UK bank sector Q1 results preview: forecasts, targets and top picks

Ahead of quarterly results from the UK’s big banks, City writer Graeme Evans discusses expectations for one of the best-performing sectors over the past month.

21st April 2026 13:45

by Graeme Evans from interactive investor

Branches of HSBC, NatWest and Barclays in Berkshire. Photo by Adrian Dennis/AFP via Getty Images.

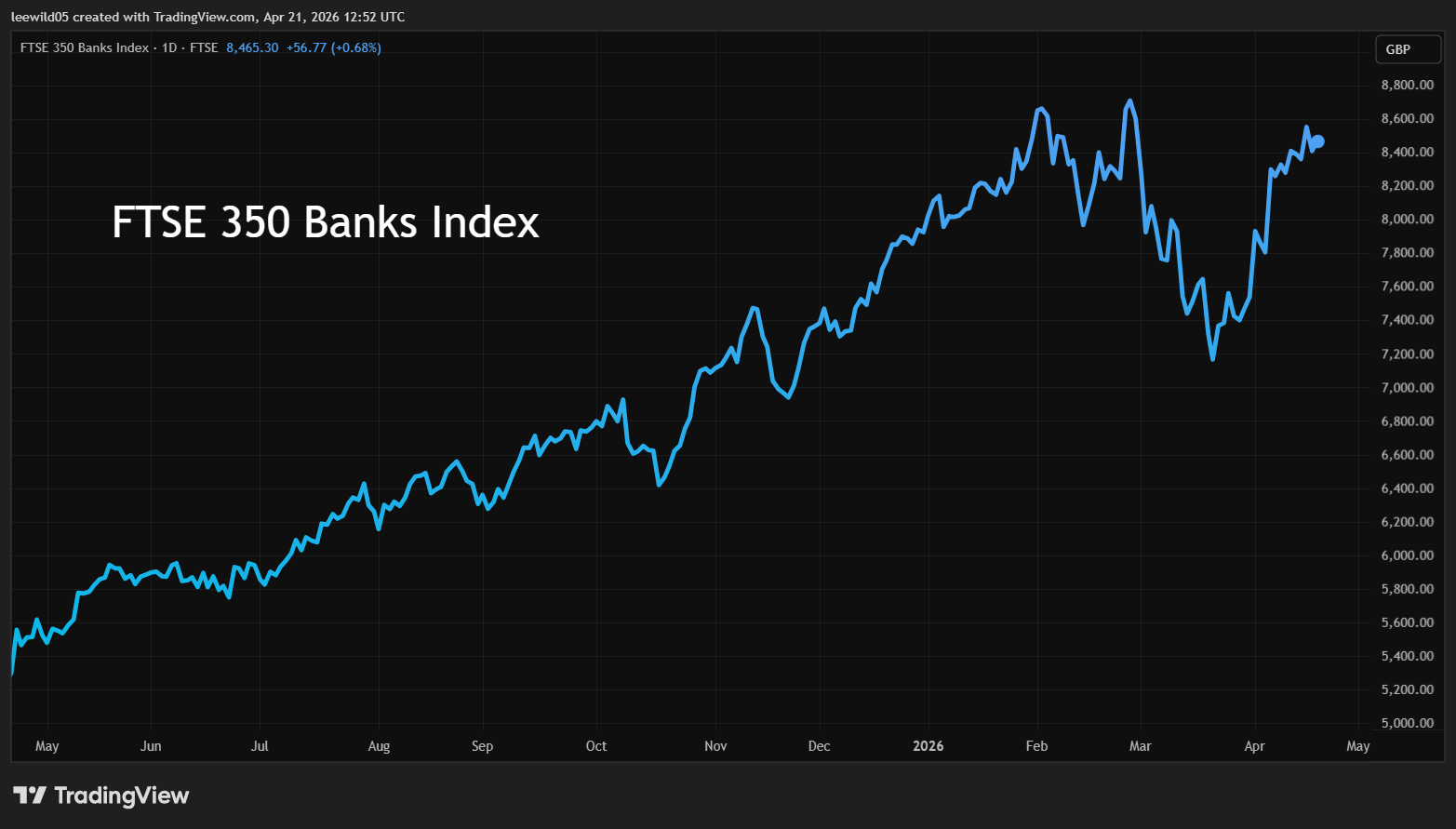

Heavily sold Barclays (LSE:BARC) and 5.6% yielding NatWest Group (LSE:NWG) will be in the spotlight when the UK banking sector delivers robust quarterly earnings at a time of deep economic uncertainty.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Both stocks are about 7% below where they started the year, having suffered peak-to-trough declines of 25% between February and the FTSE 100’s post-war low point on 20 March.

Clarity on motor finance redress means Lloyds Banking Group (LSE:LLOY) is back in positive territory for the year, while HSBC Holdings (LSE:HSBA) is up by 14% year-to-date and not far from February’s record level.

Middle East peace hopes have lifted the quartet by between 13% and 19% since 20 March, although UBS points out that the UK domestic banks still trade at a 39% discount to the FTSE 100 and at a multiple 50% lower than some US peers.

