Stockwatch: what next for these banks after spectacular recovery?

A year after making a very profitable call on these shares, analyst Edmond Jackson reviews them again and updates his rating.

13th March 2026 11:28

by Edmond Jackson from interactive investor

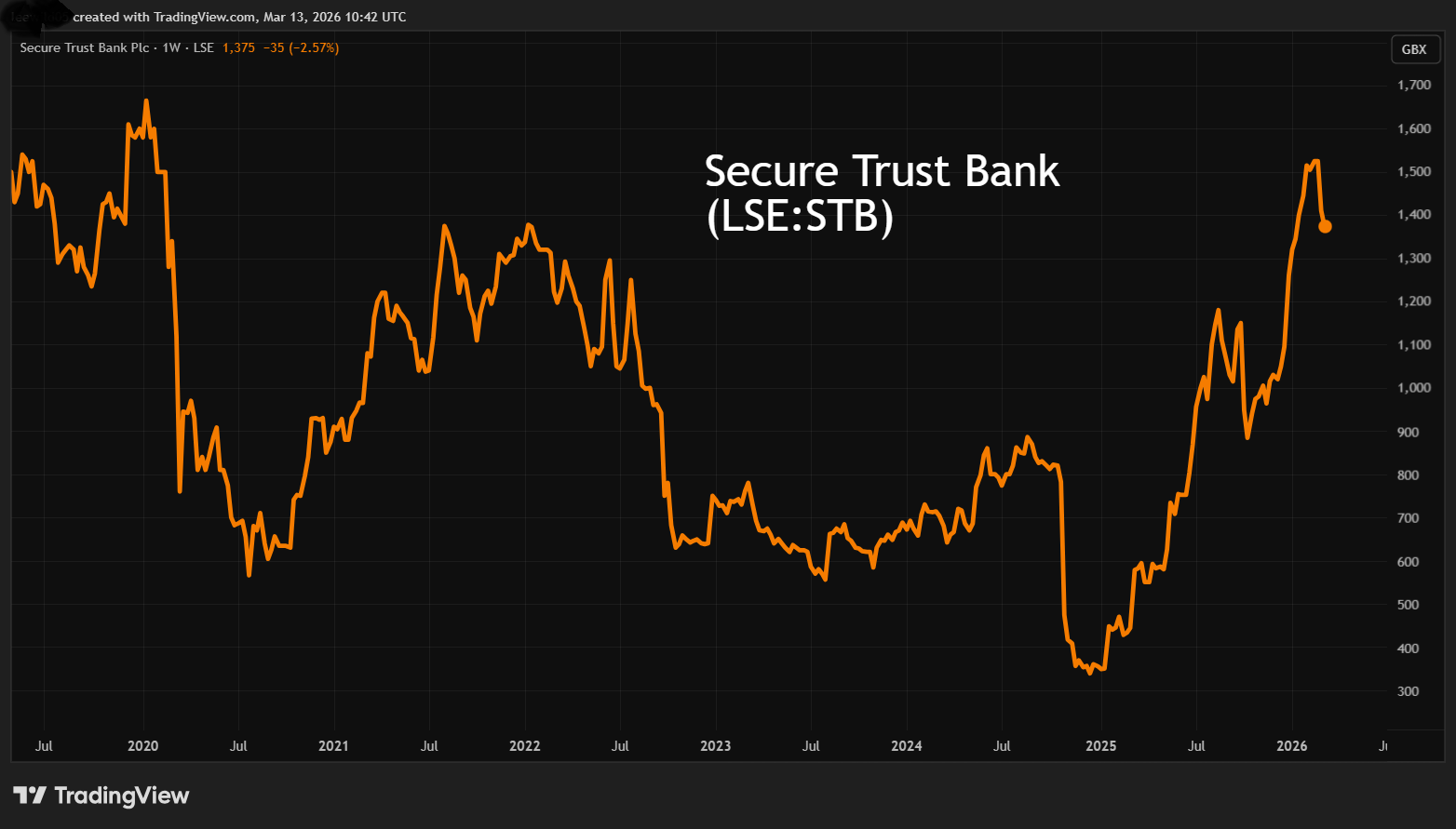

A year ago, I detailed “buy” stances on Secure Trust Bank (LSE:STB) at 580p and Close Brothers Group (LSE:CBG) at 275p as the car finance mis-selling furore came to a head with a Supreme Court ruling due.

