What happens to a Junior ISA at age 18?

Learn what happens when a Junior ISA matures and the options your child has when that time comes. And when you’re ready, start investing in your child’s future.

Important information: The value of any investment can go down as well as up and your child might not get back what was originally invested. The tax treatment of a Junior ISA depends on individual circumstances and tax rules may change. Please be aware that grandparents do not automatically have parental responsibility. If you’re unsure about the suitability of a Junior ISA or any investment please speak to a suitably qualified financial adviser.

What you’ll learn in this guide

- What the process of JISA maturity looks like

- Steps your child can take with their JISA when it matures

- Ways your child can start contributing to their ISA

- How your child can access their money and manage their account

What happens when a Junior ISA matures?

When a child turns 18, their Junior ISA (JISA) automatically matures into an adult ISA.

Once the JISA matures, the child gains full control of the account, and parental/guardian access will end. However, if they’re unable to manage their finances independently, support can continue if the proper legal arrangements are in place.

JISA maturity steps at ii

In the weeks before maturity, the parent will be notified and the child will be asked to fill in a maturity form. This needs to be printed, signed and posted to 4th Floor, 3 South Brook Street, Leeds LS10 1FT.

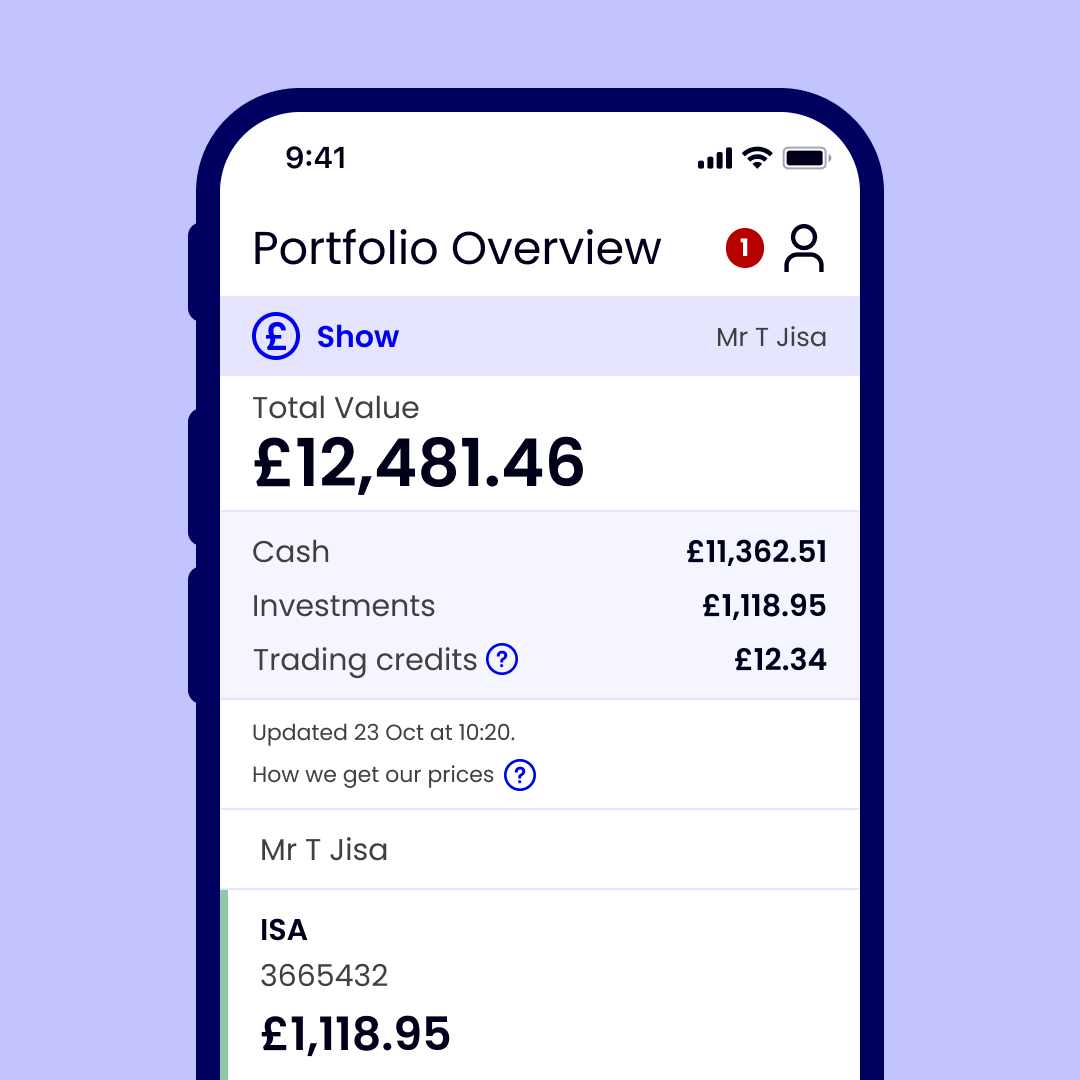

On the date the child turns 18, the JISA turns into a Stocks & Shares ISA. The child becomes the account holder and the parent can no longer access the account.

Once the child's ID and maturity forms have been verified, the child will get their login details and full access to their new ISA account.

