Funds

Expand your portfolio with funds

Find out how funds work and the different types available. Explore our expert insights and ideas to help you choose the right funds for you.

Important information: As investment values can go down as well as up, you may not get back all of the money you invest. If you're unsure about investing, please speak to an authorised financial adviser. Please note images displayed are for illustrative purposes only.

Get started investing in funds

Funds are a type of ‘collective investment’. They work by lots of investors pooling their money together, and a professional fund manager selects which companies to invest the total in.

Funds are a popular choice for many when starting to invest. They’re generally lower risk than investing in individual shares, and you can feel reassured by the fact an expert is taking care of your money.

There are some additional costs associated with investing in funds, which you wouldn’t pay when investing in shares. These costs include the ongoing charges figure, alongside management and transaction fees.

Most popular funds

Want to see what other investors are buying? Here’s our list of the most-bought funds by ii customers over the last quarter. You can also see which are performing best on our top funds page.

Most-bought funds by ii investors

- Vanguard LifeStrategy 80% Equity A Acc (B4PQW15)

- abrdn Global Govt Bond Tracker N GBP Acc (BLKGX49)

- L&G Cash Trust I Inc (BJKGG24)

- Artemis Global Income I Acc (B5ZX1M7)

- Royal London Short Term Money Mkt Y Acc (B8XYYQ8)

- abrdn Global REIT Tracker N (BK5HLJ1)

- abrdn Global Corp Bd Scrnd Trckr N Acc (BDFZ6M4)

- abrdn Global Inflat-Link Bond Trkr N Acc (BDFZ6L3)

- Vanguard FTSE Global All Cp Idx £ Acc (BD3RZ58)

- HSBC FTSE All-World Index C Acc (BMJJJF9)

Source: interactive investor. Note: the top 10 is based on the number of purchases in real time between 1 January to 31 March 2026. Our most popular investments should not be taken as personal recommendations or advice on whether to buy or sell a particular investment.

Why invest in funds?

Funds let you invest in a wide range of companies without picking individual shares. Our Funds and Investment Editor, Kyle Caldwell, talks about why this is a benefit.

“Funds can be a great way to invest because they give you access to a wide range of companies and other types of assets. Typically, 40 to 60 underlying assets are held in a single fund.

Fund investing can also help you to spread your risk, as your chance of returns won’t rest on the performance of a single stock.”

Fund ideas from our experts

With thousands of funds to choose from, it can be difficult to know where to start. To help, our impartial experts have selected ideas for a wide range of funds, investment trusts, and exchange-traded funds (ETFs).

ii Super 60

Narrow down your options with our rigorously researched list of 60 quality funds, ETFs and investment trusts.

ACE 40 sustainable

Align your portfolio with your personal values by choosing an ETF from the UK's first rated list of sustainable investments.

Quick-start Funds

Get off the mark quickly, with one of these low-cost, multi-asset funds. A simple way to help you start investing.

Aberdeen funds and trusts

Take a look at the Aberdeen funds and investment trusts available on the ii platform.

ii’s investment trends and insights

Our market-leading team of experts regularly gather and review the investment trends of over 500,000 ii investors.

Discover the team’s latest insights to help build your knowledge as well as your portfolio.

Great choice, even greater value

Enjoy access to over 3,000 funds, from many of the biggest fund managers. Choose from our wide range of investments and even save on trading fees with our free regular investing service.

Expert lists and top trading tips

Our investment experts pour over the markets daily, so you don’t have to. Invest smarter with better insights, ideas and most-traded lists of funds, ETFs and shares.

On-the-go investing made easy

Never miss an investment opportunity with our easy-to-use mobile app. Track the markets from your pocket and adjust your portfolio at the touch of a button.

Over 25,000 reasons to invest with ii...

Join over 500,000 investors, more than 50% of whom have been with us for over 10 years. See why Investors' Chronicle named us a 5-star platform and their Editor's Choice.

