Stockwatch: are stock market highs really justified?

As investors chase domestic shares higher and Wall Street reaches new highs, analyst Edmond Jackson explores the rationale for bulls and revisits some recent share tips.

21st April 2026 12:23

by Edmond Jackson from interactive investor

Market indices in the US - the S&P 500 and Nasdaq – and Japan’s Nikkei 225 rose to all-time highs last week, swallowing verbatim an Iranian proclamation that the Strait of Hormuz had reopened, only for that to be retracted.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

They have cooled slightly as Iran and the US resume their war of words amid a fragile ceasefire, and with the status of peace talks unknown. Yet oil is relatively settled at around $91 a barrel for Brent crude, where you might assume traders would have turned edgier. Oil seems to highlight an essential assumption in markets about how, despite the two sides trading mutual threats, both have plenty of incentive to end this conflict.

Yet Iran is in a strong position having finally realised, after decades, just what power it wields over the rest of the world, with its geographic control of the Strait of Hormuz. Western markets tend to apply a rationalist mindset to war-game the likely scenario, albeit potentially ignorant of what drives a fundamentalist regime and army. Iran is well-positioned to play a longer conflict than President Donald Trump, who needs it to be over as soon as possible in the run-up to mid-term elections.

While an ideal scenario all round would be Iran stepping back from uranium enrichment, and the removal of sanctions leading to lower energy prices, it is hard to envisage this currently. The next few weeks look significant in terms of whether fuel prices rise further and shortages start to appear, and, in due course, to what extent food prices increase.

Meanwhile, the S&P UK consumer sentiment index has fallen to its lowest level since July 2023, and the Item Club of economic forecasters suggests the UK is poised to “flirt” with recession - as defined by two consecutive quarters of falling gross domestic product (GDP). The GDP downgrade for 2026 is from 1.4% to 0.7% due to higher energy prices and a squeeze on consumers, which is liable to deter companies from investing. Unemployment is expected to rise from 5.2% to 5.8% by mid-2027.

- Sector Screener: should you buy easyJet and IHG shares now?

- eyeQ: FTSE 100 laggard triggers bullish signal

I take such predictions warily, recalling how in 1990 there was a firm consensus among economists for a “soft landing”, yet both the UK and US experienced recession from July 1990 to March 1991. The difference back then was other factors conflating – high interest rates and a property bubble bursting – with higher oil prices surrounding the Iraq invasion early in 1991. But I would take care regarding how much economic modelling – including company forecasts – involves extrapolation, which is liable to get compromised by radical change at the macro level.

Premature to consider recruiters after a five-year bear market?

UK employment prospects might suggest any interest in recruitment stocks is indeed premature. However, the UK is performing relatively worse in a global context. And international recruiters intrigue me given their shares have fallen a long way, and experience suggests they will begin to rally well before any upturn is established. But does that make them a sensible speculation now?

Mid-cap Hays (LSE:HAS) and small-cap Robert Walters (LSE:RWA) have seen their shares rise slightly after updates which affirmed tough conditions, but no way do charts affirm a bottom.