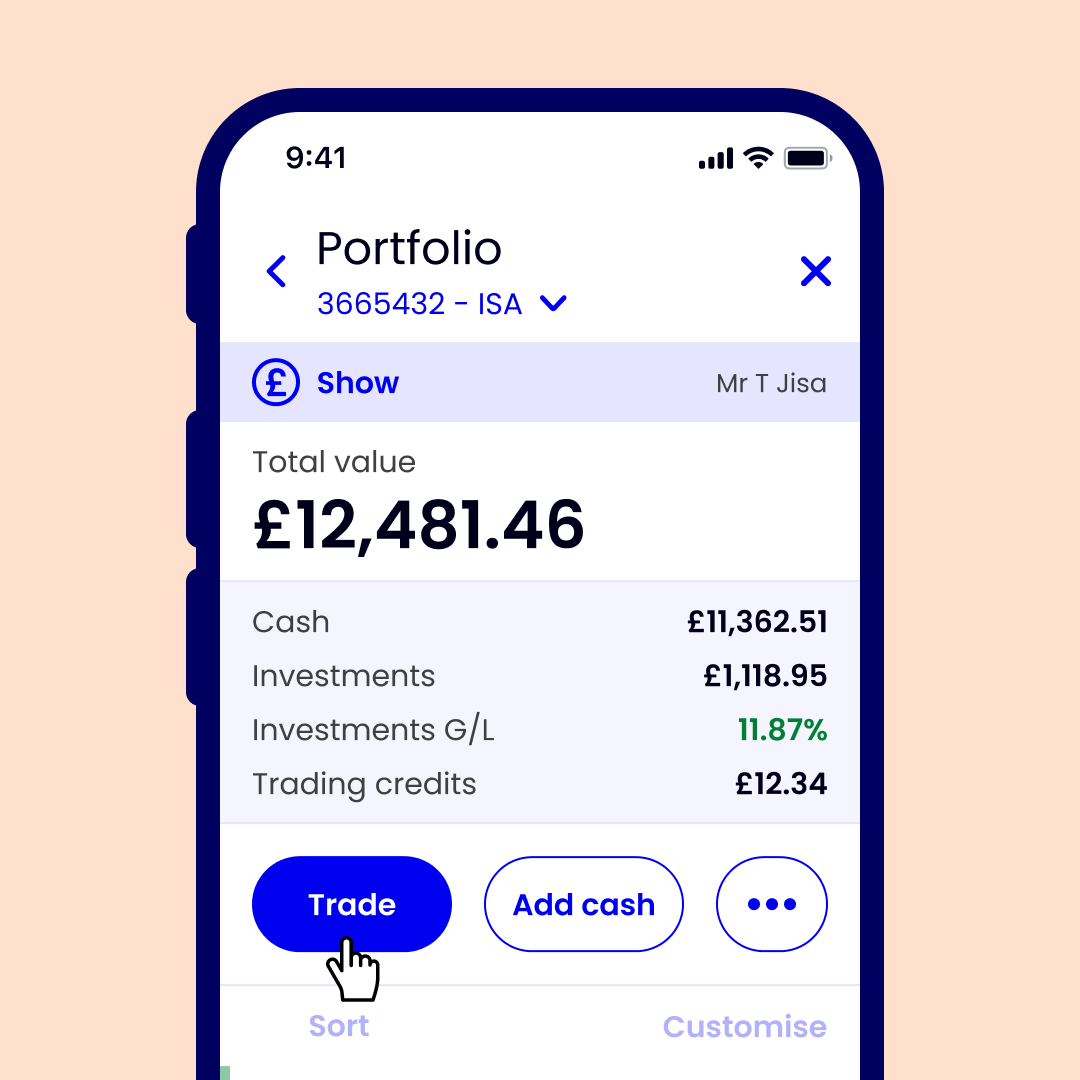

And if they want to carry on investing their money without investing their time they can add a Managed ISA at no extra cost.

Simple charges for your child's ISA

Unlike percentage-based fees charged by many ISA providers, with ii your child will always pay a low, flat fee. This can add up to real cost savings as their wealth grows.

They will start on our Core plan at £5.99 a month and can upgrade when they want access to a wider range of benefits - or when their portfolio grows above £100,000.

It’s a transparent, cost-effective way for them to invest tax-efficiently for their future.

Get started from £5.99 a month

- Self-managed ISA and Managed ISA available on all plans

- Add a Personal Pension and Trading Account at no extra cost

- Free regular investing

- Buy and sell investments from £3.99 per trade

How your child can start adding money to their ISA

Making contributions to an ISA at ii is easy and there are several ways your child can start adding to their ISA themself.

