Stockwatch: is this a special situation amid the macro chaos?

News this week plunged this stock to a six-year low, but analyst Edmond Jackson has seen it all before, which is why he likes the odds of a recovery.

31st March 2026 12:05

by Edmond Jackson from interactive investor

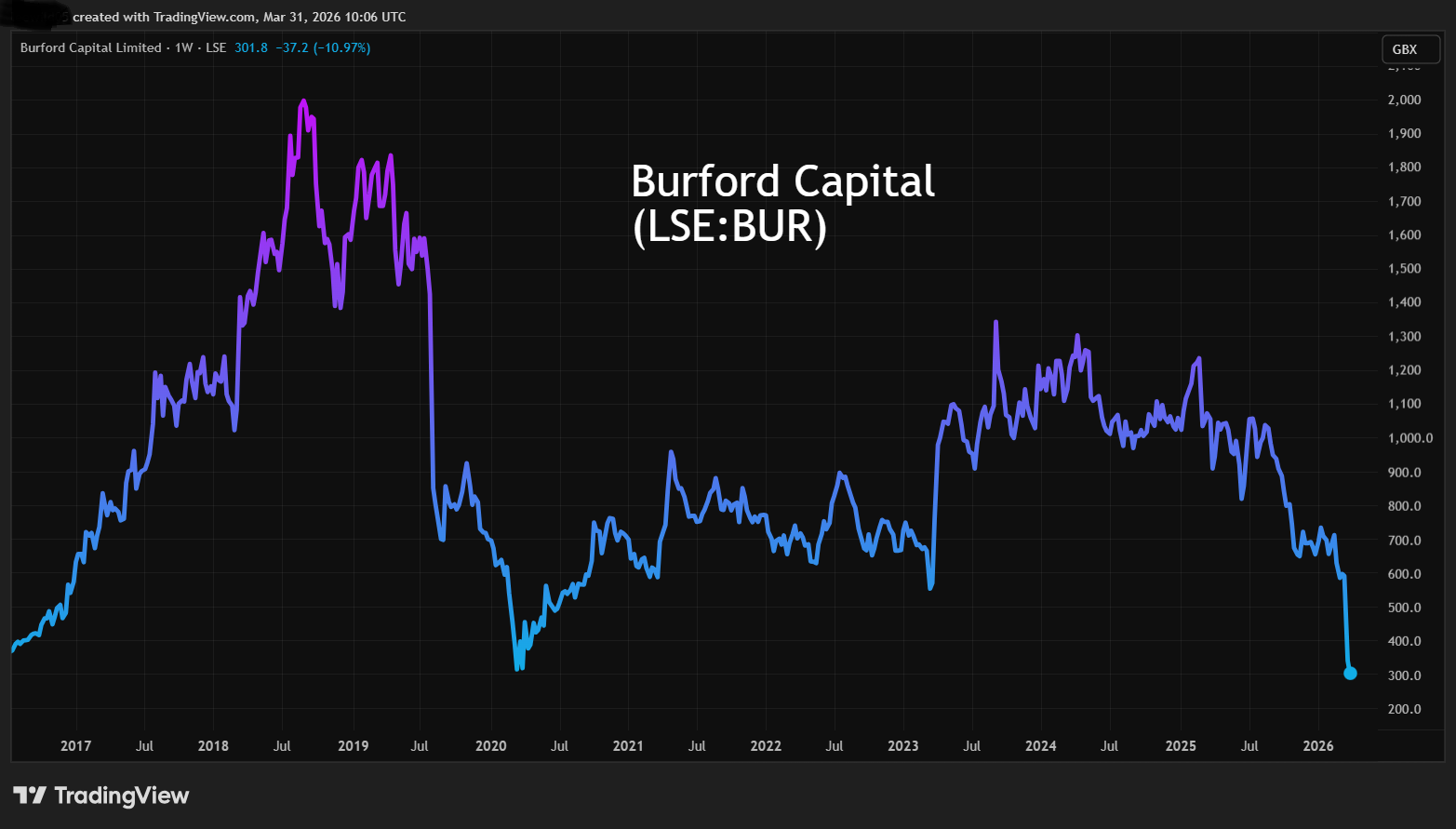

The AIM-listed shares in litigation financier Burford Capital Ltd (LSE:BUR) have seen another slump – this time in response to a surprise ruling by a divided US appeals court last Friday. It struck out a $16.1 billion (£12.2 billion) claim in relation to Argentina’s nationalisation of the YPF SA ADR (NYSE:YPF) oil company, where Burford has a key interest estimated to be worth $1.7 billion.