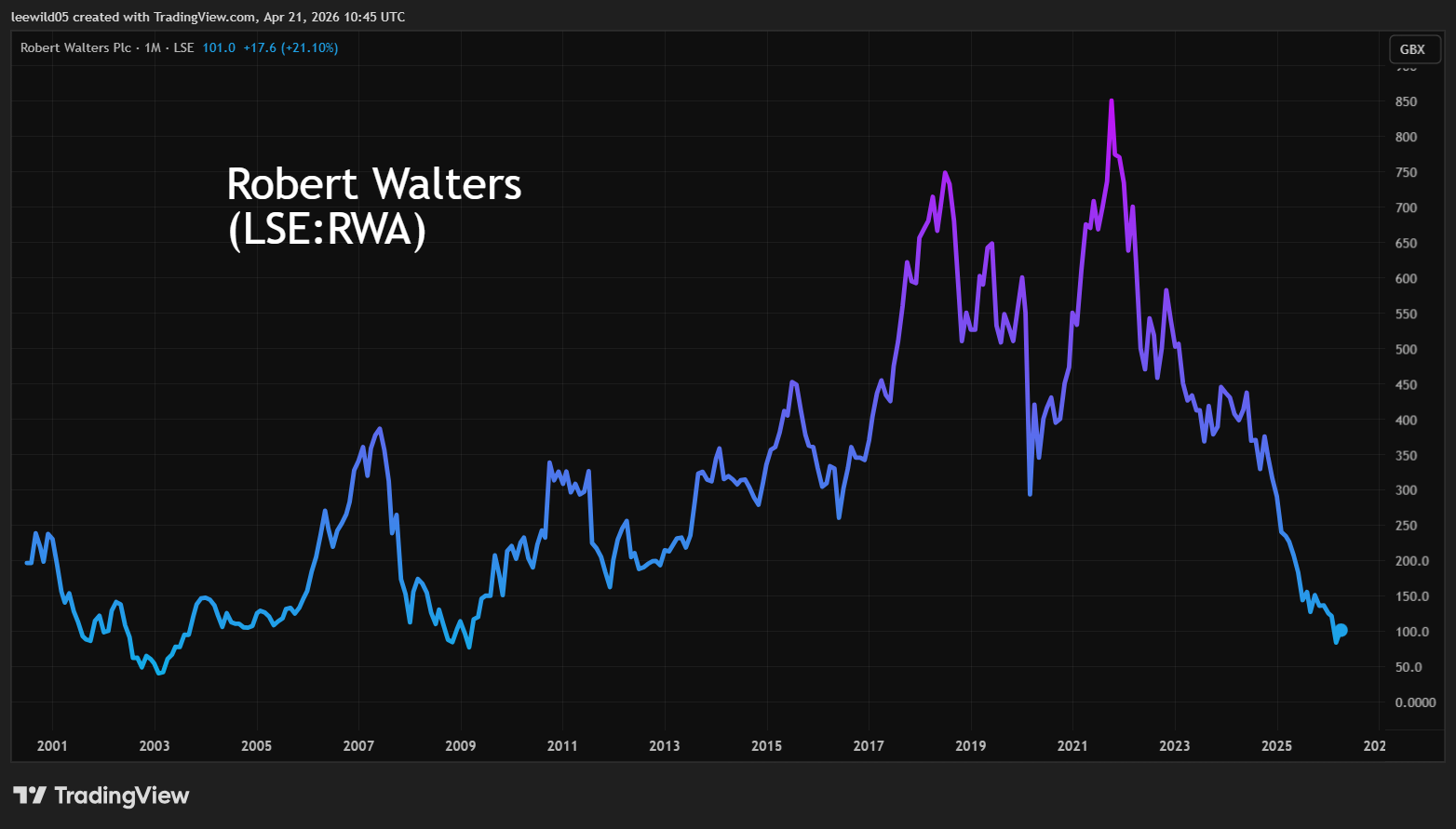

Walters has fallen to lows seen around the 2008 crisis:

Source: TradingView. Past performance is not a guide to future performance.

Walters’ first-quarter 2026 trading update showed a slowing in the rate of decline in net fees to only 2% versus 14% in the second half of 2025.

You could say it’s an early indicator of better times ahead, especially with Europe the only chief source of weakness. The company fell into net losses from 2024, although consensus anticipates a near £21 million loss this year will reduce below £4 million in 2027.

Yet I recall from a one-to-one session with founder Robert Walters many years ago, when he implored the lack of visibility, hence such numbers are guesstimates.

