Stockwatch: follow director buying in a small-cap showing strength?

With a mixed narrative even before the Iran war, analyst Edmond Jackson ponders whether the macro context will hobble the firm’s micro-level improvements and puts the accent on timing.

14th April 2026 11:02

by Edmond Jackson from interactive investor

When black clouds gather – and what could be worse than a crisis akin to 1973-74 as the restoration of shipping through the Strait of Hormuz gets trickier? – it is interesting to check shares showing strength.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Cashback Offers

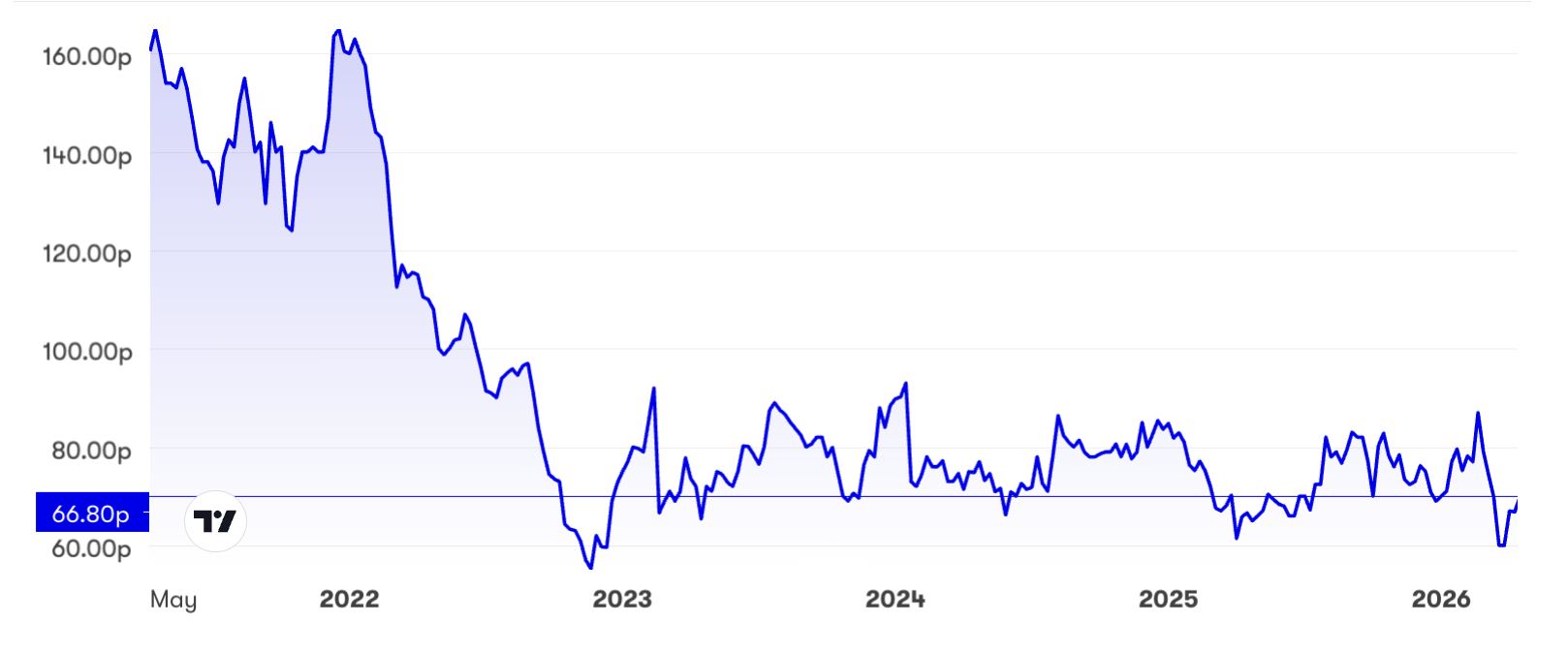

Among yesterday’s risers was small-cap industrial fasteners group Trifast (LSE:TRI), which was up 7% at over 71p, having struck a 59p low on 24 March.

The price had fallen from 87p on 20 February as the Middle East war kicked off, hence effectively this could be little more than a mean-reversion to a sideways trend over the last three years:

Source: interactive investor. Past performance is not a guide to future performance.

