Stockwatch: should investors back these four oil stocks?

With military conflict breaking out across the Middle East, analyst Edmond Jackson discusses whether it’s time to use oil & gas as a portfolio hedge.

3rd March 2026 11:51

by Edmond Jackson from interactive investor

Should we trust the rerating of various oil & gas shares, or are they more likely a knee-jerk response to Gulf hostilities that will pass like the majority have in recent decades?

The obvious immediate answer depends on how long the conflict in the Middle East lasts. During the 1991 Iraq war, I recall $120 oil, although this soon fell back once supply security was reaffirmed. It initially felt great to be weighted in oil shares and cash, but in the medium term proved a relative loss-maker versus sitting tight or buying the drop.

- Learn with ii: How to become an ISA millionaire | ISA Investment Ideas | Top ISA Funds

This time around, however, warnings of $100 oil if the Strait of Hormuz becomes compromised, is today a reality after Iran’s Revolutionary Guard warned that all ships attempting passage will be “set on fire”. I was surprised that oil prices barely flinched initially – modern traders probably have no recollection of the 1973 oil embargo that fuelled inflation and petrol queues – but Brent crude is up 3.3% to $80.30 this morning.

It reflects a dilemma where US/Israeli air attacks will likely take much longer to achieve security on the ground, especially regarding Iran’s widespread proxies such as the Houthi rebels who are to resume attacks on shipping in the Red Sea corridor.

Such problems become self-fulfilling when insurers withdraw support like they are doing now. A fifth of global seaborne oil and liquefied natural gas (LNG) passes through the Strait of Hormuz, and a third of urea trade – the most widely used fertiliser.

This is now a worst-case scenario for the global economy and is likely to escalate before it de-escalates. Higher inflation – possibly stagflation – looks very possible, which is certainly a dilemma for monetary policy.

- Market snapshot: FTSE 100 looking for a floor

- Insider: management buy these two stocks after prices drop

Last Sunday, the OPEC oil cartel agreed a modest rise in output from April, but yesterday Saudi Arabia’s biggest domestic oil refinery was shut down after an Iranian drone strike, and other oil & gas facilities across the Middle East were closed as a precaution. This reminds me of 2019 drone strikes on Saudi facilities by Houthi rebels.

Why balanced portfolios contain oil & gas shares

Despite its less ethical appeal amid environmental concerns, we are witnessing why oil & gas has, over the long run, been considered a necessary hedge.

