Stockwatch: have directors bagged a FTSE 100 bargain?

After falling by almost a quarter from last month’s near-record high, analyst Edmond Jackson discusses the odds of recovery at this blue-chip and why directors might have decided to buy.

17th March 2026 10:55

by Edmond Jackson from interactive investor

Has Melrose Industries (LSE:MRO) taken a plunge too far? Does it genuinely rate as a long-term “buy” – one to tuck away – or is it nowadays more a near-term trading chip?

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Interestingly, yesterday, and with the share price at about 500p, the shares had fallen the same 23% as easyJet (LSE:EZJ) since conflict erupted in the Middle East. You’d think an airline share would be more sensitive to the current situation than a manufacturer of aerospace engines and airframes products across civil and defence markets.

Wouldn’t generating 29% of revenue from defence be a decent hedge against 71% from the civil sector? Maybe enough investors remain spooked by the 66% drop in Rolls-Royce Holdings (LSE:RR.) during Covid, although the shares then multiplied 19x from that low.

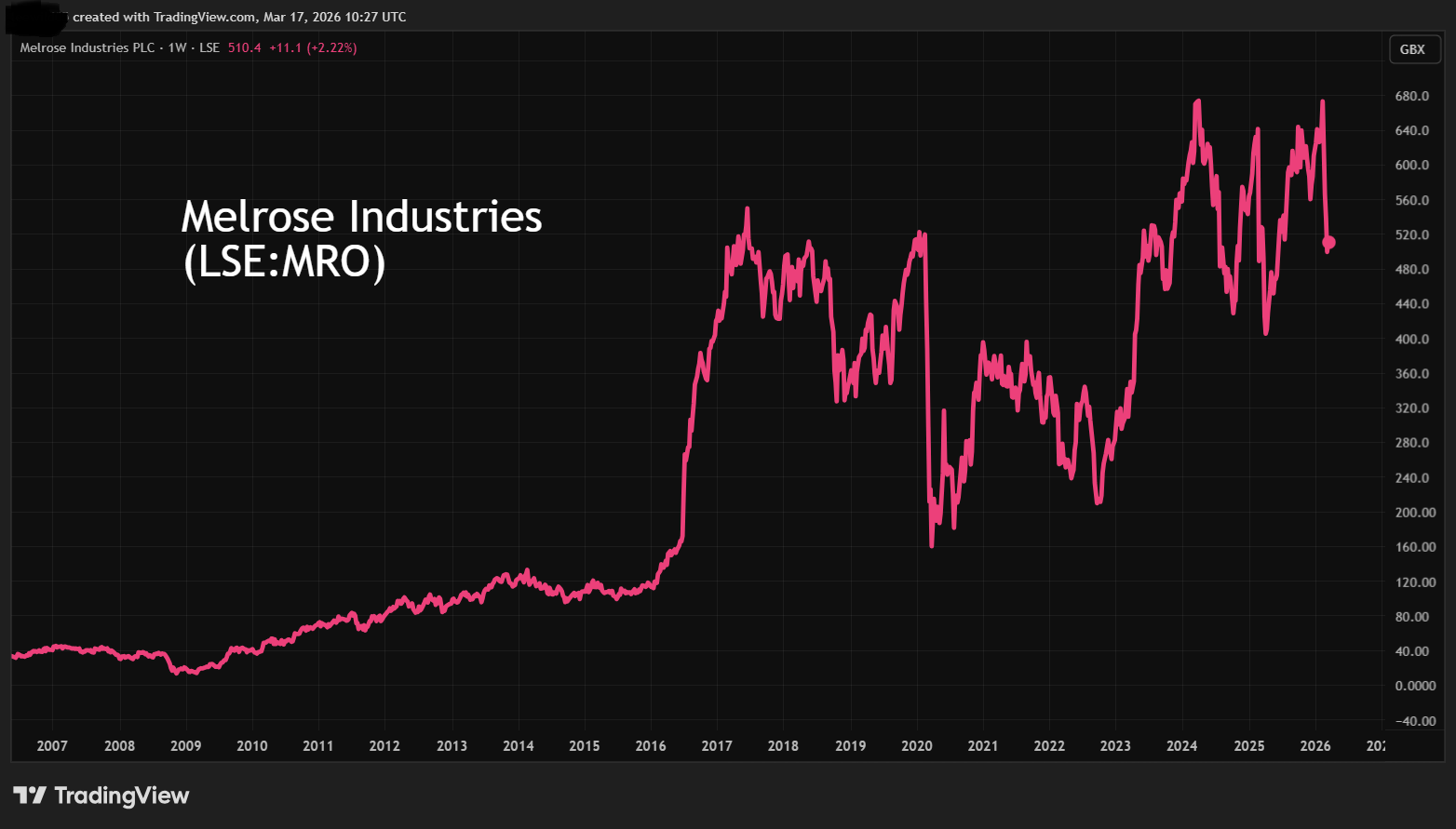

Currently capitalised near £6.4 billion after yesterday’s recovery to 508p, Melrose shares have been volatile since October 2023. Its quasi-Rolls-Royce period was back in 2016 when the shares began soaring from around 150p to over 500p before a slump to 170p with the onset of Covid in March 2020. It has been quite a roller coaster for shareholders:

Source: TradingView. Past performance is not a guide to future performance.

Attractive PEG ratio and director share buying

The “all bets are off” scenario is if consensus forecasts are fair: 2026 and 2027 each herald 23% earnings growth which, due to a forward price/earnings (PE) ratio below 13x, implies an attractive PEG (PE/growth) ratio of 0.7 (notionally you are looking for below 1.0). This also assumes consensus for £3,871 million of revenue in 2026, a modest downgrade from expectations for close to £4 billion in guidance given at the 27 February annual results.

At least it appears that an aspect of disappointment within the otherwise strong 2025 results, is factored into these forecasts, which contributed to the shares falling from 640p to 566p on results day.

Moreover, last year Melrose set out five-year targets to 2029, including £5 billion of revenue, over £1.2 billion of adjusted operating profit and £600 million free cash flow. If achievable, it implies a PE more like 9x currently.

