Stockwatch: has this canny short seller made the right call?

This share has already fallen significantly, but trading activity has caught the eye of analyst Edmond Jackson. Here’s what he makes of it.

27th March 2026 11:48

by Edmond Jackson from interactive investor

Recently it caught my attention how a newish operator in the UK equities short-selling space has increased its position. It’s unclear whether this represents a thumbs down on the UK economy, but it has typified mid- and small-cap shares, which are usually domestically focused and sensitive.

- Invest with ii: Open an ISA | Top ISA Funds | Transfer an ISA to ii

I pay attention because London-based Qube Research & Technologies – a hedge fund spun out of Credit Suisse in 2018 – posted a circa 30% gain in 2025, a remarkable achievement given that it has almost $40 billion (£30 billion) under management. Such scale of assets does, however, imply that a hedge fund needs to identify useful shorts to be acting within its mandate.

When weighing up a share’s fundamentals, I like to consider what a shorter might have seen, and whether I can see enough positives to offset that if taking a long-only stance.

On a market technical view, the more active shorters there are in a share, the sharper recovery when it comes to buying back (unless the company is going bust).

For such reasons I find short-selling activity useful rather than something to complain about. They add intrigue and potential extra reward to the investment game, and help us avoid loss when flagging high risk.

But I oppose the Financial Conduct Authority (FCA) acting in shorters’ interests by proposing to remove the requirement to publish individual hedge fund positions, instead revealing only an aggregate percentage of shorts on a particular share. Let us therefore make the most of current disclosure while it lasts.

Too late to short Treatt or are risks still rising?

One aspect why we should not always fear shorters is that they’re sometimes late to the party following a major decline. If factors behind a share’s underperformance are transient or fixable, then shorting sets up a more attractive inflection point when headwinds ease and/or a new CEO delivers improvements.