- Learn with ii: What is Bed & ISA?| Open a Stocks & Shares ISA | ISA Offers & Cashback

Charts implied both shares had bottomed, Secure at around 350p and Close at 185p, as if spooked investors had sold out. The lows implied valuations down to around 0.3x tangible book versus estimated provisions of only 0.06x, the prevailing market value for Secure and 0.4x for Close.

A year previous, Barclays (LSE:BARC) and Metro Bank Holdings (LSE:MTRO) had shown that 0.3x tangible book was a highly profitable turning point.

I thought that both shares merited accumulating. I said, “unless the Supreme Court truly has a mind of its own, I suspect the authorities have learned from the PPI fiasco, not to sling an albatross around banks’ necks”.

Events have borne this out with Secure currently at 1,400p and Close 417p.

Source: TradingView. Past performance is not a guide to future performance.

Yet Secure’s shares were quite volatile yesterday despite robust 2025 results and some attractive valuation criteria. I believe this reflects investor wariness as to the effects of the Middle East war on energy prices and the wider economy. It is already evident in sentiment towards residential property buying and, while Secure and Close are exposed to commercial property lending, I would expect businesses to be more cautious about such commitments if the UK economy turns down.

This morning’s data shows the UK economy flatlining in January after only a 0.1% rise in gross domestic product in December

While I believe any severe downturn would require Brent crude oil to be up near $150 a barrel rather than testing $100 currently, that could be roughly where prices head if Gulf oil production and supply remain compromised.

It is a general dilemma for holding financial shares given that they are relatively more sensitive to the economy. A slowdown reduces demand for credit, and recession increases bad debts. Despite its 7.4% prospective yield, M&G Ordinary Shares (LSE:MNG) fell 4% yesterday after in-line 2025 results, as asset managers tend to be a geared play on markets.

- M&G back to positive flows and maintains dividend appeal

- Trading Strategies: is now the time to buy IAG shares?

At current levels, Secure offers only a 2.7% prospective yield albeit with 8x expected earnings cover. Even if forecasts need downgrading, the table shows a strong if volatile cash flow profile, often providing even greater cover.

Secure Trust Bank - financial summary

Year-end 31 Dec

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 153 | 166 | 167 | 150 | 170 | 185 | 204 | 214 |

| Operating margin (%) | 22.7 | 23.3 | 12.0 | 37.4 | 22.9 | 19.5 | 14.3 | 12.9 |

| Operating profit (£m) | 34.7 | 38.7 | 20.1 | 55.9 | 39.0 | 36.1 | 29.2 | 27.5 |

| Net profit (£m) | 28.3 | 31.1 | 16.2 | 45.6 | 33.7 | 24.3 | 19.7 | 17.6 |

| Reported earnings/share (p) | 151 | 166 | 87.0 | 244 | 153 | 137 | 101 | 89.0 |

| Normalised earnings/share (p) | 151 | 166 | 87.0 | 244 | 153 | 162 | 136 | 227 |

| Operating cashflow/share (p) | -443 | -1,098 | 514 | -517 | 170 | -236 | 575 | 1,326 |

| Capital expenditure/share (p) | 13.3 | 35.3 | 10.2 | 7.0 | 14.0 | 14.0 | 5.2 | 10.4 |

| Free cashflow/share (p) | -456 | -1,133 | 503 | -524 | 156 | -250 | 570 | 1,316 |

| Dividend/share (p) | 83.0 | 20.0 | 44.0 | 61.1 | 45.1 | 32.2 | 33.8 | 35.5 |

| Covered by earnings (x) | 1.8 | 8.3 | 2.0 | 4.0 | 3.4 | 4.3 | 3.0 | 2.5 |

| Return on total capital (%) | 1.4 | 1.4 | 0.8 | 1.9 | 1.1 | 1.0 | 0.7 | 0.5 |

| Return on equity (%) | 12.7 | 12.7 | 6.2 | 16 | 9.4 | 7.9 | 5.6 | 5 |

| Cash (£m) | 215 | 154 | 245 | 286 | 421 | 405 | 469 | 560 |

| Net Debt (£m) | -164 | -99.1 | -190 | -232 | -367 | -310 | -374 | -465 |

| Net assets per share (p) | 1,283 | 1,375 | 1,452 | 1,622 | 1,749 | 1,811 | 1,890 | 1,954 |

Source: historic Company REFS and company accounts.

Tangible book value rose 5.8% last year to 1,973p per share, hence a market price of 0.7x, alternatively expressed as a 27.5% discount. Be careful in assuming that it’s a prop as effective as yield: Barclays fell 5% to 389p yesterday on 0.8x tangible book and a 3.5% yield.