- Invest with ii: Open an ISA | ISA Investment Ideas | ISA Offers & Cashback

Market price plunged 42% to 340p, extending below 300p briefly yesterday morning before a recovery to 320p at the close, possibly aided by New York buying (there is a dual listing). This capitalises Burford at around £700 million, and the intrigue is whether it might undervalue the portfolio of law-claims shorn of YPF.

What looked very odd was this following a 31 March 2023 ruling by a New York court, effectively declaring a complete win against Argentina. Some already see this as a breakdown of reliability in the US legal system for doing business. There is speculation the twist may reflect the Trump administration’s support for Argentina under radical right-wing President Javier Milei.

Alternatively, it might show how the appeals court system can indeed be robust, and that litigation finance is a highly speculative game where outcomes have been trickier than a decade or so ago. In which scenario, the shares are going to trade at even larger discounts to manager projections as to what the claims are worth.

Yet I doubt litigation finance is likely to diminish as a legal practice, so if stock market sentiment goes against practitioners, might this set up a rebound not dissimilar to how tobacco stocks were shunned then roared higher in the last two years?

A precedent is how Burford shares recovered well from an April 2020 low of 363p, when it was feared that courts would be compromised by Covid. By March 2024, Burford shares had tested 1,300p. I also like Burford’s compensation approach where top people are effectively paid a strong element in equity, although my recollection is that the top man sold enough (years ago) when the market price was high and possibly is now “in for free”.

Source: TradingView. Past performance is not a guide to future performance.

The shares did significantly track Burford’s 2023 financial boom when the company made a $611 million (£463 million) net profit before it slumped to just $63 million in 2025. Consensus anticipates $222 million this year and $257 million next, giving a forward price/earnings (PE) of barely 4x and offering a near 3% yield, with the dividend expected to rise to 12.8 cents from this year.

I would not, however, focus on traditional valuation measures; the crux is whether Burford’s portfolio shorn of the YPF interest has enough prospects. You can read in more detail, for example, a presentation on Burford’s website, via a link from February’s 2025 annual results.

Burford Capital - financial summary

Year-end 31 Dec

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover ($ million) | 82 | 103 | 163 | 343 | 425 | 366 | 328 | 217 | 319 | 1,087 | 546 | 413 |

| Net profit ($m) | 46.6 | 65.7 | 109 | 249 | 318 | 301 | 143 | -28.8 | 30.5 | 611 | 146 | 63 |

| Operating margin (%) | 62.1 | 74.9 | 72.3 | 79.8 | 80.9 | 74.0 | 63.7 | 30.7 | 60.8 | 75.0 | 71.5 | 56.2 |

| Reported earnings per share (cents) | 22.2 | 31.5 | 52.9 | 120 | 151 | 137 | 65.2 | -13.1 | 13.8 | 274 | 65.6 | 27.9 |

| Normalised earnings per share (cents) | 22.2 | 31.5 | 54.8 | 120 | 151 | 142 | 67.2 | -10.9 | 17.4 | 281 | 65.9 | 33.5 |

| Operational cashflow per share (cents) | -45.1 | -9.9 | -3.3 | -49.1 | -111 | -125 | 24.5 | -267 | -210 | -123 | 97.1 | -12.9 |

| Capital expenditure per share (cents) | 0.05 | 0.2 | 0.8 | 0.3 | 0.1 | 1.6 | 0.2 | 0.1 | 0.2 | 1.4 | 0.3 | 0.1 |

| Free cashflow per share (cents) | -45.2 | -10.1 | -4.1 | -49.4 | -111 | -125 | 24.5 | -267 | -210 | -124 | 96.8 | -13.0 |

| Dividend per share (cents) | 7.0 | 8.0 | 9.2 | 11.0 | 12.5 | 4.2 | 12.5 | 12.5 | 12.5 | 12.5 | 12.5 | 12.5 |

| Return on capital employed (%) | 9.8 | 13.6 | 13.5 | 18.2 | 14.8 | 14.9 | 6.4 | 1.8 | 4.5 | 14.0 | 6.3 | 3.5 |

| Cash ($m) | 196 | 217 | 181 | 176 | 343 | 187 | 322 | 180 | 108 | 221 | 470 | 566 |

| Net debt $m) | -58.4 | -86 | 93 | 347 | 408 | 489 | 359 | 854 | 1,159 | 1,314 | 1,294 | 1,561 |

| Net assets ($m) | 383 | 434 | 596 | 799 | 1,363 | 1,533 | 1,763 | 1,696 | 1,743 | 2,291 | 2,419 | 2,448 |

| Net assets per share (cents) | 187 | 212 | 286 | 383 | 623 | 701 | 805 | 774 | 797 | 1,046 | 1,103 | 1,118 |

Source: historic company REFS and company accounts.

