Open a Self-Invested Personal Pension (SIPP)

Invest in a better value pension

- Combine your pensions and pay a low, flat fee from £5.99 a month

- Build a secure future with a wide range of investments

- Retire comfortably and join over 500,000 ii investors

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. Tax treatment depends on your individual circumstances and may be subject to change in the future. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

Investing should feel rewarding

Start investing with ii and give your savings more time to grow this summer.

Open an ii Personal Pension (SIPP) and enjoy £200 cashback when you deposit or transfer a minimum of £20,000. See more details on this offer.

Offer ends 30 June 2026. New customers only. Terms and fees apply.

Important information: It’s important to take your time before transferring your pension. Make sure to consider what the best option is for you. Don’t transfer just to qualify for the offer, and don't rush any decision to meet the offer deadline. We periodically run offers, and there will likely be other opportunities in the future.

Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions.

What is a Self-Invested Personal Pension (SIPP)?

A Self-Invested Personal Pension (SIPP) is like any other pension but with more control, more flexibility, and more choice over building the retirement you deserve.

Save on tax

Invest up to £60,000 each tax year and get at least 20% tax relief from the government - for every 80p you contribute, it’s topped up to £1.

Choose where to invest

It’s up to you how you achieve your retirement goals. Choose exactly what to invest your pension in and adjust anytime.

Retire on your terms

You can withdraw from your SIPP in various ways, including tax-free cash, income drawdown, lump sums, or a combination to suit you.

SIPPs explained

Let our Personal Finance Editor Craig Rickman talk you through what a SIPP is and why you might want to open one.

Investing with a low-cost SIPP, like the ii SIPP, gives you a greater opportunity to grow your savings for the retirement you want.

Is a SIPP right for you?

A SIPP may be right for you if:

- You want a say over how your pension is invested

- You want greater flexibility over how you take retirement income

- You're self-employed

- You want to combine your pensions

- You're happy to leave your money invested until you're at least 55 (57 in 2028)

If you're unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

Lower costs

You can rely on our flat fee and can keep more of what's rightfully yours.

Wider choice

Benefit from a wide range of investments, flexible retirement options and expert picks.

Greater support

Rest easy knowing our award-winning Customer Support team is here for you.

Simple and transparent pension charges

Unlike percentage-based fees charged by many providers, with ii you will always pay a low, flat fee. This could dramatically increase your retirement wealth over time.

Start on our Core plan at £5.99 a month and upgrade when you want access to a wider range of benefits - or when your portfolio grows above £100,000.

It’s a transparent, cost-effective way to invest in your pension, with everything you need in one place.

Get started from £5.99 a month

- Add an ISA and Trading Account at no extra cost

- Free regular investing

- No additional charges when making pension withdrawals

- Buy and sell investments from £3.99 per trade

- Free family accounts (upgrade to Plus)

- 1 x Free monthly trade (upgrade to Plus)

