ISA consolidation could save investors thousands of pounds in fees

interactive investor publishes new calculations as part of its ‘Dare to Compare’ campaign.

9th March 2026 12:04

As the end of the tax year draws closer, new calculations from interactive investor (ii), the UK’s leading flat-fee investment platform, reveal that investors could save thousands of pounds by consolidating their ISAs.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

It comes as interactive investor urges investors to ‘Dare to Compare’ their investment platform fees, to ensure they’re getting the best value for their financial future. interactive investor’s research* revealed:

- Almost one-third of investors (31%) currently have more than three different providers that currently hold their investments and/or pensions, and almost half (47%) have two

- 43% of investors would move platforms for lower fees, yet they might not realise that having multiple ISAs means that they are paying well over the odds.

Camilla Esmund, senior manager at interactive investor, says: “It’s great to see the benefits of consolidating pensions being increasingly discussed in the industry, but the benefits of also consolidating ISAs can often be overlooked. Individuals may have multiple ISAs scattered across different providers, unknowingly paying over the odds and eating into their pots, which should be benefiting from the magic of compounding.”

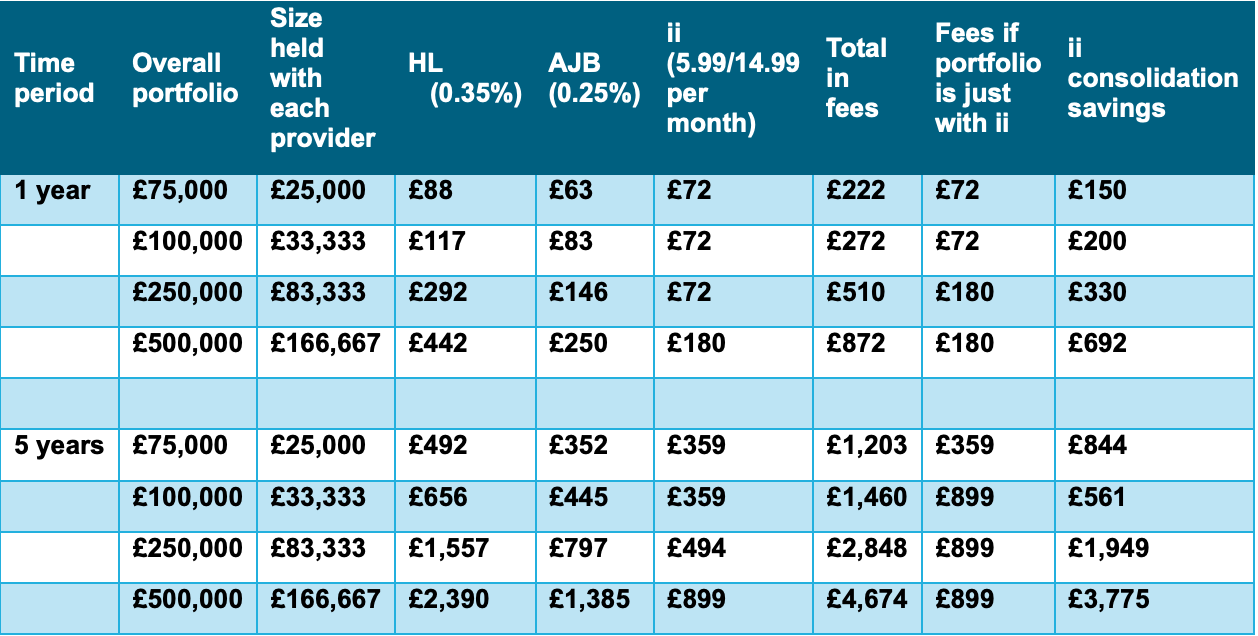

New calculations by interactive investor show that investors with a £75,000 portfolio split between three providers, could save £844 over a five-year period, by consolidating into a single account with interactive investor, which charges a flat fee.

This assumes investment growth of 5% per annum and a £25,000 investment with three providers: Hargreaves Lansdown, AJ Bell, and interactive investor.

Across the same five-year period, savings rise to £1,949 and £3,775 for consolidated portfolios totalling £250,000 and £500,000, respectively. The savings for a consolidated portfolio worth £100,000 is £561.

Source: interactive investor. Assumes investment growth of 5% per annum, with a portfolio split 50/50 between funds and shares. The percentage fees are calculated on a monthly pro rata basis, which includes compounding, and they do not factor in trading costs. The calculations are for illustrative purposes only. Other trading behaviours will result in different charges than those shown. Note, crossing £100k moves you into a higher fee band – interactive investor’s flat fee plans can be found here: ii fees & charges - ii

Camilla Esmund adds: “In addition, managing multiple ISAs across different providers makes tracking your investment performance and contributions more complex than it needs to be. By consolidating all your ISAs with one platform, it makes managing your investments - and building long-term financial resilience - that bit easier.

“You can also consolidate different types of ISAs within one account. For example, you may have a Cash ISA that you’d now prefer to have invested, so this can be moved into your Stocks & Shares ISA. While saving in cash accounts offers security, research shows investing is typically the better option for long-term growth, albeit with more risk. Over the long term, the value of your investments will normally have time to recover from any temporary market dips. A great way to manage risk is to diversify your portfolio with investments in different sectors, markets, and types of assets. At interactive investor, we offer a huge range of educational resources to help investors build diverse portfolios, as well as our new Investment Coach tool.

“For those who prefer a more hands-off approach, ii’s Managed ISA provides expert management of portfolios, giving investors peace of mind without the need for prior investment experience.”

*This survey was conducted by Censuswide, polling 1,000 UK adults who hold investment products including S&S ISAs with a balance of at least £20,000, and aged 18+. It was conducted from 16/01/26-20/01/26.

Important information: Please remember, investment values can go up or down and you could get back less than you invest. If you’re in any doubt about the suitability of a Stocks & Shares ISA, you should seek independent financial advice. The tax treatment of this product depends on your individual circumstances and may change in future. If you are uncertain about the tax treatment of the product you should contact HMRC or seek independent tax advice.

interactive investor (ii) is an Aberdeen company. Aberdeen advise ii on the fund selection for the Managed ISA portfolios. The portfolios contain funds predominately managed by Aberdeen but may also include funds managed by other third-party managers. Please review the portfolio factsheets for more details on the underlying funds. Find out more about how ii and Aberdeen work together.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.