2026 investment outlook

Our experts analyse the major talking points for investors and share their investment ideas for the future.

These articles are provided for information purposes only. The content is not intended to be a personal recommendation. The value of your investments, and the income derived from them, may go down as well as up. If in doubt, please seek advice from a qualified investment adviser.

The year ahead: bubbles, politics and economics

After three years of significant gains, the big question is whether major global stock markets can make it four in a row. Among the talking points will be the AI bubble and its possible consequences. Elevated valuations, especially among high-flying technology companies, have so far been justified by strong quarterly results.

Will that continue? Interest rates are expected to move lower through 2026, providing a boost to share prices, but any disruption to the downward trend will not be well received.

There’ll be a big focus on politics too. It’ll be all eyes on the US midterm elections in November when voters could trigger a shift in political control. We might also see an end to the war in Ukraine.

However, with tensions in Russia, China, the Middle East and elsewhere very much alive, gold could break more records in 2026.

2026 outlook

The big question for 2026: has AI caused a stock market bubble?

Ceri Jones

Bond Boss: the outlook for fixed income in 2026

Jonathan Mondillo

Stockwatch: an outlook for sectors and stocks in 2026

Edmond Jackson

The Income Investor: outlook for cash and dividends in 2026

Robert Stephens

Key tax changes impacting investors in 2026

Craig Rickman

Interest rates, inflation and the economy in 2026

Victoria Scholar

China stock market outlook 2026: problems at home

Rodney Hobson

Japan stock market outlook 2026: future looks bright

Rodney Hobson

India stock market outlook 2026: a worthwhile consideration

Rodney Hobson

Europe stock market outlook 2026: a great place for UK investors

Rodney Hobson

The UK stock market outlook for 2026

Graeme Evans

US stock market outlook 2026: about to get even more interesting

Rodney Hobson

IPO market outlook for UK in 2026

Graeme Evans

The tariff playbook: why I’m sticking with UK markets in 2026

John Ficenec

Five macro themes tipped to shape markets in 2026

Graeme Evans

2026 look ahead: CHAOS or CALM?

Richard Hunter

Outlook for 2026: why more records could be broken

Graeme Evans

Our expert's tips for 2026

My favourite US share for 2026

Keith Bowman

Kyle Caldwell’s investment trust ideas for 2026

Kyle Caldwell

Two UK funds I’d own in 2026

Dave Baxter

A FTSE 100 stock to watch in 2026

Lee Wild

Stock, fund and trust tips for 2026

10 shares to give you a £10,000 annual income in 2026

Lee Wild

20 top small-cap share tips for 2026

Graeme Evans

5%-plus yields: fund and investment trust ideas in 2026

Cherry Reynard

20 value-focused top share picks for 2026

Graeme Evans

21 top growth stocks for 2026

Graeme Evans

Fund manager predictions for emerging markets in 2026

David Prosser

The shares attracting fund managers at start of 2026

Beth Brearley

Experts name fund and trust opportunities at start of 2026

Jennifer Hill

Trading Strategies tip 2026: a FTSE 100 cyclical play

Robert Stephens

Five AIM share tips for 2026

Andrew Hore

Stockwatch: what I think could go right and wrong in 2026

Edmond Jackson

Stockwatch: is value investing the best strategy in 2026?

Edmond Jackson

Share tip review of 2025 and what I’d do with them now

Rodney Hobson

Funds to navigate a big risk heading into 2026

Morningstar

Shares for the future: what 2026 might hold for this top 5 stock

Richard Beddard

Will banks continue their strong run in 2026?

Graeme Evans

Will these airlines take off in 2026?

Graeme Evans

ARK Invest’s Cathie Wood on performance, Nvidia and China

Dave Baxter

Retail top picks for 2026 revealed

Graeme Evans

Five top share trades for 2026

Graeme Evans

Insider interviews

How we navigate the UK market’s dividend danger

Kyle Caldwell

Why we’ve boosted our dividend to yield above 6%

Kyle Caldwell

The special shares we have owned for over a decade

Kyle Caldwell

Reasons to be bearish and bullish in 2026

the interactive investor team

We’re cautious about AI, but these are the shares we’re backing

Kyle Caldwell

Why a crisis is brewing in US markets

Dave Baxter

Bargain shares on offer in the UK and beyond

Dave Baxter

ARK Invest’s Cathie Wood on performance, Nvidia and China

Dave Baxter

Why this risk will become a bigger headache for markets in 2026

Kyle Caldwell

The big trends shaking up investment trusts

the interactive investor team

We still like gold, but here’s why we’ve halved exposure

Kyle Caldwell

ARK Invest’s Cathie Wood: why we’re betting big on Tesla

Dave Baxter

City of London: the UK shares still offering value

Dave Baxter

City of London: the stocks powering our dividend growth

Dave Baxter

Latest market news straight to your inbox

Keep your finger on the pulse with impartial, expert content from our award-winning investment journalists.