But if consensus forecasts for Secure are roughly fair – for around £60 million net profit this year and normalised earnings per share (EPS) near 300p, representing 66% annual growth - then the forward price/earnings (PE) ratio would be 4.7x, generating a PEG (PE/Growth) of 0.1x. I would treat such with a pinch of salt, however, given that interpretations of EPS can vary, the company presenting basic EPS at 2.5x total basic EPS.

There still appears significant scope to absorb downgrades, although with shareholders sitting on recent big profits here – and in other banks – I am wary that the direction of travel in forecasts could tilt sentiment.

2025 results are good in parts

Lending balances grew 8.1% last year to £3.3 billion and deposits similarly to £3.5 billion. Management targets around 10% growth on which it bases the expectation to raise average return on equity over 16% versus a slip last year from 14.6% to 14.3%.

Pre-tax profit from continuing operations was £59.3 million versus £59.4 million, maintaining a net interest margin (the difference between what is earned from loans and paid out on deposits) of 4.7%.

Disposal of the vehicle finance business last December for a £9 million net gain has enabled Secure to focus on core operations of savings deposits, property finance and business finance. Management emphasises “large investable scale markets” and “refreshed strategic priorities” – of product expansion, effective digital solutions and capital discipline – able to deliver higher returns. That’s good, although I would say that it depends what the economy allows, and feel these are actions any bank should be doing normally.

From an economist’s perspective I also find it intriguing how banks like this are optimistic about lending, versus the Begbies Traynor red flag report that regularly cites UK corporate financial distress reaching new record levels. Trusting what the optimistic banks say on lending prospects appears to assume a dual UK economy, which may indeed be fair. The red flag report’s negative bias may reflect how weak businesses were kept from administrators by past government and central bank stimulus measures as well as ultra-low interest rates.

- Want to pay less tax? Here are five allowances to use by 5 April

- Where investment professionals are investing their ISA

Also of note is the way “strong new business lending up 8.1%” was divided between real estate up 9.4% and commercial finance up 3.2%. The latter could be said to be near flat in inflation-adjusted terms – and inflation is expected to rise – while I feel real estate actions are exposed to the effects of war.

Yesterday, global real estate services group Savills (LSE:SVS) declared 2025 underlying EPS up 17% and dividends up 12%, yet its shares fell 7% to 935p despite only a modest forward PE of 11, a conceptually attractive PEG of 0.9 and a 4.0% yield. It seems the market is already targeting cyclical shares to mark down, although modestly for now.

One can similarly say of Secure that it is a well-run business on seemingly attractive valuation measures, assuming the economy allows management to achieve its objectives.

Close has a 31 July financial year-end, hence it reported results in September. Its performance is, however, in the frame given interim figures to 31 January were released on 18 March. Otherwise, there hasn’t been any meaningful update recently.

Last January, RBC Capital Markets upgraded the shares to “outperform” from “sector perform”, raising its price target from 475p to 625p. RBC’s rationale was “meaningful cost efficiencies to extract, which are not fully reflected in consensus expectations”. I suggest that Close shares being down nearly 20% since this note shows the importance of macro expectations.

Strong record of director buying at Secure continues

It was a key factor in my rating Secure “buy”: four directors bought a total £435,500 worth over 800p in 2024, before the motor finance commissions’ probe was launched that October. It hinted they perceived value without the motor issue.

Three of them continued buying early last July: a total £579,000 worth at prices from 848p to 884p. This included the chair and CEO who continued to buy. The chair snapped up £234,000 at 1,170p last August and £229,000 at 916p in October; the CEO, £249,000 at 878p also in October, also £497,000 at 1,288p in January.

It is refreshing to see a CEO make sizeable serial cash purchases rather than be reliant on options like so many are nowadays, exercising and selling enough options to pay tax and maybe lock in some profit.

As yet, there is no profit-taking by insiders now that the pre-results restricted period is over.

A year ago, it also encouraged me how three Close directors had bought – although relatively modestly – at around 420p, although the pattern since has all been options exercising and selling.

Near-term ‘hold’ stances at best

If the economy does turn down, risks to banks do not seem as great as they were in 2007, and both Secure and Close are over the motor finance mis-selling fiasco. Close similarly trades on a PEG of 0.1x – for what forecasts are currently worth – although dividend restoration (since a cut from 67.5p per share for the July 2023 year) is not expected until a 19.3p payout for the year to July 2027.

However, the downside implications of a protracted Middle East war – this time compromising energy – make me wary of financial shares right now. I like Secure for its managerial initiatives and look forward to what Close has to report, hence I broadly rate them a “hold”, but you need to decide your risk preference.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.