Obviously, many equity-related forecasts are being put at risk if the world faces an energy supply crisis akin to 1973-74, more likely if tankers remain compromised in the Strait of Hormuz.

- Insider: these directors lock in 7% yield at a discount

- Funds worth watching as Middle East conflict grinds on

Meanwhile, Melrose’s current market share price is a circa 11% discount to the 559p per share paid by a new non-executive director who bought £111,840 worth on 3 March. The next day, the chair added £96,579 worth, having also been a substantive buyer at 400p and 567p in April 2025 and December 2024 respectively. His buying is no “obligatory first purchase” like non-executive directors are expected to make, yet that the chair is only just breaking even with his trading may imply how tricky this share can be. However, one should not forget that it’s the long run that really counts.

Possibly a modest 1.8% dividend yield fails to smooth volatility. The board seems less keen to ramp up the payout any further than the 20% growth in each of 2024 and 2025, despite nearly 4.5x earnings cover. Probably its dilemma has been a volatile record of cash generation versus capital expenditure needs, although free cash flow last year turned around from negative to £125 million. Management proclaimed “an inflection point with substantial further increases in cash generation to come” although this is not marked by a greater increase in dividends. Instead, like many companies, it has announced a new 12-month share buyback programme worth £175 million.

Melrose Industries - financial summary

Year-end 31 Dec

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£m) | 7,132 | 6,650 | 2,954 | 3,350 | 3,468 | 3,589 |

| Operating margin (%) | -6.8 | -7.4 | -8.3 | 1.6 | -0.1 | 16.7 |

| Operating profit (£m) | -487 | -493 | -246 | 53.0 | -4.0 | 600 |

| Net profit (£m) | -536 | 833 | -308 | -1,019 | -49.0 | 370 |

| Reported earnings/share (p) | -39.0 | -30.9 | -16.6 | 0.1 | -3.8 | 29.0 |

| Normalised earnings/share (p) | 1.9 | 0.4 | -6.0 | 17.4 | 19.5 | 30.8 |

| Operating cashflow/share (p) | 52.4 | 16.8 | 14.5 | 2.2 | -9.3 | 16.8 |

| Capital expenditure/share (p) | 23.1 | 15.2 | 21.2 | 7.9 | 9.4 | 7.5 |

| Free cashflow/share (p) | 29.3 | 1.6 | -6.7 | -5.7 | -18.7 | 9.3 |

| Dividend/share (p) | 2.5 | 5.3 | 7.0 | 5.0 | 6.0 | 7.2 |

| Covered by earnings (x) | -15.6 | -5.9 | -2.4 | 0.0 | -0.6 | 4.0 |

| Return on capital (%) | -3.4 | -4.5 | -2.2 | 1.0 | -0.1 | 10.2 |

| Cash (£m) | 311 | 473 | 355 | 58.0 | 88.0 | 166 |

| Net debt (£m) | 3,335 | 1,268 | 1,507 | 764 | 1,558 | 1,737 |

| Net assets/share (p) | 486 | 515 | 527 | 268 | 221 | 225 |

Source: company accounts.

