Stockwatch: how much notice should we take of Warren Buffett?

He’s the best-known and most widely followed professional investor in history, but stocks have become more expensive and economies fragile. Analyst Edmond Jackson gives his view on the 95-year-old Sage of Omaha.

4th November 2025 12:38

by Edmond Jackson from interactive investor

Warren Buffett, CEO of Berkshire Hathaway. Photo by Johannes EISELE/AFP via Getty Images.

The revelation that Berkshire Hathaway Inc Class B (NYSE:BRK.B) has accumulated record cash holdings - $377.5 billion (£287.7 billion) in cash and near-term US Treasury Bills, or nearly 54% of its net assets - is eye-popping.

That’s not just a red flag about some US equity valuations but also the economy, and is key to understanding Warren Buffett’s style.

Yet his sayings can be somewhat contradictory, and it’s interesting to critically consider his key points to smaller investors.

- Invest with ii: Buy US Stocks from UK | Most-traded US Stocks | Cashback Offers

In his annual reports and AGM conversations, a regular Buffett theme over the decades has been long-term prosperity of the US economy. There’s a sense of “trust in Uncle Sam”, explaining why he has barely diversified outside US businesses in his investment career (albeit global exposure via multinationals).

He has also advocated that smaller investors use a low-cost S&P 500 index fund as the best means to achieve satisfactory returns, and put regular sums into the market this way.

It’s akin to the “semi-strong” theory of market efficiency, which you might describe in less abstract terms as “trust market prices” – where guessing market moves is probably futile. A further implication is that doing well over the long run is achievable by owning the whole market rather than fretting over stock selection.

Yet on the grand scale of Berkshire Hathaway – one of the top 10 US companies and the first non-tech firm to break the $1 trillion valuation – does the exact opposite. Its portfolio of marketable securities is highly concentrated, its five largest holdings constituting 66% of equities at 30 September, down from 71% at the end of 2024. These are American Express Co (NYSE:AXP), Apple Inc (NASDAQ:AAPL), Bank of America Corp (NYSE:BAC), Coca-Cola Co (NYSE:KO) and Chevron Corp (NYSE:CVX).

And Buffett seems to be trading more amid caution at valuations and possibly scope for a cyclical downturn.

Looking at Berkshire’s trend in filings this year, cyclicals such as communications have been targeted: T-Mobile US Inc (NASDAQ:TMUS) is now eliminated and Charter Communications Inc Class A (NASDAQ:CHTR) cut 46.5% to $435 million, albeit small in portfolio context.

- ii view: Buffett builds Berkshire Hathaway cash pile to record high

- How to invest like the best: Warren Buffett

Most notably in terms of a macro view, the Bank of America holding has been pared down 41% since mid-2024 to $28.6 billion. Banks are usually a leading indicator of the stock market – something you ideally buy in the trough of a recession and sell after a boom.

At Berkshire’s 2024 AGM, and in relation to Apple, Buffett also cited the prospect of the peak marginal corporate income tax rate rising in future – as justification for selling down Apple (and by implication possibly Bank of America also). This to me feels like another adage-break in the sense not to put tax considerations before quality of business.

