The funds capturing the oil price surge

Saltydog Investor considers the return of the energy fund, and what might influence its prospects.

10th March 2026 09:16

by Douglas Chadwick from ii contributor

This content is provided by Saltydog Investor. It is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Rising tensions in the Middle East have pushed oil prices higher and brought energy funds back into focus.

At Saltydog, we are great exponents of unit trusts and open-ended companies – they are well regulated, easy to trade, and give great exposure to global markets. They can also provide access to most major market trends.

However, if you want to capitalise on very specific short-term market movements then exchange-traded funds (ETFs), which we also cover in our analysis, are sometimes a better bet.

- Invest with ii: Top ETFs| Index Tracker Funds | FTSE Tracker Funds

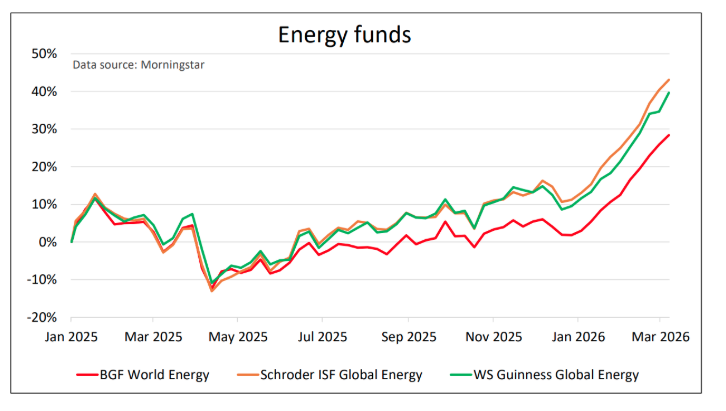

Having said that, although oil prices have spiked in the last few days, energy funds have actually been doing well for quite some time.

There are not many relevant funds domiciled in the UK, and so we also include some offshore funds in our analysis. Here are our leading three at the moment.

Past performance is not a guide to future performance.

There may be a long-term transition to renewables, but oil is still hugely important to the global economy. It remains essential for transport, petrochemicals, aviation and shipping, and is still one of the most important commodities traded in the world. It is also politically important. Most oil is traded in US dollars, which helps reinforce the role of the dollar as the world’s reserve currency and ties the oil market closely to the global financial system.

For much of the 20th century the global oil industry was dominated by a small group of large international companies known as the “Seven Sisters,” including companies such as Exxon Mobil Corp (NYSE:XOM), Chevron Corp (NYSE:CVX), BP (LSE:BP.) and Shell (LSE:SHEL). Today, the picture looks very different. A large share of the world’s oil is now produced by companies owned or controlled by governments, known as national oil companies. Examples include Saudi Aramco in Saudi Arabia, Rosneft in Russia and the National Iranian Oil Company. The revenues generated by these companies are a major source of funding for their governments.

This is where the idea of the “fiscal breakeven” oil price becomes important. It refers to the oil price a country needs to balance its national budget.

Saudi Arabia provides a good example. It is one of the lowest-cost oil producers in the world, but the government still needs oil prices somewhere around $90 a barrel to balance its budget. Oil revenues fund a large share of public spending in the kingdom, including major infrastructure projects and the Vision 2030 programme designed to diversify the economy.

- Fund Focus: what the Iran conflict means for your portfolio

- Ian Cowie: an investment trust to hold in febrile times

Saudi Arabia is not unique. Other major oil-exporting countries face similar pressures. Russia, for example, relies heavily on oil and gas revenues to support its federal budget, particularly since the invasion of Ukraine and the sanctions that followed. Iran faces similar constraints, which is particularly relevant given the current tensions in the region. Oil exports remain an important source of revenue for the Iranian government, helping explain why developments in the region can have such a strong influence on global energy markets.

Commercial oil companies operate very differently. Their primary concern is whether producing oil is profitable.

Thanks to technological advances and improved efficiency, many large international oil companies can operate profitably at far lower prices than many producer countries require. In simple terms, commercial oil companies can often make money at around $40, while some oil-producing countries need prices closer to $80 or $90 just to balance their budgets.

Another important development over the past decade has been the rise of US shale production. Advances in drilling technology, particularly hydraulic fracturing and horizontal drilling, have transformed the economics of oil production in the United States.

Much of this growth has taken place in the Permian Basin, which stretches across western Texas and southeastern New Mexico. The basin covers an area comparable in size to the UK and has become one of the most productive oil regions in the world.

Political slogans such as “drill, baby, drill” may grab headlines, but the real shift has been technological. Shale production has made US oil output far more flexible than traditional oil-producing regions.

At the same time, another longer-term factor has been shaping the oil market: a period of relatively low investment in new production.

After the sharp fall in oil prices in 2014, many companies cut exploration budgets and delayed or cancelled projects. The growing focus on environmental, social and governance (ESG) investing also led many investors to reduce their exposure to fossil-fuel companies.

The result was a period of underinvestment across much of the industry. Demand for oil has remained relatively strong, but growth in new supply has been more limited than many analysts expected.

Politics continues to play an important role as well, and Venezuela provides a good example. The country holds the largest proven oil reserves in the world, estimated at around 300 billion barrels. Yet despite this enormous resource, Venezuela produces far less oil than it once did.

Years of political instability, sanctions and underinvestment have severely damaged the country’s oil industry. Much of Venezuela’s oil is extremely heavy crude located in the Orinoco Belt, which makes it more difficult and expensive to extract and refine.

However, following the capture of President Nicolás Maduro earlier this year, Western companies are once again being encouraged to invest in Venezuela’s oil sector.

Taken together, these factors help explain why energy companies have been performing well in recent months, even before the latest tensions in the Middle East pushed oil prices higher.

For more information about Saltydog, or to take the two-month free trial, go to www.saltydoginvestor.com

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.