How to invest in funds with ii

To start buying funds with ii, you’ll first need to open an account. Choose from our Stocks & Shares ISA, Self-Invested Personal Pension (SIPP) or Trading Account.

You can open your account in less that 10 minutes, either here on our website or through our mobile app.

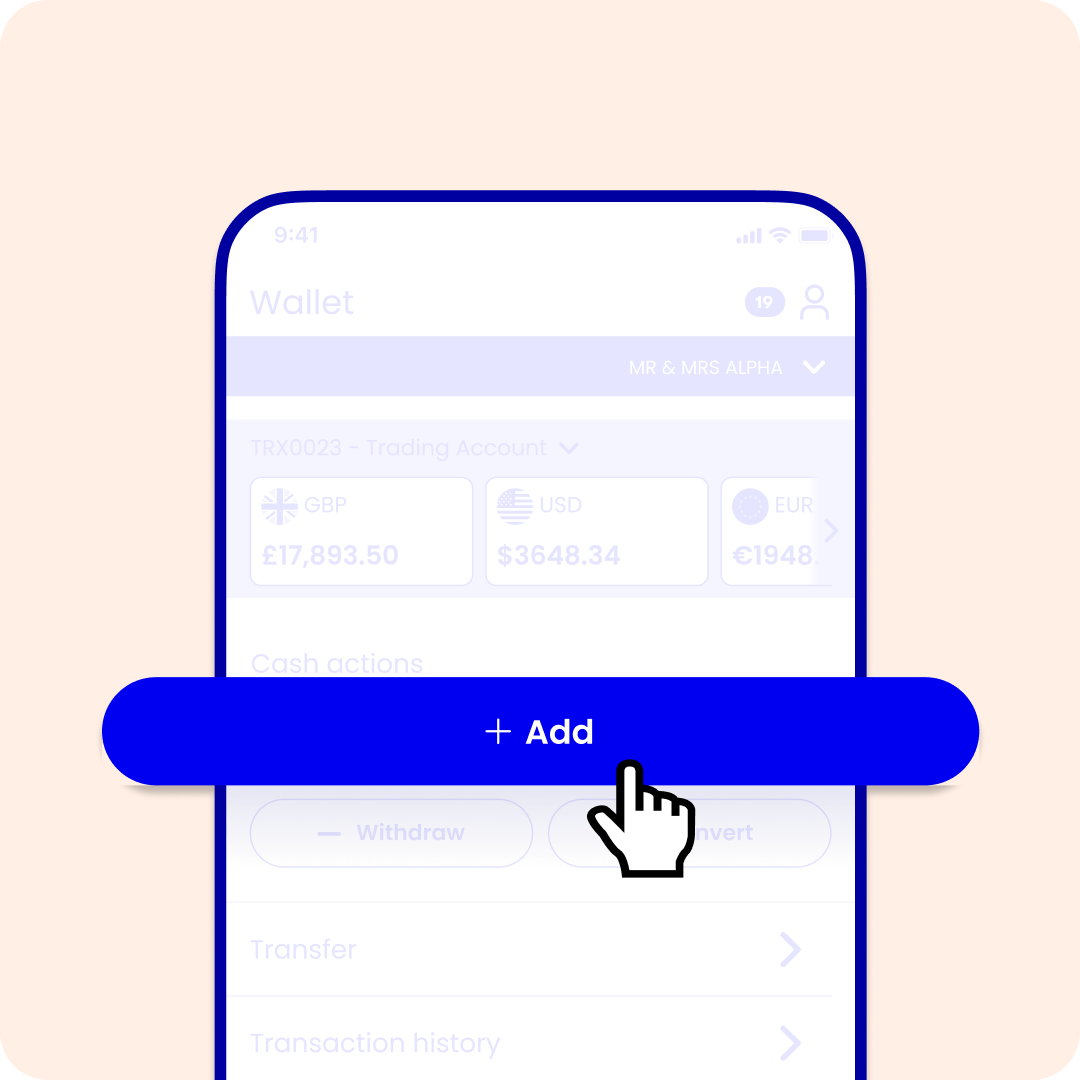

You’ll need to add cash to your account to buy your funds. You can do this by making a one-off payment or setting up a monthly direct debit.

