Investment trusts: crisis? What crisis?

As the door shuts on a golden era for the sector, a Kepler analyst explains that another door has quietly opened.

27th February 2026 14:03

by Alan Ray from Kepler Trust Intelligence

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

One question my colleagues and I used to get asked a lot goes something like this: ‘When will the next investment trust IPO be? and ‘What do you think the next big thing in IPOs will be?’

Superficially, these are fair enough questions. Before interest rates rose, the investment trust sector experienced a decade-long golden era of IPOs and other fundraising. Even investors not tempted to participate in some of these newer investment trusts may have derived comfort from knowing that their own investments were part of a thriving community.

IPOs make for good headlines, and with those headlines now replaced by stories about M&A and corporate activity, it’s very easy to gain the impression that the sector is now in less good health. The phrase ‘existential crisis’ occasionally gets thrown into the mix, making for uncomfortable reading.

First, let me say that the following statement carries 100 nuances and caveats, which space and a need for clarity prevent me setting out here. Many aspects of life and investment are cyclical. Any industry that has seen a decade of rapid expansion shouldn’t be too surprised if this is followed by a pause and some M&A and corporate activity.

Being very close to the investment trust sector, it’s easy to get caught up in the specific injustice of this merger or that EGM requisition. But take a step back, and this all seems like capitalism operating quite normally. And if this really is the sector’s last existential battle, well, that’s a shame for me and a few other people, but really, investment trusts are just a tax-efficient form of investment company with no employees. So, as good capitalists, let’s try not get too emotionally invested.

In any case, behind the headlines, we can’t help noticing that a) many discounts are narrowing and b) many discounts are now not discounts at all. In fact, there are numerous investment trusts issuing new shares steadily. Daily share issuance isn’t a ‘story’, and so it is easy to see why it flies under the radar. And, very recently, specialist bond investor Invesco Bond Income Plus Ord (LSE:BIPS) has executed a larger fundraising transaction, which I look at further below.

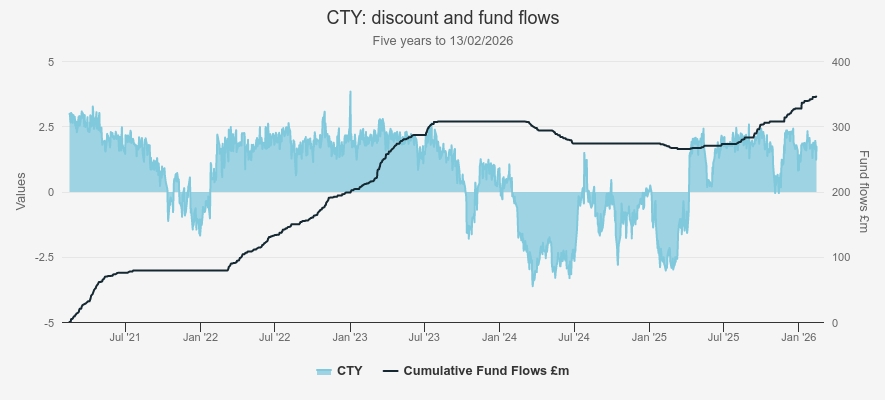

But first, I imagine that City of London Ord (LSE:CTY), if it were a person, wouldn’t mind ditching the baggage that comes with being described as a ‘bellwether’, but there are worse things to be called.

The chart below shows CTY’s discount, or premium, and the cumulative total of shares issued or bought back over the last five years. The discount is the blue shaded area, and the cumulative total of share issuance, measured in £m on the right-hand axis, is the black line. This doesn’t look like an existential crisis to me.

CITY OF LONDON: DISCOUNT AND FUND FLOWS

Source: Morningstar

With a market cap of £3 billion, CTY does, of course, have that all-important ‘scale’ that is one of the sector’s obsessions, so perhaps it’s the exception.