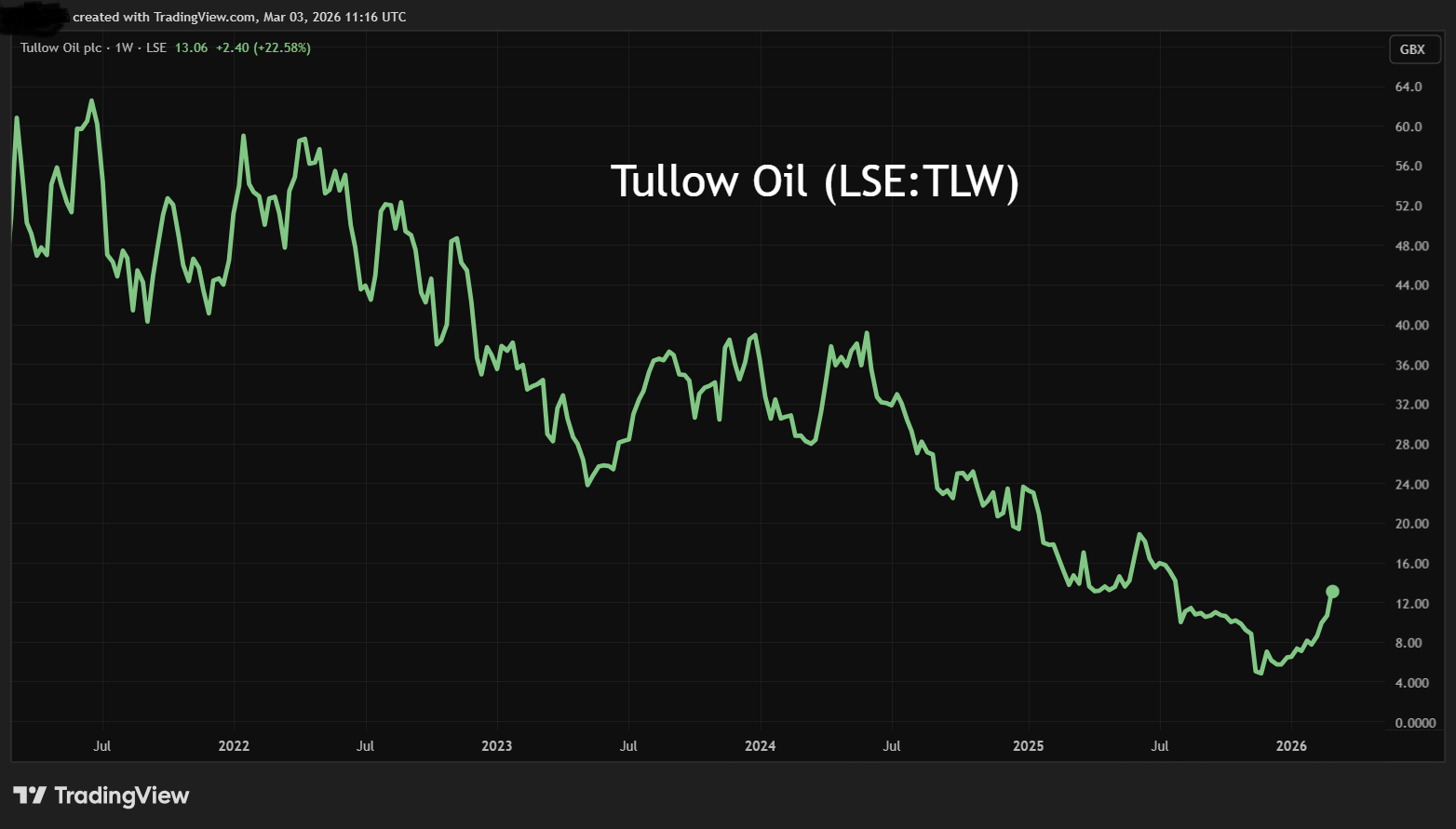

Indeed, a circa 20% rise in oil prices this year, even before this conflict kicked off, shows how the oil market is attuned to events. Related shares mostly lagged this rise given that the commodity will always be more sensitive to expectations alone, but come the reality of disruption, share prices have jumped. Tullow Oil (LSE:TLW) was London’s biggest riser, up 20% yesterday given that it remains highly indebted, hence material changes in oil prices having greater effect.

Small-caps such as Tullow and EnQuest (LSE:ENQ) have also been in a relative bear market versus BP (LSE:BP.) and Shell (LSE:SHEL).

It certainly shows the big companies coping better in a relatively low oil price environment lately, as the sense of excess supply conflated with demand disruption as global tariffs rose. But if energy prices remain elevated, then initial inflection points in small caps likely have more upside from here.

Basic valuation criteria vary, with the sharpest contrasts in small cap:

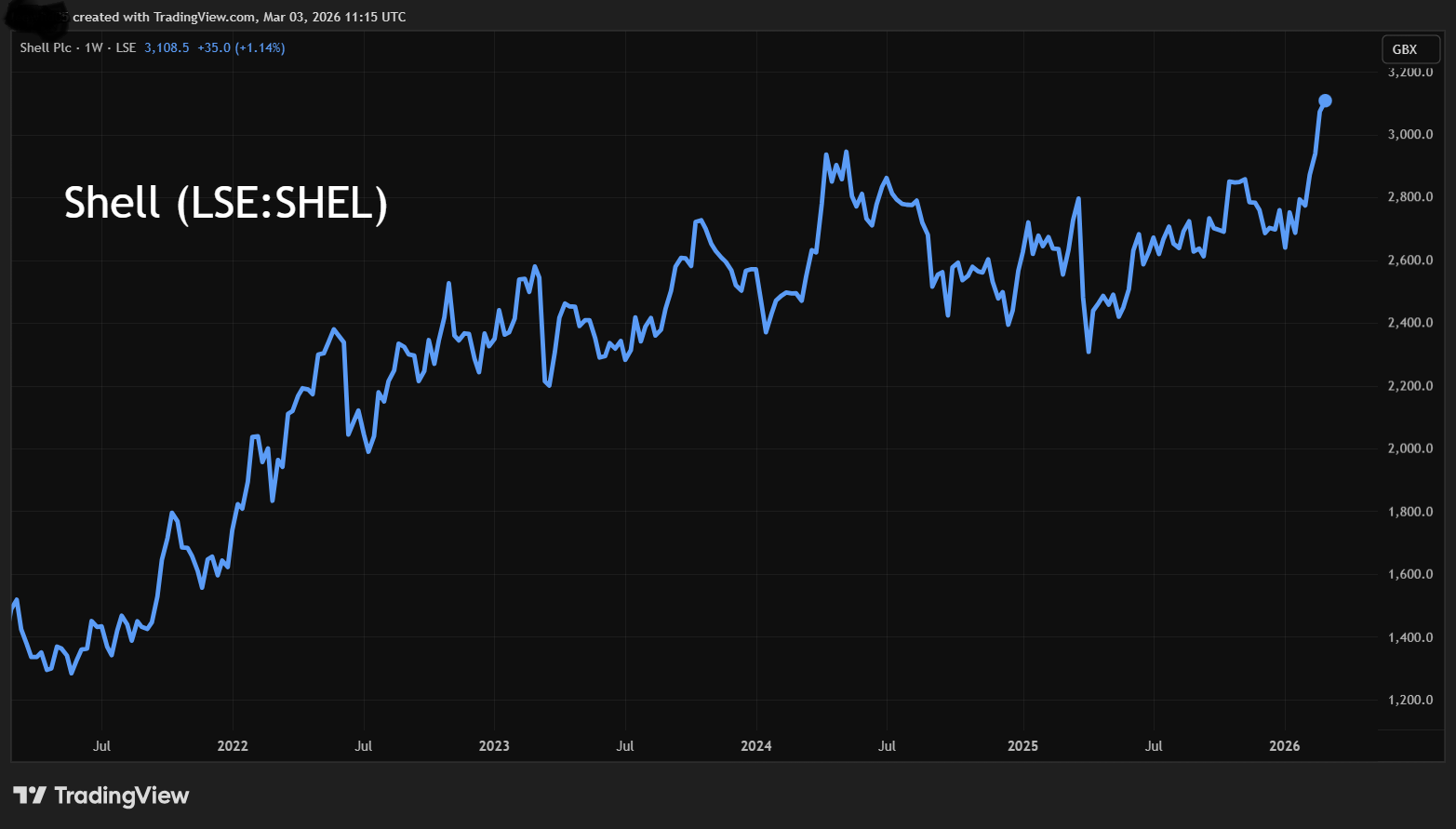

At 493p, BP is on a 12-month forward price/earnings (PE) ratio (at recent oil prices though) of 14.5x with a 5.2% yield and at nearly 2x net asset value (NAV). At 3,152p, Shell is on a 13.1x PE, 3.6x yield and 1.4x NAV.

Source: TradingView. Past performance is not a guide to future performance.

Yet Tullow at 13p is on a 6.6x PE, zero yield and near 17p negative NAV due to around £1.7 billion equivalent of net debt. Enquest’s net gearing is less astounding at around 200%, and, at 17.8p, trades at 1.3x NAV and a 3.8% yield but is expected to be loss-making both for 2025 and 2026 due to North Sea windfall taxes. Might that change though, with elevated energy prices?

Worth establishing a portfolio hedge?

Hedging at current prices is by no means straightforward. If a worst-case scenario evolves for stagflation, oil & gas shares will see profit-taking as energy demand falls. If the war proves relatively short-lived as the US administration anticipates, oil prices are also going to retreat.

Yet it’s unclear whether air bombardments can achieve this to restore security of shipping. Even a capitulation of the Revolutionary Guard might leave Iran’s proxies well-fuelled with hatred of the West.

Furthermore, even if OPEC raises output there are no real logistical alternatives to the Strait of Hormuz. Two pipelines run across Saudi Arabia but one is at capacity and another could accommodate an additional two million barrels equivalent per day whereas the Strait of Hormuz transits 18 million. Another pipeline across the United Arab Emirates can handle just under two million.

I would therefore steel for a worst-case of chronic disruption given the antagonists involved are now ideologically motivated. Stamping out actions by proxies will be hard and insurers will be liable to keep a firm line.

The likes of BP and Shell are going to appeal to professional investors and, given their fetish with quarterly relative performance figures, if a trait develops towards big oil for portfolio hedging this way it will have positive effect. I would therefore apply a medium-term “buy” stance to both.

Small caps – especially Tullow, given the potential status change for debt risk – have more leverage, hence appeal to speculators.

Capricious past hazards of backing Tullow

I took a speculative “buy” stance on Tullow at 45p in September 2021, and again at 34p in January 2023 when a director was adding substantially to his holding. Indeed, he kept doing so, last buying £238,000 worth at 11.9p in August. Over 2025, he bought a total £468,000 worth and currently holds 28.3 million shares, or 1.92% of the company.

On the short side, Helikon Investments might well be the only hedge fund involved but it has a determined 1.85% exposure, which it raised 0.43% last November.

Source: TradingView. Past performance is not a guide to future performance.

Yet as the “tide in the affairs of men...” saying goes, a major one by way of sustained higher oil prices could now swing Tullow’s fortunes favourably. Determining this properly requires a capable sensitivity analysis to oil-price scenarios.

The sense of a tipping point for earnings is shown even by the recent expectation for around £42.5 million equivalent net profit in 2026 and earnings per share (EPS) of around 2p – with Tullow now able to leverage even better.

- eyeQ: Glencore, Persimmon, Taiwan Semiconductor, Apple

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Rate me damned to fail a third time but the logic of an oil & gas supply crisis, I believe, is on the cards, which means I retain a “buy” stance. Mind, though, how a speculative run would be liable to hit some extent of reversal if disruption is significantly resolved.

EnQuest builds on 2026 market favour

In contrast to Tullow, Enquest has conservative financial criteria: near £1 billion equivalent free cash flow generated since 2021, which is now aiding debt de-leveraging.

A sense of reducing risk was also implied by dividends introduced from the 2024 financial year. It helped the shares up from 10p in January ahead of a robust February operations update.

Source: TradingView. Past performance is not a guide to future performance.

Yet a near-term loss-making scenario appears to follow from an extension of the UK windfall tax to 78% on oil & gas producers. There’s also operational issues such as a third-party infrastructure outage a year ago. EnQuest is thus pivoting towards its Malaysian interests, which will involve costs and time.

My sense is that the UK is liable to end up with a coalition government unable to wrest change in North Sea taxation, hence I am not inclined to get involved. But Reform has pledged to improve oil & gas, so if you reckon on Nigel Farage as prime minister, then EnQuest might rate a long-term “buy”. There are no short positions over the 0.5% disclosure threshold.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.