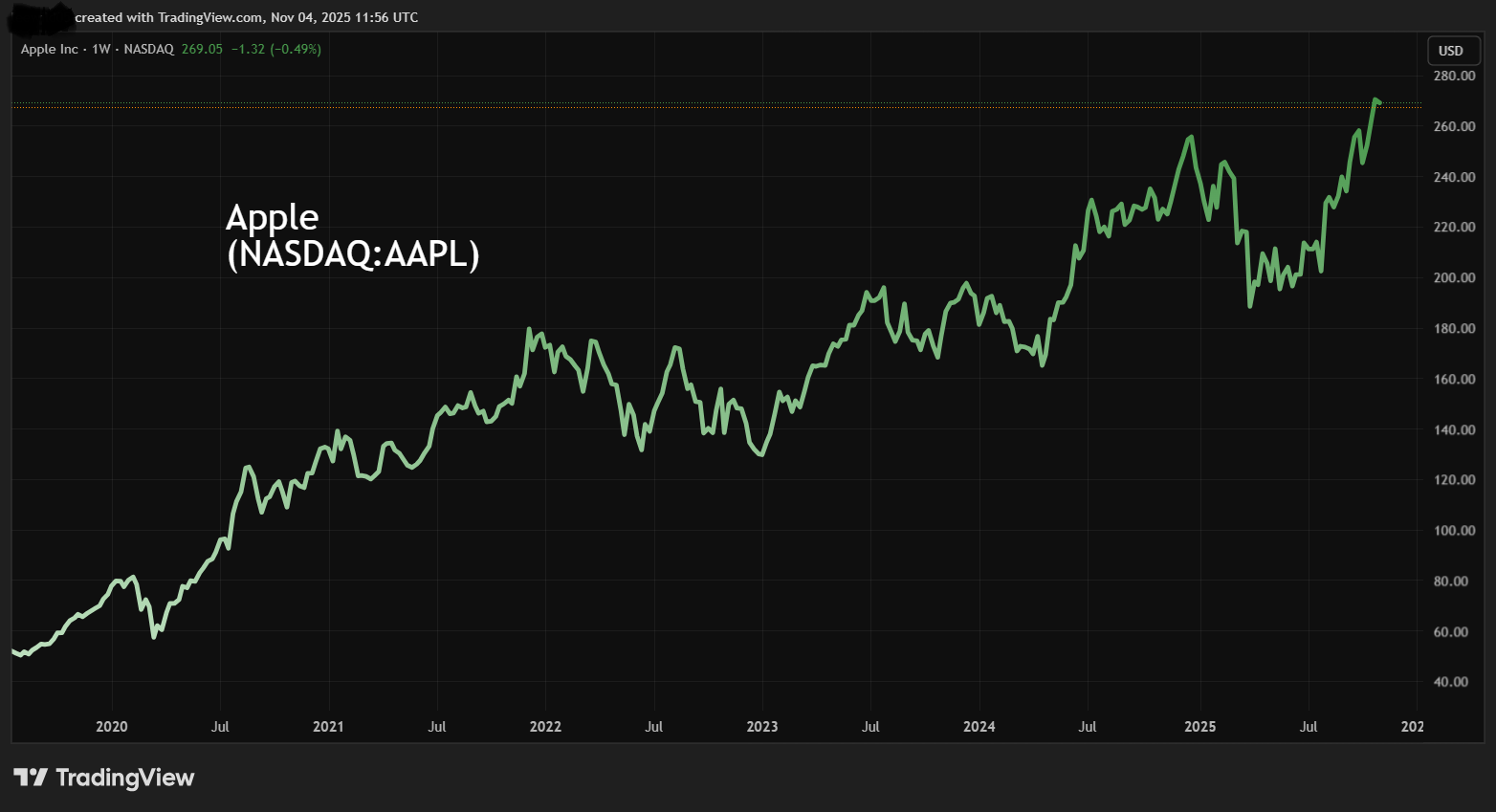

Amber lights for Apple equity

Berkshire’s Apple stake is another candidate for scrutiny. Last year it was cut by two-thirds, but in a demonstration of how the world’s shrewdest investor can still get things “wrong”, Apple has continued to advance despite the March-April slide on tariff fears:

Source: TradingView. Past performance is not a guide to future performance.

Past “bubble” periods in markets suggest this latest tech-driven one could still be early stage and last several years. Compared with valuations in 1999-2000, today’s tech giants have colossal earning power, which the rush to adopt AI is helping advance, for now anyway.