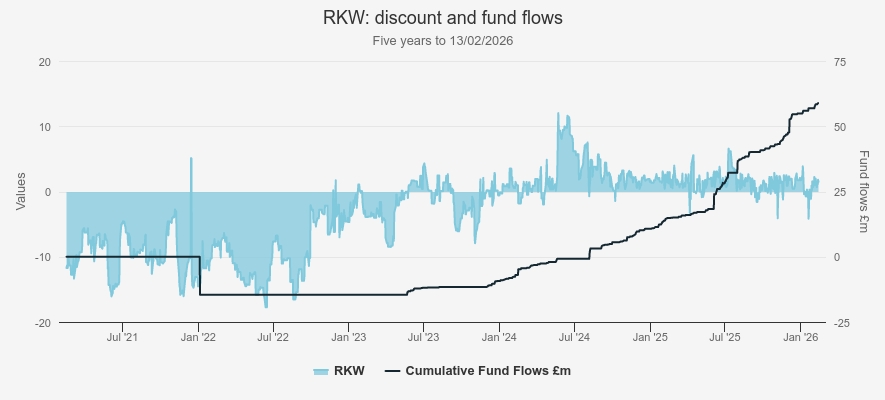

Let’s look at a different example. UK small-cap specialist Rockwood Strategic Ord (LSE:RKW) has defied the scale obsessed to grow from about £50 million to over £200 million through a combination of performance and share issuance, totalling a net £60 million over the last five years. RKW’s own discount and fund flow chart is below, and again, this doesn’t look like an existential crisis so much as an everyday story of a small investment trust winning the hearts, minds and wallets of investors by performing extremely well.

RKW: FUND FLOWS

Source: Morningstar.

As mentioned already, in February BIPS completed a placing and retail offer for shares, raising a total of £25 million, approximately equally split between the placing, for which read ‘professional investors’, and the retail offer. By the standards of the golden era, this is relatively small, but the fact that almost half the money came from retail investors so often prevented from participating in these transactions in the past, is an extremely good sign.

The advantage is that these transactions are often keenly priced, with fewer friction costs than come with buying shares in the normal way. I imagine others will be analysing the result with great interest. And, as we will come on to look at further below, equity strategies with a ‘value’ style bias are returning to popularity. But where are the new value strategies to cover regions like Europe or the US going to come from? Perhaps BIPS provides us with a glimpse of another way to bookbuild for an IPO.

Fellow bond specialist M&G Credit Income Investment Ord (LSE:MGCI) has also quietly been getting on with the job of issuing shares over the last couple of years, with over £50 million of new shares issued since 2024, and TwentyFour Income Ord (LSE:TFIF) has amassed over £300 million of issuance over the last five years. These share issuance programmes may not always directly connect with retail investors, but they help to place limits on the premium to NAV, which, for those buying shares in the normal way in the market, is important. And to be fair to the ‘scale obsessed’, there are cost benefits to scale that can compound over time.

It’s perhaps not that surprising to find that investment trusts focused on bonds have been doing well over the last few years. What’s very encouraging elsewhere is that investors are beginning to pay attention to undervalued UK equities. Last year, investors finally seemed to react to the UK’s low valuations, with the FTSE 100 performing exceptionally well. Fidelity Special Values Ord (LSE:FSV), which invests across the market cap spectrum, had an even more exceptional year, but given its value bias, probably has a lot more to offer investors and recently began to issue shares after its discount transitioned to a premium.

Temple Bar Ord (LSE:TMPL), perhaps even more overtly a ‘value’ investor than FSV, is also in a good place. After a few years of sizeable share buybacks, 2025 saw it get the rewards, with the discount eliminated and a steady stream of share issuance. More internationally, but equally with defensive, value qualities, Murray International Ord (LSE:MYI) has recently moved to a premium. This again follows a long period of steady share buybacks over the last five years, and it’s now in the very early stage of issuing shares. Similarly, Invesco Global Equity Income Trust ord (LSE:IGET) transitioned to a premium over a year ago, and has issued almost £60 million of new shares, driven by strong performance.

But the pattern isn’t limited to undervalued or defensive stocks. CQS Natural Resources G&I Ord (LSE:CYN), which, it’s fair to say, had a difficult 2025 due to the extraordinarily aggressive attentions of activist investor Saba, has dusted itself down and, with strong performance and a share price premium, began to claw back some of the ground it lost in a large return of capital last year. CYN is one of only a handful of investment trusts that give investors specialist access to the resources sector, which plays such an important role across so many other sectors.

Conclusion

It’s easy to see why the end of a ‘golden era’ is accompanied by very negative discussions about an existential crisis. But anyone who has worked on an IPO will likely have found it an incredibly difficult and unpleasant experience. I think there are very few fund managers who would choose to do an IPO a second time, especially if they were given the alternative of steady share issuance. While my normal rule is never to introduce a new concept into the conclusion, rules are there to be broken. So, let’s ask, why do we even care if fund managers can raise new money? All we care about is performance, right? Well, I think we just need to be mindful that to attract talent, the sector needs to be commercially appealing. All of the above examples, which are just a sample, show that, very quietly, the commercial appeal persists. As we slam shut the door on the golden era, another door quietly opens in its place.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.