- How to trade the greatest late-cycle bull market in history

- Sector Screener: two FTSE 100 stocks with long-term appeal

- Four tips for ISA investors to navigate stock market volatility

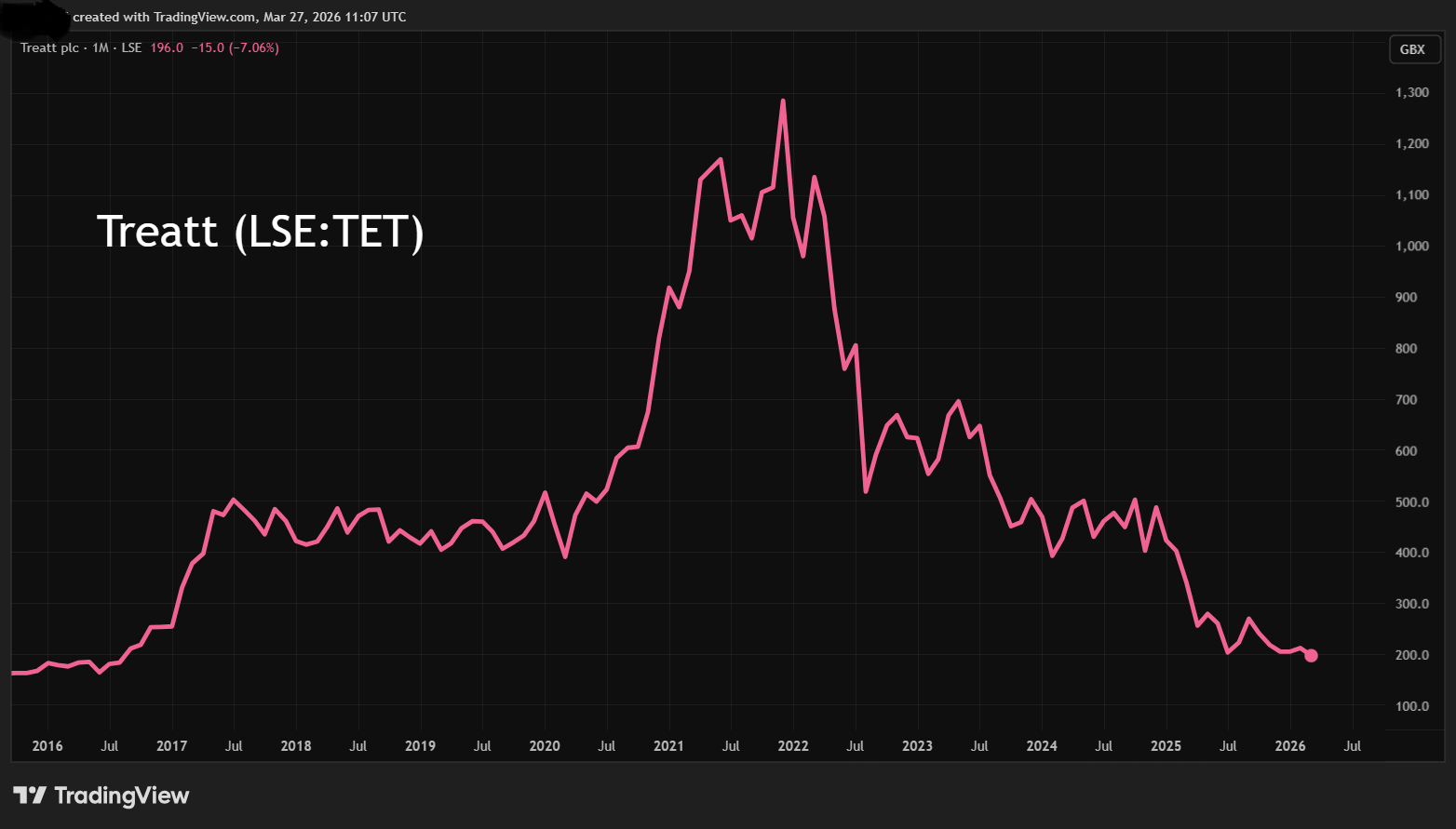

Treatt (LSE:TET) is a small-cap manufacturer of natural extracts for the beverage, flavour and fragrance industries. It originated in 1886 and floated on the stock exchange in 1989. At around 200p a share currently, it is capitalised at only £117 million, implying a niche-type business, possibly more likely to end up being bought and integrated into a larger operation to achieve synergies, rather than prove to be a genuine growth share.

Qube is the only listed shorter, and Treatt must be a peanut trade for them, but having hit the 0.50% disclosure threshold on 21 January, it rose to 0.6% on 5 February. Unless this was below 0.5% for some while, it looks late in the overall context of Treatt’s decline from over 1,200p in late 2021 to a 185p low this week:

Source: TradingView. Past performance is not a guide to future performance.

Instead of exhibiting, say, an overall uptrend, the share price has mean-reverted back down to September 2016, yet last September there was an initially agreed takeover offer at 260p a share from a similar business, Natura Global. That was swiftly thwarted by the accumulation of 28% of Treatt equity by Germany’s Dohler Group – a key Treatt customer and quasi “white knight” in a takeover contest. Dohler was subsequently allowed to appoint a non-executive director to Treatt’s board.

This affirms the business’ worth to a private owner – a key Warren Buffett concept – with industry taking a different view to market traders. At least as of six months ago, they judged that here is a worthwhile business to commit to its equity.

Treatt’s CEO, who backed the takeover, resigned in November after only 41% of shareholders accepted the offer. During his tenure, Treatt had faced trading challenges such as higher citrus prices (relating to 55% of revenue) and weaker US market conditions (at 40%, Treatt’s largest market by far), partly due to tariffs. A weak trading update last July led to the bid also prompting a search for a new leader, with the chief financial officer taking an interim managing director role.

From a short perspective, the company can look as if it doesn’t know what it is doing – confronted by changes that soon look to include higher input costs due to global shipping issues (it’s why shares in Currys (LSE:CURY) plunged 11% yesterday, as an importer from China). Yet sentiment could shift to long positions if a capable new CEO is appointed and takes appropriate action.

- Chart Insights: gold, inflation and interest rate outlook

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

That Treatt borrowed £5.0 million to buy back its shares in its last financial year might ultimately prove value-enhancing, but it doesn’t address what really counts.

In the year to 30 September 2025, revenue fell nearly 12% to £132.5 million, adjusted pre-tax profit by 44% to £10.3 million and the dividend by 33% to 5.6p a share. Treatt’s share price did initially rise 7p to 203p yesterday after the AGM trading update was overall “in-line”. Management said a quiet first quarter was consistent with prior years, although there was talk of being more weighted to the second half than last year, which could be interpreted as a mild profit warning.

At this level, the forward price/earnings (PE) ratio is 15x expected earnings for the September 2026 year, assuming £8.0 million net profit – down on £5.1 million in 2025. Then we should look for a modest recovery to £8.6 million in the year to September 2027, implying a 13.8x PE and a fair price for those earnings.