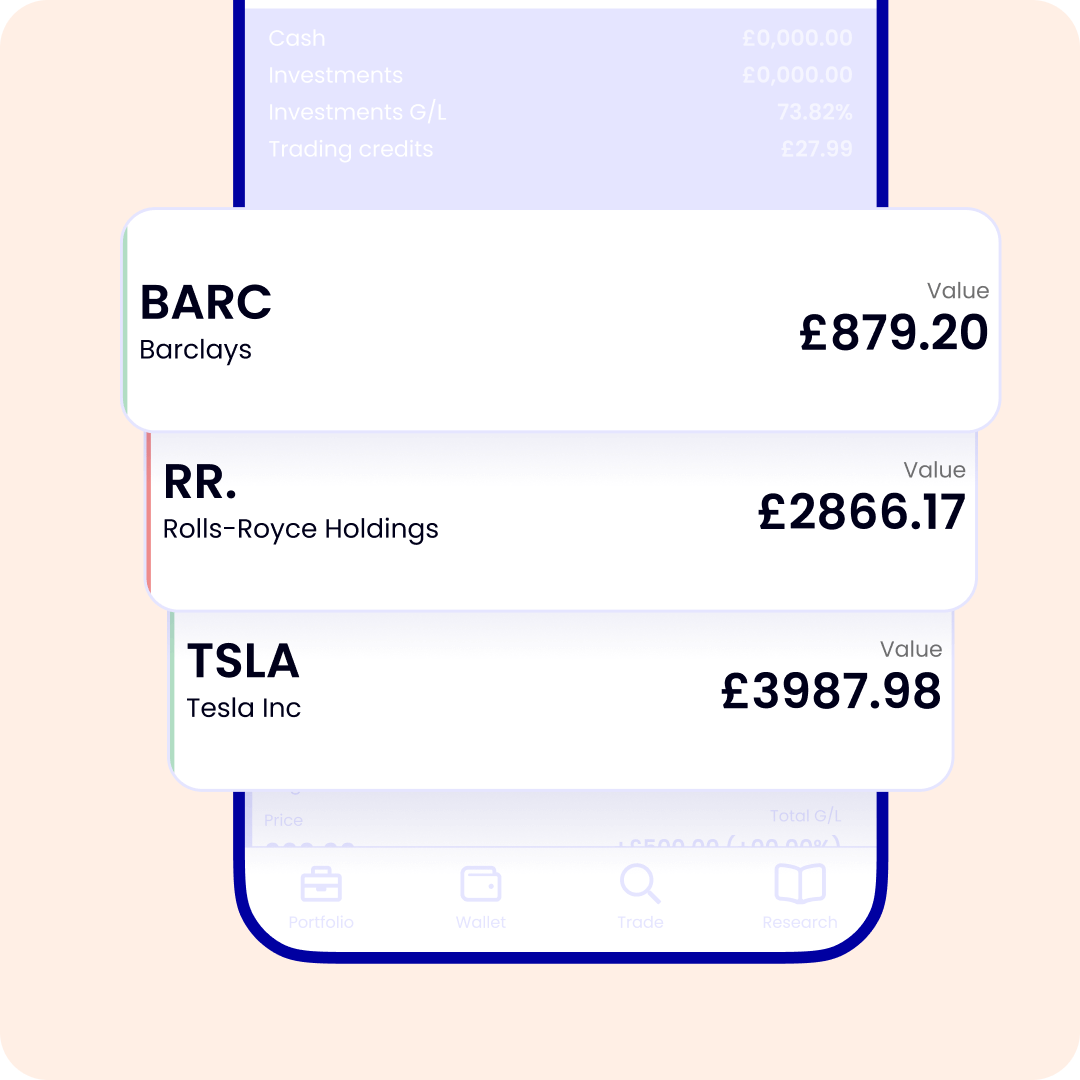

Research the funds you’re interested in and select those you want to invest in. If you need help choosing, remember to explore our expert insights and ideas.