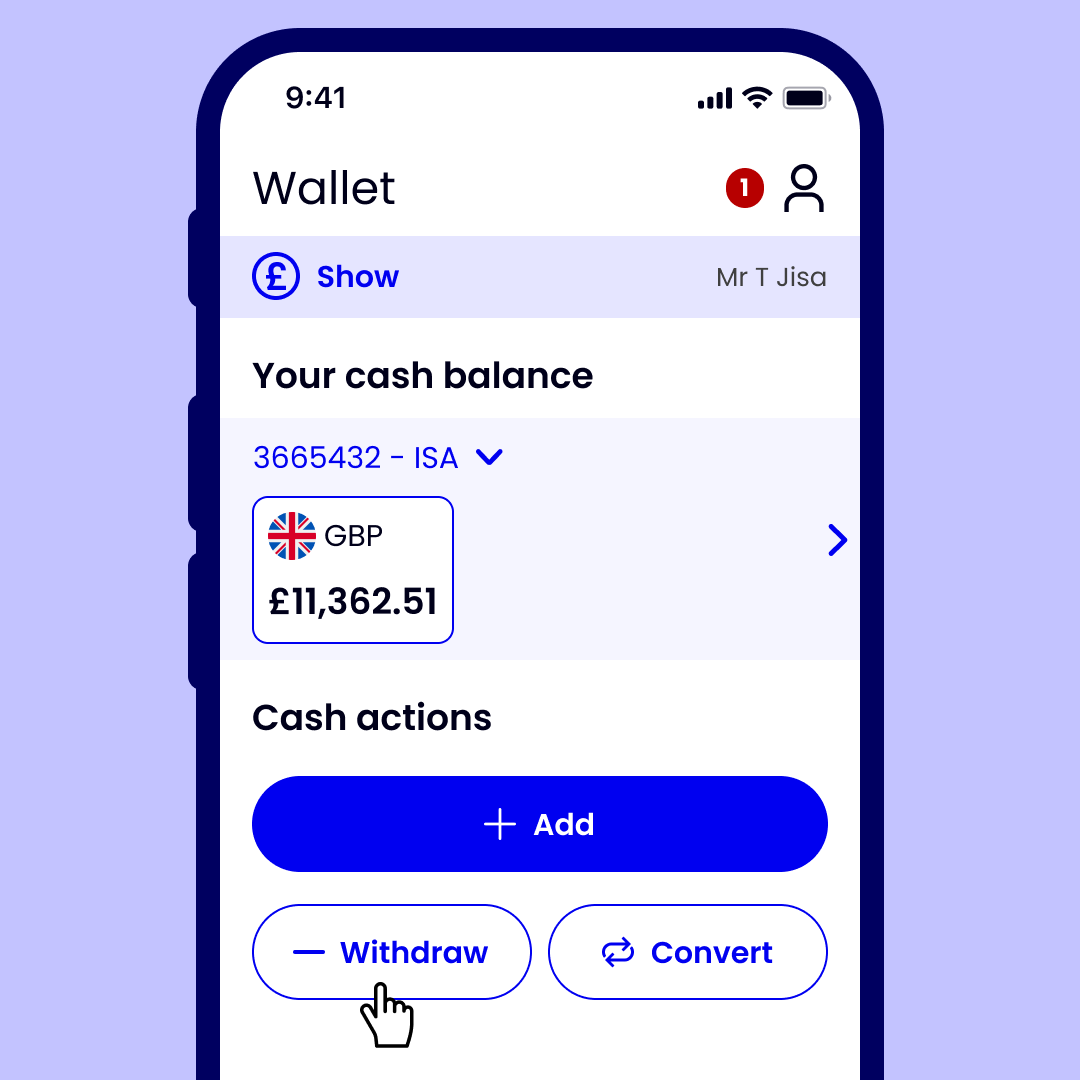

Direct Debit

Direct Debit is the easiest way to make regular cash payments into an ISA.

One-off lump sums

Your child can add one-off payments into their ISA as and when they choose.

Parent or guardian contributions

As the child’s parent you can still contribute to your child’s ISA, but not directly. You have to send money to their bank account, and they can then pay it into their ISA account.

What your child can do with their new ISA

If your child doesn’t know where to spend their money, they can keep it in the ISA and let it grow.

Reinvesting in the ISA can help them benefit from compounding. This could lead to their wealth growing faster as the invested money earns returns, and those returns also start earning more returns.

Explore our Learn Hub and ISA guides for next investing steps ideas.

They can now invest up to £20,000 a year without paying tax on gains, which means they keep more of their money. If they want to, they can keep adding money to their account and building their portfolio.

And using our regular investing service, they can invest from as little as £25 a month without having to pay trading fees.

For some inspiration, explore our ISA investment ideas.

Once a Junior ISA matures into an adult ISA, your child can withdraw money into a bank account held in their name. All payments into an ISA use up part of the £20,000 ISA annual allowance and withdrawing money doesn’t restore the allowance.

Once a JISA matures becomes an ISA, your child can also remove the funds and close the account if they want to. There are also other types of ISA accounts, other than the Stocks & Shares ISA, that they could move their money to.

Parents cannot close the account or withdraw funds because the money is legally the child's.

Are you interested in opening a JISA for your child?

Jump-start your child’s future by investing up to £9,000 per year tax-free. Help your child put their strongest financial foot forward and open a Junior Stocks & Shares ISA for free (with the Plus and Premium plans).

And by the time they turn 18, they could be on their way to buying their first car, covering university expenses, or building their investment portfolio.

What happens when a vulnerable child's JISA matures?

When a young person turns 18, they legally become an adult and take full control of their account. At that point, parent or guardian access will end.

However, if your child does not have the capacity to manage their finances independently, there are legal arrangements that can allow you to continue supporting them. For peace of mind, we recommend starting the process well before their 18th birthday.

For more information, please visit the official government website: www.gov.uk/become-deputy