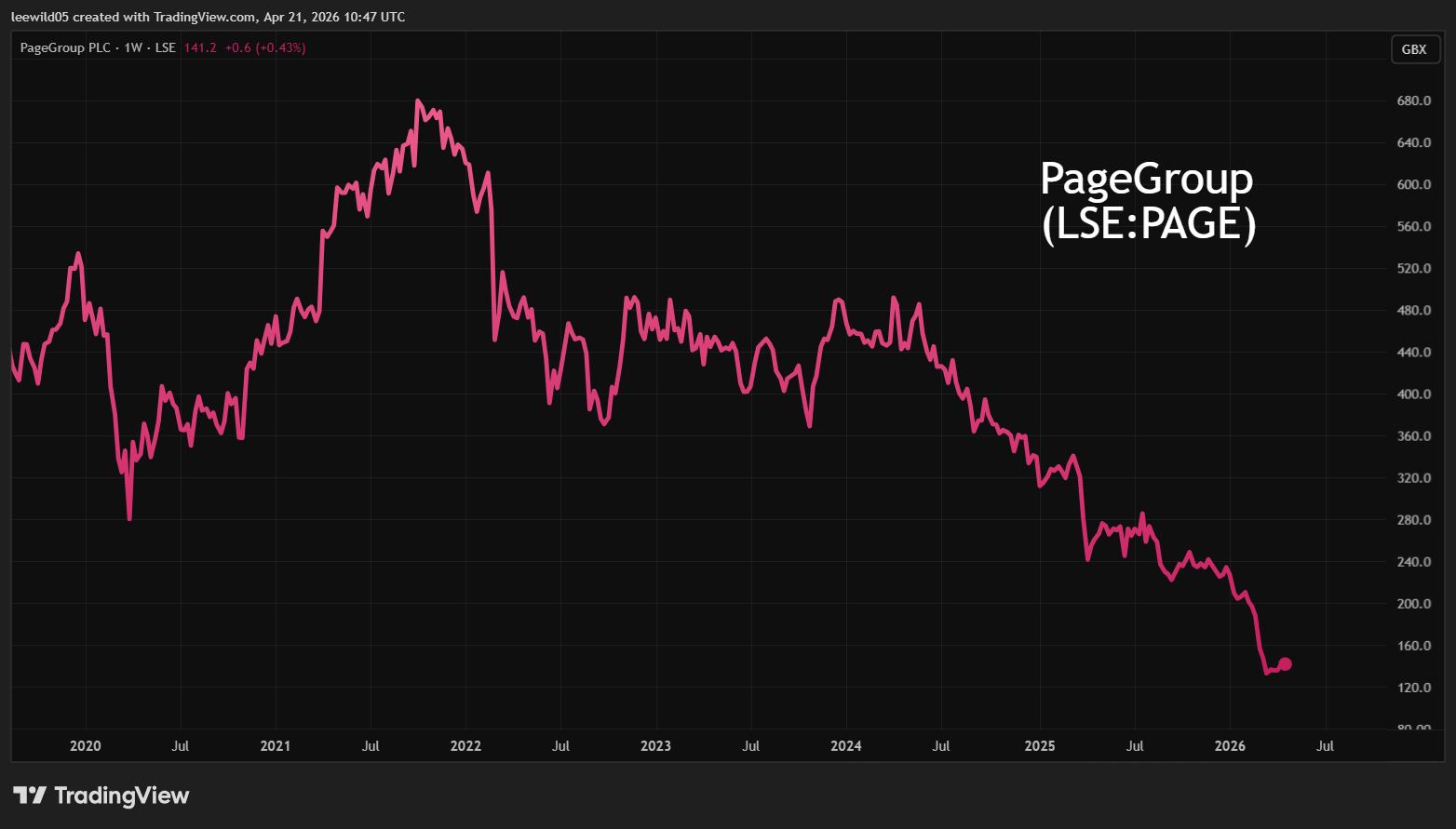

PageGroup (LSE:PAGE) fell 7% to 124p a week ago in response to its first-quarter update, when management were frank about how the Middle East conflict is contributing to greater uncertainty for the rest of the year, with bright spots in the US and Asia being offset by lower client/candidate confidence in Europe.

Shares have recovered to 137p on an 18x forward price/earnings (PE) ratio, with a 6.3% yield albeit expected to be uncovered by earnings this year.

Source: TradingView. Past performance is not a guide to future performance.