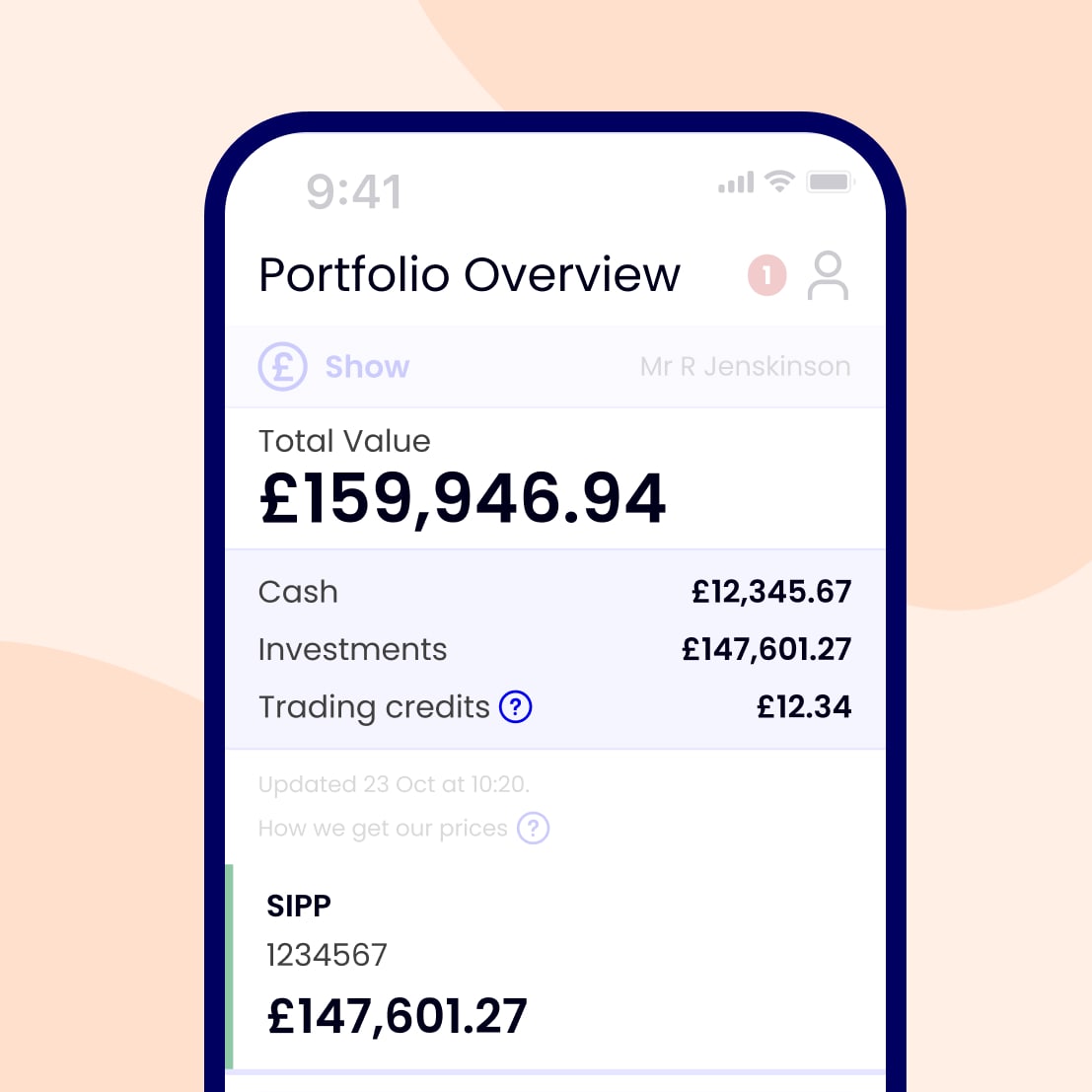

How we calculate your ii pension charges

Ella has a SIPP valued at £205,000 and holds no other ii accounts. Her pension portfolio is split between funds, shares, and cash.

Ella contributes £500 per month to her pension using ii’s free regular investing service, but does make the occasional trade.

So Ella’s total charge for the month is £16.48 made up of:

- Plus plan - £14.99

- £500 monthly investment - free regular investing

- 1 fund trade - £1.49

Important note about charges: The investments you choose may have their own charges, such as charges from a fund manager. These are in addition to our account charges. Other charges including foreign exchange (FX) fees, may apply.

Fang is building towards her retirement goals with ii

“Once I heard flat fees, I jumped at it. I calculated all my other fees and I said ‘that’s really expensive compared to ii’. Why did I not do it earlier? That’s why I’m with ii.”

Fang says she isn’t an investment expert but still felt it was important to achieve the retirement she wants. With ii’s low, flat fee, she can get on with what matters most to her and save more of her money.

Open your ii SIPP in 3 simple steps

It’s quick and easy to open a pension. You can set up personal contributions through one-off payments or a regular, monthly Direct Debit.