When you know the funds you want, it’s time to buy.

With the cash ready in your account, you can place an order to buy your fund. If you want to invest in the same funds every month, you can always do this with our free regular investing service.

Funds FAQs

A fund is a type of pooled or 'collective' investment that gives investors access to a range of different companies. Each investor in a fund receives shares or units representing a portion of the fund's holdings.

Funds are usually structured as unit trusts or open-ended investment companies (OEICs). In practice there is little difference between these two structures, but a full explanation can be found on our Unit Trusts & OEICS page. These types of funds are sometimes called 'mutual funds', although this is not a commonly used term in the UK. Other types of funds include ETFs and investment trusts.

There are two broad management styles for funds: active and passive. Active funds are looked after by a fund manager who specially selects the underlying investments. The manager constantly checks and balances the fund's investments to keep it on track with its objectives.

Passive funds (also called 'tracker' funds) usually invest in the constituents of a stock market index and will follow the market's fortunes up and down. There is less management involved with passive funds, so they tend to have lower costs than active funds.

Read more about active vs passive investing.

Funds are usually traded once a day at a time set by the fund manager. This means there is often a delay between the time you place an order to buy/sell and when your fund is actually traded. There is also a longer settlement period to factor in when you buy and sell funds. It usually takes between 3 and 4 days for your trade to fully complete and your units in the fund (or cash if you sold) to arrive with you.

You can invest in funds through investment platforms like ii. Before you can invest, you'll need to open an investment account, then research and choose the funds you want to buy. Always remember to check the investing costs, including trading fees, account charges and the fund's ongoing charges (OCF).

Funds are a type of ‘collective investment’. This is where your and other investors’ money is pooled together, and a professional fund manager selects which companies to invest the total in. The fund manager will then manage the underlying investments in the fund, rebalancing it when necessary to ensure it meets its goals.

Traditional funds don’t trade instantly on a stock market as shares do. Instead, they are usually bought and sold once daily at a set time.

Active funds

An actively managed investment fund has an individual fund manager (or a team of managers) who make investment decisions for the fund on what to buy and sell. Investors who buy active funds hope the fund manager(s) will outperform rival active funds and a comparable stock market index.

Passive funds

Passive funds, also known as ‘index trackers’, mirror the composition of a stock market index, such as the FTSE 100. That means there are no active decisions regarding what to buy and sell. Investors should expect the return of a passive fund to be close to the performance of the index it tracks but with a slight lag due to the fund charge. Index trackers can also be structured as exchange-traded funds (ETFs).

Read more about active vs passive funds

Income funds pay out any income generated by the fund, such as dividends from shares or coupons from bonds. While accumulation funds simply reinvest that income back into the pool of money invested by the fund manager.

Many funds offer both an income variety or ‘share class’ and an accumulation share class. The income share class is suited to investors who are ready to take an income from their investments. For example, retirees who want to supplement their retirement income.

On the other hand, the accumulation share class can be a better choice for investors who have the time to build up their investments and pension. This is because the accumulation share class can benefit from the power of compound interest.

'Mutual funds' is essentially another term for investment funds. It’s a term used more commonly in the US.

When you buy and sell funds with ii,you’ll usually pay a one-off trading fee. The amount depends on the type of investment and which price plan you're on. Please see our charges for details.

You can skip the trading charges if you decide to go down the regular investing route when buying ETFs.

Funds also charge a separate annual fee. This is a small percentage of your investment which goes directly to the fund manager. Active funds tend to have an ongoing charges figure (OCF) of between 0.85% and 1% a year. For context, that works out at £85 to £100 on a £10,000 investment. Passive funds are cheaper, with some index funds and ETFs costing less than 0.1%. That would work out at £10 on a £10,000 investment.

Keep up to date with our ii newsletter

The markets move fast. You can move faster. Keep your finger on the pulse with impartial, expert content from our award-winning investment journalists.