Accounting for growth an issue for confidence

When I first drew attention to Burford as a long-term “buy” at 135p in April 2014, the 2013 results had showed a 25% rise in profit and a 20% rise in income. This initially looked encouraging and I went along with it, but by March 2017 I was concerned at the extent of subjectivity in Burford’s accounting for growth.

Management was taking a view on the probability of legal outcomes as if “marking its homework”. Moreover, it reflected in current profit not dissimilar to the way software companies used to be criticised for extrapolating returns. Burford argued that this was more realistic than a cash-based approach where only proven returns are accounted for, leaving big upside unacknowledged when accounting for a period.

- Stockwatch: has this canny short seller made the right call?

- Four tips for ISA investors to navigate stock market volatility

Yet when short seller Muddy Waters targeted the shares in August 2019, it identified further examples of accounting it deemed aggressive, and it was among the key reasons the shares halved from around 1,500p to 750p. In fairness, the shares did recover to 930p by that November but have obviously remained volatile, and sceptics fear that “modelled realisations” up $700 million in 2025 to $5.2 billion at year end may eventually prove overcooked. Burford does also have $2.1 billion debt that generated $151 million interest expenses, and operating expenses rose 17% in 2025 to $181 million.

Dynamics of the income statement on page 42 of the annual results presentation show a total $329 million annual expenses versus $413 million revenue (down 24%), which can feel opaque if one is not wholly sure of the security of such revenue.

But despite cash receipts falling 24% to $530 million – as shown on page 45, I find it hard to dispute this extent of cash conversion.

A discount to net tangible assets and intrinsic value

Page 49 of the annual results shows $2.3 billion tangible book value, which Burford says has always been on an ex-YPF basis, hence it equates to around 1,050 cents per share, or 795p – the shares current price of 295p representing a 63% discount.

Moreover, in an announcement yesterday, the CEO implied book value is not intrinsic value (Warren Buffett would strongly agree, even if I doubt he would invest in Burford given the unpredictability of returns).

He said: “Burford is run on a cash basis, does not rely on cash from the YPF case, which has always been additional to the core business. Our core business is based on a portfolio of many hundreds of valuable cases – we expect to produce more than $5 billion cash proceeds and that has produced over $1.2 billion cash in just the last two years.” It’s planned that some $700 million retained cash will be utilised to double the core portfolio by 2030.

The market implicitly is now sceptical of this, requiring a discount to such projections despite being backed by a relatively recent track record of conversion to cash. You might want to consider if a 60% discount is excessive, as that is the essence of whether Burford is currently oversold.

Wariness follows not just from the YPF shocker, but the 2025 results showing impairments in several cases such as a $22 million unrealised loss in proteins antitrust cases. They came in the context of a fourth-quarter net loss of $50 million, significantly missing forecasts, and 2025 net realised gains down 52% to $158 million.

Executive compensation partly in shares

After the 2025 results, Burford executives used part of their cash compensation to invest over $4.3 million in ordinary shares via a deferred compensation plan. This builds on the CEO and chief investment officer making net purchases of around $35 million, raising their holding in the company to around 8.5%.

It would obviously help near-term sentiment if they also bought in the market, although it would need to be substantial, so watch for this.

- Fund Focus: where to hide in the market sell-off?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

As a long-term follower of Burford, I have seen both the business and shares recover from the onslaught of the August 2019 short attack, which by comparison with the YPF disappointment seemed to me worse existentially. The business also bounced back from Covid, posting strong numbers by 2023. You must remember, this kind of operation will always have a lumpy financial profile.

Regarding debt worries, there are no financial covenants on bond-related debt, which are all unsecured, and maturities stretch out over eight years. However, Burford does “have more debt than the level we previously suggested was ideal”.

Overall, I am tempted enough to rate the shares a “buy” for recovery. However, you need to spend time investigating what is a complex beast with inherent uncertainties. Also mind how disillusion among existing shareholders appears to be prompting stop-loss selling.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.