Perhaps Buffett would say we have no real idea of how long such overvaluation might last and that the long-term median valuation should be respected. Apple’s trailing price/earnings (PE) ratio is in the mid-thirties (I recall drawing attention some years ago on 12x when Apple was out of favour) and in Buffett’s investing lifetime there is a precedent of how the “Nifty 50” growth stocks de-rated and Polaroid filed for bankruptcy in 2001 after it failed to adapt.

I do not imply a parallel with Apple but note that various Chinese Android smartphone manufacturers now enjoy their devices rated equally if not better than iPhones, so if the cult of Apple users contracts over years, then, yes, the stock’s PE can mean-revert down.

Despite Apple’s market value soaring over 24% in the third quarter of 2025, it is speculated that Berkshire continued to offload, given that its latest report cites the cost basis of its consumer products equity holdings down $1.2 billion from Q2. This category is dominated by the Apple stake.

Time will tell whether Buffett’s conservatism – to protect value by locking it in – will win versus the adage to “run winners”. Yet Berkshire can only sell into strength of demand, otherwise valuation would plunge or even face illiquidity.

So, while I have been bullish about Apple in the past, and for smaller nimble investors still regard it as a “hold”, best note this Berkshire selling in a context of strong Chinese competition challenging Apple’s profit margin.

Ultimately Buffett embraces active over passive investing

In Berkshire Hathaway’s annual reports Buffett has often said “our favourite holding period is forever”, but this may not square with the real world.

He has also often enjoyed quoting Benjamin Graham – a 20th-century dean of value investing – who used to characterise share investing as being in a partnership with “Mr Market”, an incurable manic-depressive. Sometimes he will bid/offer you extravagant prices, other times well below what the businesses could fetch in a private sale. Intelligent investors must avoid falling under his spell and be patient to do the opposite.

Such a view can still reconcile with stock market valuations being “semi-strong efficient” in the long run; for example, mean-reversion up or down. It accords with another Graham/Buffett adage about how the market is a voting machine in the short run but a weighing machine longer term.

Where does this leave Berkshire Hathaway as an investment proposition?

Over the last 30 or so years, I have encountered investors who not unreasonably believe that it is worth having a share in Berkshire’s fortune, given that Buffett is also highly attuned at acquiring private companies. Last month, for example, the petrochemicals division of Occidental Petroleum Corp (NYSE:OXY) was acquired for $9.7 billion.

While the A class are the original higher-priced shares with more voting rights, the B are more affordable with significantly less voting power but identical investment performance. They have had a very good run up to $530 last May. Indeed, they are up about eight-fold since the 2008 financial crisis, although more recently appeared to drop below trend-line:

Source: TradingView. Past performance is not a guide to future performance.

At around $475 currently, the trailing PE is 15x but there is no yield as Buffett would see paying out as a thumbs down on his capital allocation, but until this year Berkshire has periodically engaged in share buybacks.

On the face of it, third-quarter results showing operating profit up 34% year-on-year to $13.5 billion – driven mainly by insurance, railroad and energy – implies momentum from the fully owned businesses that are strongly positioned. Insurance underwriting soared over 200% to $2.37 billion.

Yet there appear at least two cautionary stances among US brokers following Berkshire, on the grounds of Buffett’s succession risk at age 95 and also headwinds that could weigh on earnings and share performance. Vehicle insurer Geico and railroad Burlington Northern Santa Fe may face cyclical and structural challenges.

- Wild’s Winter Portfolios 2025: winning stocks revealed

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

A chief risk I see is the US economy becoming two-tier: big tech and AI masking a trend towards sluggish growth elsewhere, which might resolve in due course, but maybe not if tariff-induced inflation creeps in.

Greg Abel was Buffett’s clear first choice as successor CEO and has been with Berkshire some 25 years; time enough to ingrain plenty of Buffett’s mindset.

I regard Berkshire as essentially a well-honed spread of US businesses and shares, yet the economy is in question and Buffett’s actions suggest the market is high-priced. At best, I therefore rate “hold” and would let events play out further.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.