Trifast did, however, deliver a superb bull run from 9p in the wake of the 2008 crisis, up to 273p in 2018, but fell to 60p by November 2022, establishing this sideways range.

This is a manufacturer of bolts, nuts, screws and washers that is allegedly “niche”, if no blazing new technology, and prone to the wider business cycle. Major industries are involved such as automotive, electronics and medical.

A current market value of £95 million doesn’t exactly flag a growth business given that Trifast floated 32 years ago. But, at 0.45x expected sales of £214 million in the latest year to 31 March and a latest price/earnings (PE) of 8x – with guidance having been affirmed for numbers due – this looks to me like the kind of smaller well-established company liable to end up in a takeover.

- The Income Investor: a FTSE 100 dividend play after 21% fall

- Stockwatch: why I’m upgrading this mid-cap share to buy

When I tried to compare operating margins, it appears that Trifast is the last listed industrial fasteners company left.

A big dilemma, however, is cyclicality; why the shares plunged over 30% in response to the outbreak of the Middle East war. Forecasts for 30% earnings per share (EPS) growth in the March 2027 year, for a PEG ratio of 0.25, are moonshine if industry is facing $150 oil.

Trifast - financial summary

Year end 31 Mar

| 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 187.0 | 198 | 209 | 200 | 188 | 219 | 244 | 234 | 223 |

| Operating margin (%) | 9.6 | 9.6 | 8.2 | 2.0 | 4.7 | 5.3 | 0.0 | 2.0 | 4.2 |

| Operating profit (£m) | 17.9 | 19.0 | 17.1 | 4.1 | 8.8 | 11.6 | 0.0 | 4.6 | 9.4 |

| Net profit (£m) | 12.7 | 15.1 | 12.2 | -0.2 | 5.8 | 9.0 | -2.9 | -4.4 | 1.0 |

| EPS - reported (p) | 10.4 | 12.2 | 9.9 | -0.2 | 4.3 | 6.6 | -2.1 | -3.3 | 0.9 |

| EPS - normalised (p) | 10.3 | 11.9 | 9.9 | 3.9 | 4.7 | 6.9 | 2.0 | -2.6 | 1.9 |

| Operating cashflow/share (p) | 14.5 | 8.2 | 8.0 | 12.7 | 17.4 | -13.1 | 2.2 | 21.2 | 12.5 |

| Capital expenditure/share (p) | 2.4 | 2.9 | 3.4 | 3.8 | 2.3 | 3.8 | 0.0 | 0.0 | 0.0 |

| Free cashflow/share (p) | 12.1 | 5.3 | 4.6 | 8.9 | 15.1 | -16.9 | 2.2 | 21.2 | 12.5 |

| Dividend/share (p) | 3.5 | 3.9 | 4.3 | 1.2 | 1.6 | 2.1 | 2.3 | 1.8 | 1.8 |

| Covered by earnings (x) | 3.0 | 3.2 | 2.3 | -0.2 | 2.7 | 3.1 | -0.9 | -1.1 | 0.4 |

| Return on total capital (%) | 14.6 | 15.0 | 12.9 | 2.3 | 5.4 | 5.7 | 0.0 | 2.5 | 5.0 |

| Cash (£m) | 24.6 | 26.2 | 25.2 | 28.7 | 30.3 | 26.7 | 31.8 | 20.9 | 24.3 |

| Net debt (£m) | 6.5 | 7.4 | 14.2 | 30.3 | -0.5 | 37.5 | 53.8 | 39.4 | 38.7 |

| Net assets (£m) | 102 | 110 | 121 | 116 | 132 | 139 | 136 | 124 | 121.0 |

| Net assets per share (p) | 84.5 | 90.9 | 99.3 | 94.9 | 96.9 | 102 | 99.8 | 91.3 | 90.1 |

Source: historic company REFS and company accounts.

Operating margins and returns on capital are modest at around 5%, but despite a somewhat volatile net profit and EPS trend, cash flow per share has traded substantially in excess of EPS.

Directors have bought strongly up to the end of March

They have clearly regarded a circa 60p to 80p monotonous trading range as an opportunity. It probably reflects confidence at the mid-stage of a transformation plan to improve margin and profit.

Last 7 January, a non-executive director – who is also a director of Harwood Capital which owns 17.4% as Trifast’s largest shareholder – bought £14,000 worth at 70p then piled in for over £896,000 worth at 59.75p on 26 March. The chief executive bought £99,000 worth at 80p on 16 February, and on 30 March another non-executive director bought £6,900 worth at 63p.