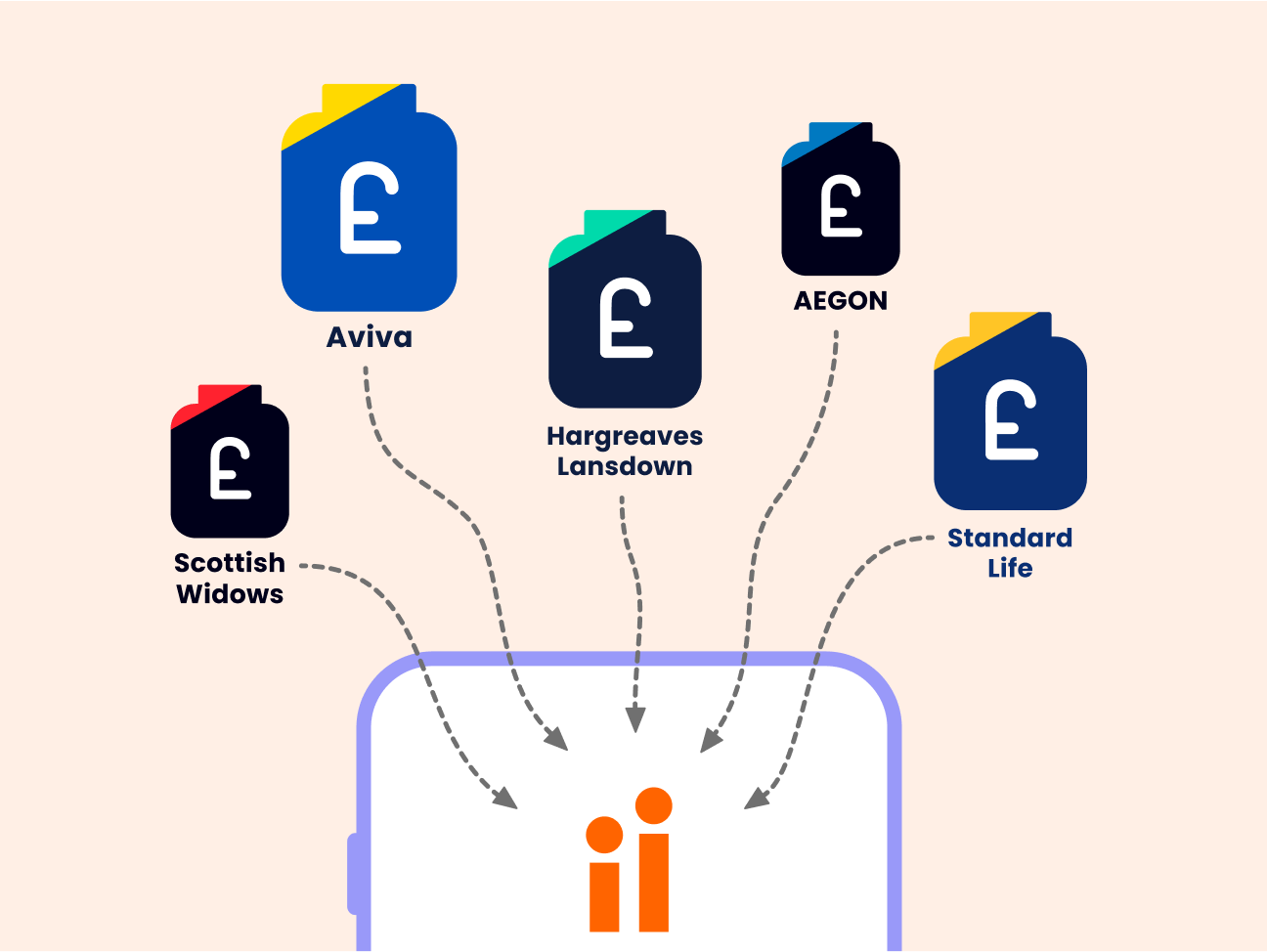

You can also transfer any existing pensions to your SIPP using our simple online process.

Once you've set up your account, choose from our wide range of shares, funds, bonds, and more.

Remember, you can change your investments at any time, to reflect your changing needs - before and during your retirement.

Check out the different ways you can access your pension when you reach age 55 (57 from 2028) with the ii SIPP.

Need inspiration for SIPP investments?

As well as offering a range of shares, funds, ETFs, investment trusts, and more, we also have a collection of ready-made options exclusive for ii investors.

ii SIPP Selected Growth Option

Our SIPP Selected Growth Option is a low-cost investment, carefully chosen by our experts to help meet common retirement investing goals.

