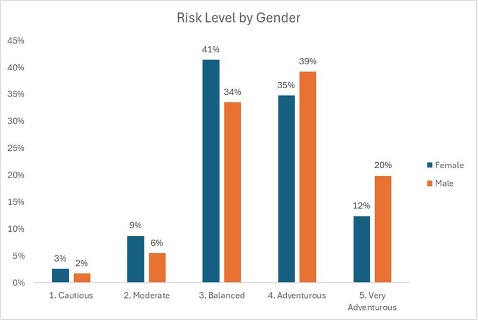

Are women actually more risk averse when it comes to investing?

I asked men and women how they would describe their risk preferences when it comes to investing*. “Moderately adventurous” was the most popular option for both men and women. On the flip side, “cautious” was the least popular answer for both men and women.

Let’s drill down into portfolios a bit further to see if we can identify differences in allocation to riskier areas of the market.

The AIM market - which is the smaller end of the market and often considered riskier - accounts for a very small percentage of both male and female portfolios on average.

When I looked at this data in 2024, men had a 4% exposure to AIM compared to 2% for women. So, men had double the exposure, but both had very small allocations overall. But this has since shifted – there’s now only a single percentage point difference, with men at 3% and women 2%. Not only does this help disprove that women are naturally more cautious investors, but it also shows that men being labelled as higher risk investors isn’t necessarily accurate, either.

Men | Women | |

FTSE 100 | 22% | 26% |

FTSE 250 | 12% | 14% |

FTSE OTHER | 5% | 5% |

FIXED INCOME | 3% | 4% |

INTERNATIONAL | 13% | 10% |

AIM | 3% | 2% |

I also looked at the breakdown of our ii Managed ISA portfolios. Investors can choose a portfolio which suits their investment goal, stage of life, and tolerance for risk.

12% of women have chosen “very adventurous” portfolios vs 20% of men, so an 8 percentage point difference – which is significant. Plus, we can also see more women have chosen “balanced” portfolios – 7% more than men.

Interestingly though, there’s only 4% difference between men and women choosing “adventurous” ii Managed ISA portfolios. Nevertheless, this is probably where we can see the most significant differences around risk appetite.

Below: ii Managed ISA portfolio breakdown by risk level

Do women just ‘buy and hold’?

It is also often assumed that men are more active traders than women, whereas women prefer to buy and hold (where an investor buys stocks and holds them for a long period regardless of fluctuations in the market). One’s investment approach always needs to be suitable for them, and them only. One approach for one person won’t be right for another, but it’s nuanced and individual – not based on gender.

Our data shows that men on ii are almost twice as likely to actively trade, but it’s only 15% of men compared to 8% of women, so relatively small proportions of men and women are frequently trading when you look at the bigger picture.

Buy and hold | Trading more actively | |||

2026 | 2025 | 2026 | 2025 | |

Female ii customers | 15% | 15% | 8% | 7% |

Male ii customers | 10% | 10% | 15% | 13% |

Additionally, when you look at how many male and female customers on ii have traded in the last 12 months, the differences are smaller. And, in fact, more women have traded in the last year than they did when I looked at this data two years ago.

Ratio of female and male customers who have traded on ii (12 months to 22 February 2026) | ||

Not Traded | Traded | |

Female ii customers | 48% | 52% (up from 48% in 2024) |

Male ii customers | 41% | 59% |

How can we move the conversation forward?

Ultimately, our data – although just a snapshot – indicates that many of the gender-based assumptions we have about women and investing aren’t reflected in the growing body of research.

We need to accurately reflect investor behaviour and the success of female investors. After all, 46% portfolio growth over 6 years, despite choppy markets, is setting a standard of excellence in retail investment, and that’s what we’ve seen from women investing through interactive investor.

It’s time to broaden the conversation and change how we frame it. As women, let’s speak to our peers, family and friends about investing. Hopefully, the myth-busting from this data can be brought into these conversations. Our research* found that over half of men we polled said they speak to friends about investing (53%), whereas for women it was 48%. I’d love to see these percentages rise for both men and women.

One way you can join the conversation is by checking out ii Community – free for all interactive investor customers, allowing users to share thoughts and ideas with other investors across a range of topics.

Women sharing their positive experiences with investing will inspire others to start, or to build on theirs. And if we can stop using generalisations, we can avoid women feeling patronised, or isolated. This will inspire young women to start investing earlier, and it will show women in later stages of their life that is never too late to make a difference to their long-term wealth.

Sources

Note – with the exception of ii’s Managed ISA data, the data is across all accounts – ISA, GIA, and SIPP.

*interactive investor poll conducted on the ii website in February 2026 with over 1,000 respondents.

** The Wisdom Council – Consumer Understanding Research (Investors) 2023 – note, all respondents held investments and this included some individuals who were in their DC workplace pension but may not have identified as investors.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

interactive investor (ii) is an Aberdeen company. Aberdeen advise ii on the fund selection for the Managed ISA portfolios. The portfolios contain funds predominately managed by Aberdeen but may also include funds managed by other third-party managers. Please review the portfolio factsheets for more details on the underlying funds. Find out more about how ii and Aberdeen work together.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.