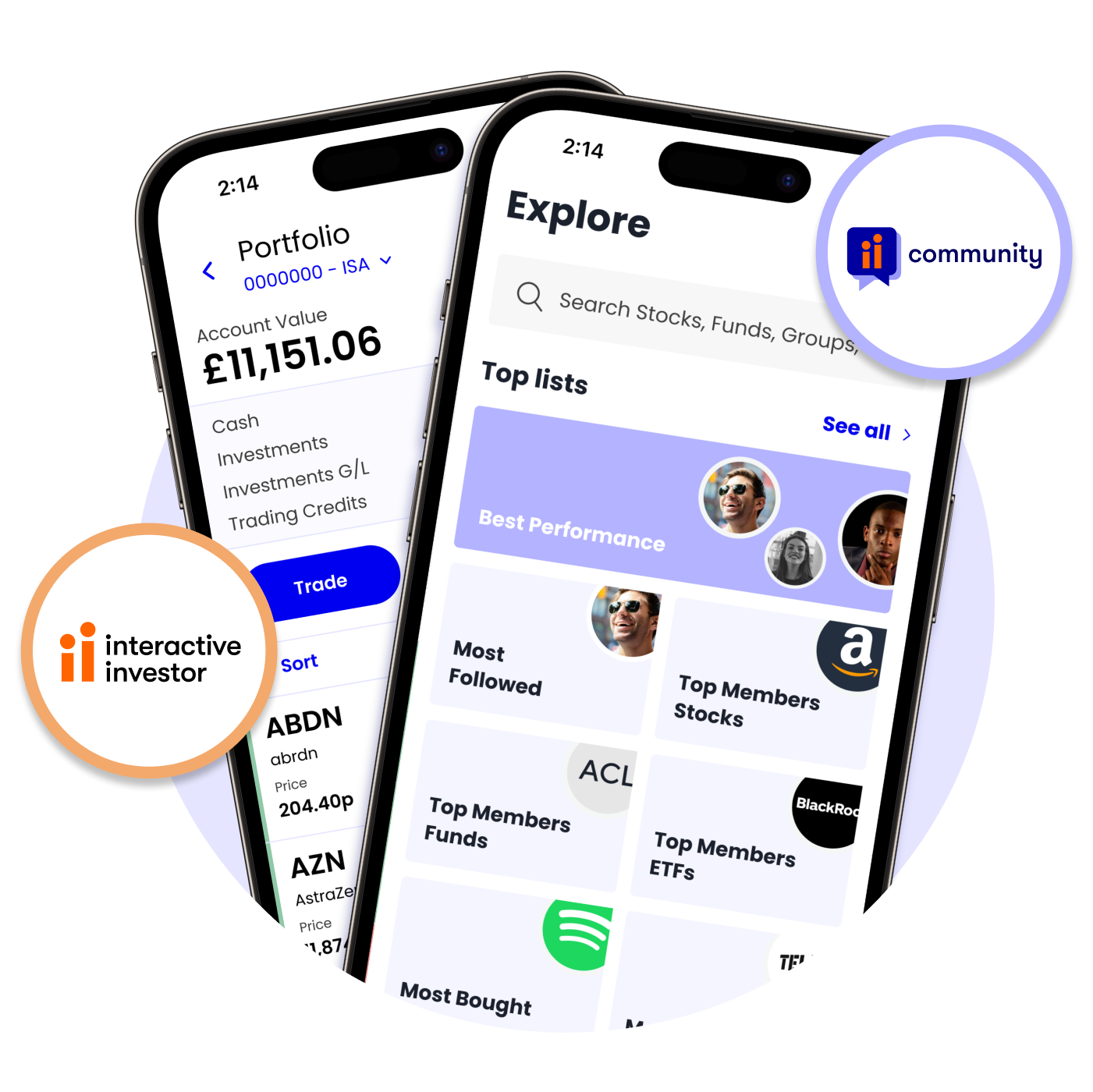

Free and exclusive access to ii Community

Join ii Community - the free social trading network built for ii customers.

Connect, compare portfolios, and talk strategy with like-minded investors. Whether you’re after expert insights from our award-winning journalists or want to swap ideas in private groups, this is your space to stay sharp, informed, and inspired.