This has followed regular buying by various directors, especially the director of Harwood who accumulated nearly £1.5 million worth from December 2024 to October 2025 at prices from 63p to 82p. Harwood itself raised its stake by 1.6 million shares to 23.7 million on 26 March albeit involved Slater Investments reducing by 3.6 million shares to hold 12.1 million or 8.9%.

Manifestly the directors have conviction about value despite a 4% expected revenue slip in this latest financial year due to “an overall softer demand environment from ongoing tariff disruption, unprecedented challenges in the UK automotive sector, partially offset by growth in smart infrastructure especially in the US”. A mixed narrative then, even before the Middle East war.

- Insider: bosses bet big on turnaround play and 'AI winner'

- Shares for the future: new score for riskier FTSE 250 stock

Sales are well diversified internationally but this has meant adverse foreign exchange movements impacting, especially a weaker dollar given that around a quarter of revenue is US-generated.

UK performance has been affected by higher national insurance and minimum wage increases, but if the low-paid are a significant element then it doesn’t exactly flag a high-end business. There have also been cyberattacks, including in Europe, although [these are] a liability generally nowadays. Automotive sales fell in both territories and a concern is chronic ex-growth in a wider shift to electric vehicles, especially from China (if they can get shipped now, of course).

The US has provided growth despite a currency translation headwind, with sales up 8% in the first-half-year driven by smart infrastructure up 15% and medical equipment by 32%. However, such revenue rises were partly driven by tariff-inclusion, hence lower margins.

Will the macro context allow micro-level improvements to raise profit?

When I last wrote about Trifast in July 2024 – suggesting “buy” at 75p – I was attracted by the programme under way to recover operating margins that had been near 10% in 2017 and 2018 at the reported level.

I thought the upside case significantly rested on such margin improvement; yet the last accounts – interims to 30 September 2025 – showed a relatively modest 4.3% at the reported level, or 6.2% if adjusting for intangibles amortisation and costs of the recovery programme. This had improved from 3.3% at the reported operating level to September 2024 or 5.4% adjusted.

Among private firms, Companies House accounts show, for example, AFC Europe on a 6.4% operating margin with £28.2 million revenue in 2024.

Last November’s operational review from Trifast also cited continuing to rebalance into faster-growing markets and sectors; yet its largest division remains UK automotive, which is fundamentally an industry under pressure. Fasteners are also a competitive sector, hence the time being taken to recover margins, and also because manufacturing is capital intensive with significant fixed costs.

This puts the onus on getting timing right; where the directors’ actions say “buy” and the share is currently in jack-rabbit mode as investors ponder the economic fallout from the Middle East.

- Five ways to hit the 2026-27 tax year running

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Last February, Peel Hunt – Trifast’s broker – maintained a target price of 140p versus a prevailing 80p price, after a third-quarter update affirmed full-year 2026 guidance. However, that implies a 21x PE based on normalised EPS of 6.6p, falling near 16x if 8.6p is achieved to March 2027. I respect the improvement programme, and how, in 2018, EPS around 12p was achieved on sub-£200 million revenue. In the current environment, I still wouldn’t expect the market to push the PE on such a cyclical into the mid-teens.

Meanwhile, a total dividend around 2p per share in respect of this latest year implies a near 3% yield. Yet while net debt appears to be only around £17 million, net finance costs took 45% of operating profit. In terms of financial risk, this looks rather mixed should economies turn down.

Re-balancing from automotive towards smart infrastructure and medical equipment, and exiting low-margin customers means Trifast is in the proverbial “well-positioned when the upturn comes” situation. It’s potentially a bid target before that happens.

Peel Hunt argues in favour of respecting what Trifast has achieved in sluggish market conditions, which is fair, but what if high energy prices reverberate around the economy?

A ‘comprehensive update on performance’ is due later this month

This will also affect sentiment. The trend in directors buying up to restrictions kicking in, implies it should be good.

Around 70p currently, I retain a “buy” stance, albeit I’m more cautious that Trifast’s broker and would target more like 100p – with scope for plenty of variance according to how the global economy pans out.

In a recession scenario should the US/Iran conflict drag on, volatility will continue.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.