As yet, this financial record is very mixed, for example operating margins and return on capital only becoming meaningful in 2025. Dividend cover – if at all – has similarly been weak until lately. If “investment grade” constitutes a proven financial record, then Melrose is yet to manifest it. Much appears to depend on forecasts and the macro context.

On the other hand, and especially with a restructuring programme “nearing completion with full benefits expected in 2026 and beyond”, it seems conceivable that Melrose attracts a takeover bid from the US.

A decent pitch at the 2025 results

Melrose’s engines and structures divisions typically provide technology for more than 100,000 flights a day, supporting its claim of strong positions “on the world’s leading aircraft...structural demand from record order and increasing aftermarket requirements set to continue, we are well placed to deliver further profitable growth and increased cash generation in 2026 and the years ahead”.

The share price hit was down to revenue guidance of £3.75-3.95 billion, which was shy of consensus estimates at around £4 billion. Also, the 2026 adjusted operating profit range is down from £650-690 million to £620-650 million. It does not appear that cash conversion is improving since guidance is for £100 million free cash flow.

Meanwhile, net debt has crept up 6.5% to £1,407 million versus net assets of £2.8 billion including £2.7 billion goodwill/intangibles.

This feels a bit hard to square with “restructuring benefits in 2026 onwards...” Admittedly, the macro context – even before the war on Iran – has been challenging, with weak supply chains continuing to affect aerospace operations, something which is liable to persist.

- Shares for the future: why I’ve put trading blocks on three shares

- Stockwatch: what next for these banks after spectacular recovery?

A stronger pound and weaker dollar have affected translation of results, where 91% of revenue in 2025 was derived from the US (the location of operations avoiding tariffs). More positively, if war persists, then the dollar is likely to continue or at least retain its recovery since end-January 2026.

The 2025 income statement shows revenue up 8% to £3,589 million and adjusted operating profit up 23% to £647 million, giving an 18.0% margin. Reported operating profit of £600 million benefited from cutting expenses by 55% to £354 million. However, net finance costs were 29% higher at £132 million (on net debt of £1.4 billion), which slightly checked the pre-tax profit turnaround to £468 million.

Profit was significantly driven by higher engines and defence demand “together with the positive impact of our multi-year transformation programme reading through”. Engines revenue growth was 15% to £1,632 million, with “good” growth in engine repairs in the second half.

Management proclaims the group is “well positioned to benefit from expected production ramp-ups and ongoing aftermarket expansion”, and a multi-year transformation programme has provided an “excellent foundation for growth”.

Discerning such essentials explains why the shares are volatile, and it possible to derive optimism and caution alike.

Modest if notable short selling

Checking the register of short positions, only 1.54% of the issued share capital is loaned out, but given this is a £6.4 billion company, there could be more lurking below the 0.5% disclosure threshold. The disclosed short position has been roughly this low going back to 2018, with a couple of big spikes to near 30% in August 2016 and 18.5% in April 2018. Yet one of the two traders currently disclosed slightly increased its short on 27 February (annual results day) and the other on 9 March.

Versus soundbites on prospects – likely put together by PR professionals – and money risked by short-selling experts, I have to say the shorters tilt me toward near-term caution. They must factor in share borrowing costs and dividend payment obligations, hence the need for conviction. Versus the like of Greggs (LSE:GRG) – London’s second most-shorted share at 13.5%, having spiked from 1.0% last June – there is not exactly scope for a short squeeze in Melrose when perception of declining prospects eases.

- Want to pay less tax? Here are five allowances to use by 5 April

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

In the near term, it appears support kicked in at around 500p, yet, as for any airline-related share, much depends on how and when the Middle East conflict and oil/jet fuel supply settle.

If conflict abates, then shares like this will respond well – and genuinely, if energy supply is secured. For now, the US is flailing around to attract a huge logistical support to achieve secure passage of all tankers. Meanwhile, Iran can use covert means to threaten those serving US allies.

Benefits of restructuring, strong market positions and longer-term takeover possibilities are reasons to have Melrose on a watch list. On an investment rather than trading view, my current stance is “hold”, chiefly because the Iran war looks another fine mess the US has created in the Middle East.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.