That’s despite an outlook for compound annual earnings growth of 18% in the period to 2028, as well as 2026 forecast dividend yields ranging from 5.6% for NatWest to more than 4% for Lloyds and 3.4% for Barclays.

Source: TradingView. Past performance is not a guide to future performance.

UBS remains Overweight on the UK sector, with Barclays among its top picks based on a current multiple of 6.8 times 2027 earnings and NatWest another of its most preferred stocks.

Barclays kicks off the industry’s results season on Tuesday 28 April, before Lloyds the following day and NatWest on 1 May. HSBC is on 5 May and Asia-focused Standard Chartered (LSE:STAN) on 30 April.

- Stockwatch: are stock market highs really justified?

- Sector Screener: should you buy easyJet and IHG shares now?

- AB Foods confirms Primark split

UBS expects the results will be “defensive but not decisive” as banks struggle to dispel worries that the robust margins, loan demand and credit quality of the first quarter won’t last.

It added: “We expect the upcoming results season to show UK banks as highly profitable, with lenders reconfirming 2026 targets but failing to deliver decisive reassurance in an uncertain operating environment.”

Whilst past returns are no guarantee of future performance, the bank noted that UK players outperformed the wider sector on the trading day following the Iran ceasefire agreement. This includes gains of 8% for Lloyds and Barclays, compared with an average 5.3%.

It said UK domestic banks screened favourably as they’re generally cheaper, growing faster and positively pre-disposed to benefit from modestly higher rates than European counterparts.

UBS sees 31% further share price upside on last week’s level for Barclays to 580p, with NatWest forecast to move 24% higher at 780p as the bank looks to recover after a negative reaction to February’s £2.7 billion acquisition of Evelyn Partners.

Standard Chartered is backed by UBS to move 19% higher at 2,090p, while the bank has a Neutral recommendation on the shares of Lloyds and HSBC.

The positive stance on domestic lenders comes despite material hits to GDP and inflation forecasts due to the energy supply shock and the risk of a further blow to sentiment from next month’s local elections.

Unless stagflation proves to be much worse than the market is currently expecting, the bank said robust levels of credit growth and quality, capital markets strength and margin tailwinds were positive factors in the discussion around UK banks.

- eyeQ: FTSE 100 laggard triggers bullish signal

- 10 hottest ISA shares, funds and trusts

- AGM alert: Lloyds Bank, Unilever, ITV

The use of structural hedges to smooth out interest rate volatility has already provided a significant income boost, although with average hedge durations of three to 3.5 years it will take time for the impact of the recent rise in industry swap rates to be realised.

UBS said: “That’s why we think investors will seek confidence that deposit and mortgage spreads have held up in March and April so as not to offset an improved hedge income outlook.”

Lenders have already warned there will be some pressure from the churn of Covid-era mortgages, which were written at particularly high margins.

This is likely to be offset by mortgage volumes being pulled forward as more customers seek to remortgage in anticipation of much higher interest rates.

Bank of America expects policymakers at the Bank of England will increase their base rate by 0.5% to 4.25% this year, which compares with two rate cuts seen in February.

While unhelpful to the economy, it said this would still be some way below peak rates of 5.25% a couple of years ago and could be followed by three rate cuts in 2027 once inflation peaks.

The bank expects impairment provisions to increase in the forthcoming results but with no noticeable deterioration in actual credit quality in the first quarter.

In the current environment, BofA said its preference was for national champions with a strong deposit franchise.

It said: “Both Lloyds and NatWest are well placed but we prefer NatWest given the valuation and year-to-date performance, in part reflecting a negative reaction to the Evelyn Partners acquisition, which feels overdone to us.”

The bank has a price target of 770p on NatWest shares, which compares with a more cautious stance on Lloyds based on an estimate of 117p.

It points out that longer-term guidance from Lloyds is likely to be light in forthcoming results as management is due to deliver a strategic update with half-year results on 30 July.

- eyeQ: easyJet, BP, Reckitt Benckiser, BlackRock

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- ii Top 50 Fund Index: most-bought funds, trusts and ETFs in Q1 2026

Barclays shares have come under pressure after the Middle East conflict cast some doubt over a three-year plan to return at least £15 billion via dividends and buybacks.

The group’s investment banking division is expected to benefit from high market volatility in the most recent quarter, although comparatives from 2025 are likely to be tough.

BofA has a price target of 570p and is also positive on the shares of HSBC, despite the bank’s exposure to Middle East conflict through operations in the United Arab Emirates.

It highlights further signs of Hong Kong commercial real estate recovery, as well as the net interest income benefit from higher interest rates.

BofA, which has a price target of 1,500p, said: “All the indicators continue to point to Hong Kong’s solid position as a wealth centre - which could be enhanced further given its safe-haven status.

“Both HSBC and Standard Chartered should be well placed to capture the benefits. However, both banks also have direct exposures to the Middle East, mostly in the UAE, although the bulk of the exposure is to high-quality, investment grade conglomerates.”

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.