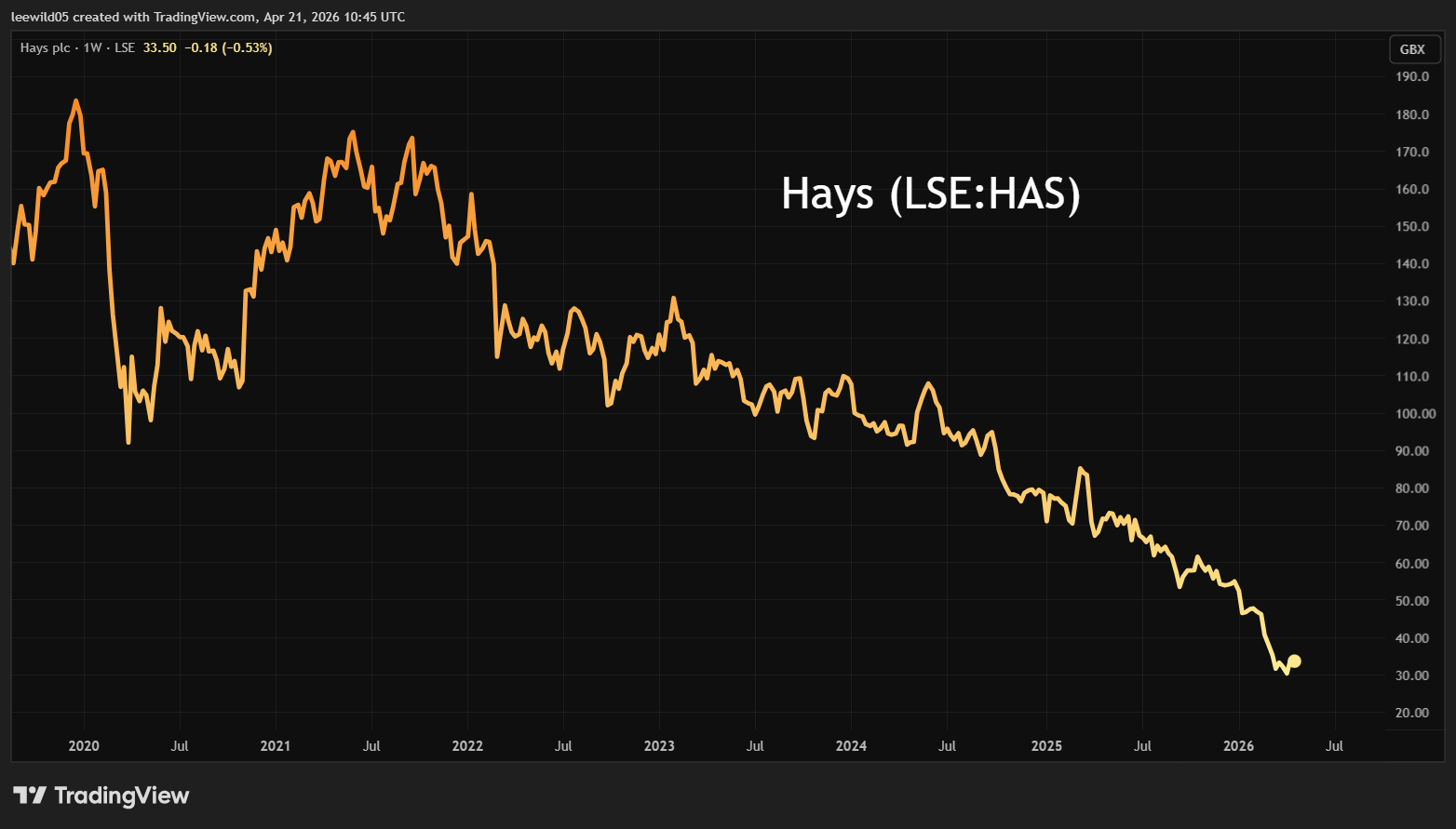

The same period for Hays saw net fee income down 8% overall on a like-for-like basis, with Germany and the UK worst-affected, down 11% and 10% respectively versus Australia and New Zealand 2% easier.

The outlook statement as of 16 April was tricky to decipher. There was a sense of Hays’ PR function working hard to emphasise “strong consultant productivity growth...a substantial bid pipeline...decisive actions to improve and restore our financial performance...strong progress with our structural cost and productivity initiatives...expect the full financial benefits to build over time”.

- ii view: Hays shares stuck near record low after latest results

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

But it remains significantly hostage to whichever way the global economy tilts as a result of the Middle East conflict. Proverbially, it is “well placed for the upturn when it comes”.

The chart is similarly bearish, yet to genuinely indicate a bottom:

Source: TradingView. Past performance is not a guide to future performance.

Hays experienced losses from 2024, but £19 million net profit is the consensus for 2026 and £32 million in 2027. That gives a 12-month forward PE around 18x, albeit a PEG (PE-to-growth) of 0.3 if forecasts are fair. Hays does sport a 2.5% yield, with allegedly over twice earnings cover versus no 2026 dividend prospect for Walters.

Recruiters are particularly sensitive in the current situation yet, intriguingly, are testing all-time lows while the wider market is back near all-time highs. “Buy the drop” exuberance has yet to manifest in the sector. At least it shows the market is rational to an extent that numbers are prevailing over hope.

- Shares for the future: nothing dull about this FTSE 100 stock

- ISA investing: nine ii experts reveal their ISA tips for 2026-27

Such shares should rally on Middle East conflict resolution, although if talks get bogged down then I would tend to see first if lows can consolidate. What rating to apply to recruitment stocks is binary and, according to unpredictable events, I am forced to compromise with a “hold” rating.

Has propeller come off renewables trusts?

On 10 March, I explained how both the Renewables Infrastructure Grp (LSE:TRIG) and Greencoat UK Wind (LSE:UKW) stood a decent chance of inflection points at current depressed share price levels of 67p and 96p respectively.

Soaring oil & gas prices, if sustained, will raise electricity prices, thus potentially transforming net asset values (NAV based on cash flow projections). For UKW, a 10% gain in electricity prices would boost NAV by around 14.5% and vice-versa.

TRIG initially edged up but is currently around 66p, while UKW advanced to 107p only to fall back to 97p, especially on 17 April after the government expressed the intent to remove a carbon price support element within a tax on fossil fuels for electricity generation. This is liable to reduce electricity prices from April 2028 to the early 2030s and by a lesser amount thereafter. UKW estimates NAV will reduce by 3-5p per share, which was instantly priced in, but the shares have fallen another 2p in the current market.

The plunge in energy prices at the end of last week surprised me, as my base-case scenario is the Strait of Hormuz taking longer to resolve – if at all - than markets expect. I therefore retain “buy” stances on such renewable trusts as a hedge for a scenario where electricity prices do grind higher to at least offset this tax setback.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.