Investment Pathways

Investment Pathways are four simple, low-cost options for investing your drawdown funds, chosen by our experts.

Highly Rated Funds

The Highly rated funds tool is a selection of funds, investment trusts and ETFs that hold strong analyst ratings from our Data provider, Morningstar.

Quick-start Funds

Our Quick-start Funds are an ideal way to get started with your pension. These low-cost funds have been specially selected by experts, and many experienced investors rely on them too.

Transfer your pension

Got too many unloved workplace pensions? Or SIPPs you’re overpaying for elsewhere?

Whatever your pension problem, ii has the answer with more control and lower costs.

Transfer for free today with our simple online process.

SIPP FAQs

A SIPP works much like any other pension, but gives you more control and flexibility over how it is invested.

While most pensions are invested in the stock market in some way, many offer a limited choice of investments. With a SIPP you can choose from a wide range of funds, shares, ETFs, Investment Trusts and more.

If you need help with choosing investments, we've made it easy to get started with our Quick-start Funds and other investment ideas.

With ii, if you transfer your pension as a cash payment, it usually takes between 2 to 6 weeks to complete. For cash transfers, you must sell your existing stocks before transferring.

If you’d like to keep your existing investments, the transfer will take longer. It usually takes 8 to 12 weeks but it depends on the type of investments you hold.

The length of time the transfer takes will also be reliant on how quickly your current provider works with us to complete it.

If you’re transferring a defined benefit pension or a Small Self-Administered Scheme (SSAS), the timeframes shown are not representative. For these schemes, given the increased level of due diligence that providers are required to carry out, transfers may take considerably longer.

Whether it costs money to transfer a pension depends on your provider. Some providers do charge transfer fees while others do not. Check if, and how much, you will be charged before transferring. It’s free to transfer pensions into an ii SIPP, but you may be charged by your current provider for transferring out.

Yes, you can do a partial pension transfer. However, if your funds are fully crystallised with your current provider, you can’t do a partial transfer and a full transfer will be required instead. So, it may be worth checking with your current provider before starting the transfer process.

If you’re able to transfer, you'll be asked if you want to transfer all stocks/cash (an 'in specie'/full transfer) or specific stocks/cash only (a partial transfer).

If the investments you want to transfer are not available with ii, you'll need to sell them first or keep them with your existing provider.

If you’re drawing an income from your pension, please note this will not be available during the transfer.

Still have questions? We have plenty more advice about transferring a pension to ii.

You aren’t always required to speak to a financial adviser before transferring a pension. However, we recommend doing so.

It’s a legal requirement to seek qualified financial advice before transferring a defined benefit pension worth more than £30,000. The advice must be a positive recommendation to transfer, and you will need written confirmation from them that it’s in your best interest before you can transfer.

If you have a defined contribution pension scheme and are 50 or over, then you can access free, impartial guidance on your pension options by booking a online face to face or telephone appointment with Pension Wise, a service from MoneyHelper.

If you’re under 50, you can still access free, impartial help and information about your pensions from MoneyHelper.

You can contribute more than your annual allowance, but you cannot claim tax relief on contributions which exceed your annual allowance.

If you claim tax relief on contributions which exceed your annual allowance, you may be subject to an annual allowance charge. The excess will be added to your taxable income for the tax year. You’ll need to declare this when completing and submitting your self-assessment tax return to HMRC.

However, your annual allowance could be more than £60,000 if you qualify for "carry forward".

There is no age limit on contributing to a SIPP, although you will only receive tax relief on your contributions up to age 75.

If you do not start taking a regular income, you can continue to contribute up to £60,000 a year to your SIPP until you reach 75, providing you have sufficient earnings.

If you've made a taxable withdrawal, your annual allowance for contributions falls to £10,000. You can choose to start making withdrawals at any time after reaching the age of 55 (57 from 2028).

The most you can contribute to a SIPP in a tax year is £60,000. You may be able to contribute more than £60,000 if you qualify for carry forward.

Thinking about a SIPP?

Our free Essential Guide to SIPPs has everything you need to know to help you get started. It covers what a SIPP is, how it works and whether it’s right for you.