In due respect, Treatt even managed to keep its dividend growing throughout Covid, and 6.2p a share is consensus for September 2027, maintaining 2.4x expected earnings cover. Since 2023, capital expenditure needs have appeared relaxed, hence relatively stronger free cash flow:

Treatt - financial summary

Year-end 30 Sep

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 88.0 | 101 | 112 | 113 | 109 | 124 | 140 | 147 | 150 | 132 |

| Operating margin (%) | 10.2 | 12.4 | 11.4 | 11.3 | 12.9 | 16.1 | 9.5 | 9.9 | 12.4 | 5.6 |

| Operating profit (£m) | 9.0 | 12.5 | 12.8 | 12.7 | 14.0 | 20.0 | 13.4 | 14.5 | 18.7 | 7.4 |

| Net profit (£m) | 6.2 | 9.6 | 12.2 | 8.8 | 9.8 | 15.1 | 13.3 | 10.9 | 13.9 | 5.1 |

| EPS - reported (p) | 11.7 | 15.9 | 15.9 | 16.5 | 18.1 | 24.9 | 21.8 | 17.9 | 22.7 | 8.4 |

| EPS - normalised (p) | 12.7 | 18.2 | 19.0 | 18.4 | 20.5 | 25.5 | 17.2 | 29.7 | 25.2 | 15.2 |

| Operating cashflow/share (p) | 16.7 | 3.5 | 1.0 | 30.6 | 22.5 | 14.1 | -2.3 | 35.2 | 34.5 | 18.7 |

| Capital expenditure/share (p) | 1.5 | 9.7 | 11.3 | 17.6 | 41.5 | 23.6 | 20.9 | 9.4 | 9.3 | 8.2 |

| Free cashflow/share (p) | 15.2 | -6.2 | -10.3 | 13.0 | -19.0 | -9.5 | -23.2 | 25.8 | 25.2 | 10.5 |

| Dividends per share (p) | 4.4 | 4.8 | 5.1 | 5.5 | 6.0 | 7.5 | 7.9 | 8.0 | 8.4 | 5.6 |

| Covered by earnings (x) | 2.7 | 3.3 | 3.1 | 3.0 | 3.0 | 3.3 | 2.8 | 2.2 | 2.7 | 1.5 |

| Return on total capital (%) | 16.6 | 20.7 | 14.5 | 12.6 | 13.0 | 16.9 | 9.4 | 10.2 | 12.8 | 5.3 |

| Cash (£m) | 6.6 | 4.8 | 32.3 | 37.2 | 7.7 | 7.3 | 2.4 | 0.8 | 1.8 | 1.8 |

| Net debt (£m) | 2.3 | 10.2 | -10.1 | -16.0 | -0.4 | 9.1 | 22.4 | 10.4 | 0.7 | 5.9 |

| Net assets (£m) | 37.2 | 46.5 | 81.6 | 87.1 | 91 | 106 | 134 | 137 | 141 | 135 |

| Net assets per share (p) | 70.6 | 87.9 | 137 | 145 | 151 | 176 | 220 | 225 | 230 | 220 |

Source: historic company REFS and company accounts.

A mixed update on operations

Citrus market headwinds have begun to show initial signs of easing, “although we continue to expect that a full recovery will take some time to come through”. In premium products, challenging market conditions continue to impact consumer demand, particularly in the US.

More positively, there has been encouraging progress in new markets, especially China. A new Shanghai Innovation Centre is fully operational and benefiting from closer collaboration with customers. Double-digit growth is currently being achieved in line with forecast and is expected to continue that way. A distribution partnership in Asia adds further upside.

The question is whether Asia can tip the balance given China slipped to 7% from 8% of revenue last year, where an increase from the Rest of World from 15% to 18% could conceivably involve wider Asia markets. The UK’s proportion remained 5%, hence sales are genuinely international versus most small caps, perhaps reinforcing Treatt’s strategic and synergistic appeal to a trade buyer.

Is a near 12% discount to net tangible assets relevant?

Qube’s down-bet implies belief the short to medium term is liable to worsen, significantly out of management’s control and where cost-cutting can only go so far to help profit. The Germans have blocked a rival takeover, leaving 260p a share a mirage of the past.

The 30 September balance sheet did, however, show £135 million of net assets, with only 1.6% intangibles and no goodwill, implying net tangible assets of 225p a share. True, assets are essentially worth what they can earn, but I believe the share’s 11% discount does provide some longer-term comfort to shareholders. Treatt’s products may be pressured but are not being displaced, say, by new technology; they have stood the test of time.

- How to build a higher-risk ISA portfolio

- Fill your ISA before tax year end: ii experts share fund ideas

A mid-teens PE can therefore be justified if it’s given a fair chance, and longer-term performance can mean-revert upwards.

I therefore think Qube is potentially right from a share trading angle – further near-term revenue/profit risk – but from a fresh money, long-term investment view is welcome to carry on selling the shares down. I think they are being a tad cute given the classic short-selling target would be a business failing rather than being somewhat challenged like Treatt. However, I do agree that a new assertive CEO is required here.

Your approach, and whether to start averaging in, therefore significantly rests on risk appetite. I broadly recognise a long-term “buy” case for Treatt, but feel it would be irresponsible to make it my final view given that I am wary another profit warning is possible. So, I rate the shares a “hold” but definitely a candidate to watch with fresh money.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.