Wild’s Winter Portfolios 2025: both beat the market

An amazing final month for these seasonal portfolios means they each outperformed the benchmark index this winter. Lee Wild explains how it happened.

13th May 2026 12:07

by Lee Wild from interactive investor

Well, what a six months! In October I was issuing my usual warning that typically accompanies these winter portfolios. “Borrowing costs and inflation will remain an issue, and it’s anyone’s guess what President Trump will do next,” I said. There were fears about an AI bubble, while a strong summer might have exhausted demand for some of our constituent stocks.

Trump’s unique approach to international relations saw the US president imprison the President of Venezuela, threaten to annex Greenland, then start a war against Iran in March that continues to this day. The instability and subsequent oil crisis unsettled global financial markets, but I needn’t have worried.

A strong quarterly earnings season and fresh demand for tech stocks, specifically AI plays, gave markets a boost, with Wall Street making record highs for fun. Bullishness inevitably found its way to UK shores, and while the FTSE 100 is still some way shy of February’s record high, it’s still up 4% in 2026 so far.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Reflecting wider volatility across financial markets, this year’s winter strategy got off to a bad start and was scarred by a couple of big losers. However, there were good months too, and twice as many big winners.

Outperformance in March, where losses were far less than the wider market, and an incredible final month, was reminiscent of a Grand National winner digging deep during the final few furlongs to win by a nose.

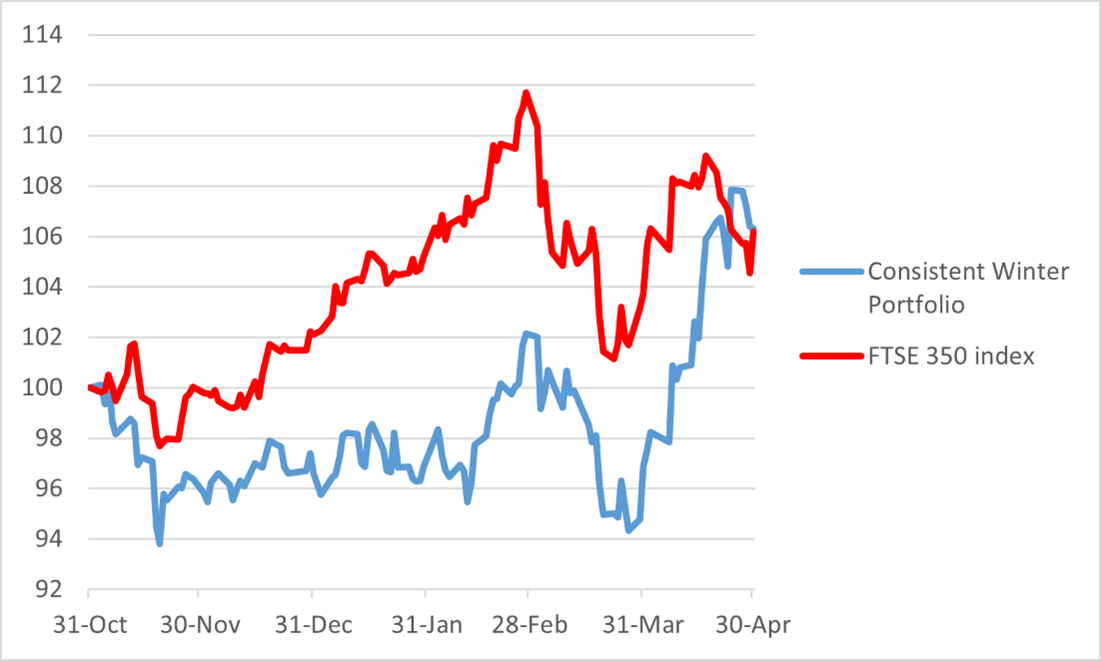

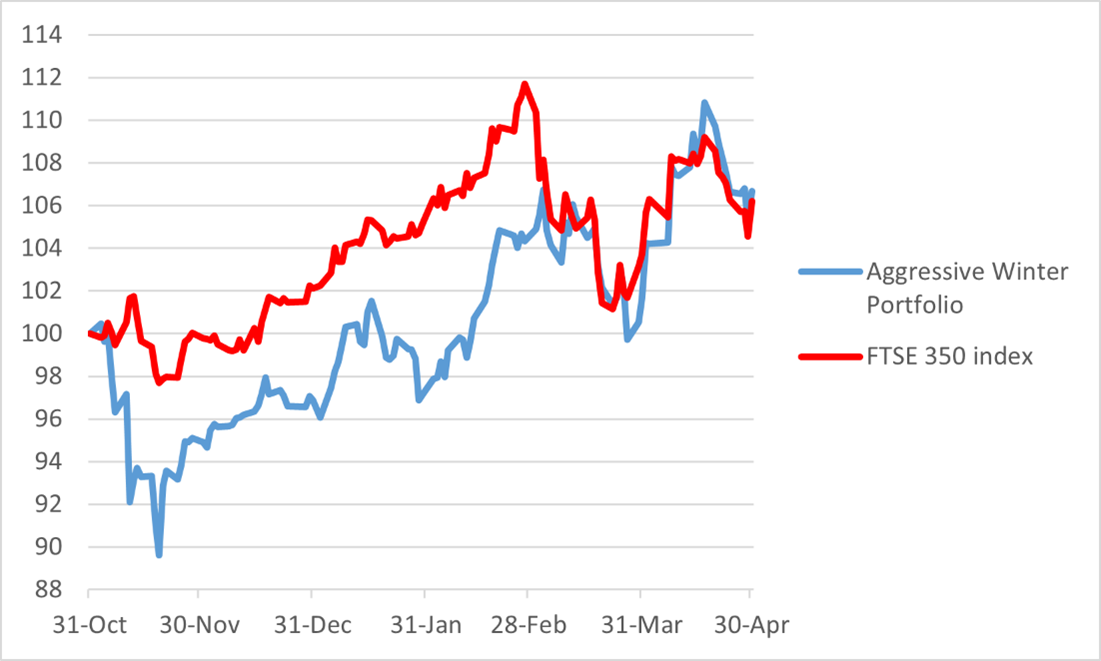

When markets shut on 30 April, Wild’s Consistent Winter Portfolio had risen almost 10% in a month, turning a modest loss since late October into a 6.3% profit for the six-month strategy. A 5% monthly gain for Wild’s Aggressive Winter Portfolio meant the higher-risk basket of shares ended the winter with a 6.7% profit. It meant both portfolios beat the FTSE 350 benchmark index, where a 2.4% jump in April took seasonal returns to 6.2%.

Now let’s run through the star stocks and name and shame the dogs.

Wild’s Consistent Winter Portfolio 2025-26

Past performance is not a guide to future performance.

The consistent portfolio of more historically reliable stocks was held back by bus and train operator FirstGroup. It had looked an odd inclusion when we ran the data in October, yet records show it had risen in nine of the previous 10 winters, returning an average profit of 14.3%. Not this time.

Jus a couple of weeks after the investment winter began, FirstGroup issued mixed results and announced no new share buyback scheme. Already fragile markets didn’t like it. Despite a few glimmers of hope, the trend was overwhelmingly negative throughout the season. After a 2% drop in April, the shares ended the winter down 22.6%.

Soft-drinks maker AG Barr had looked like a stinker early on too, despite a 9/10 record of positive winter returns at an average 11.4%. Shares had slumped 8% by January, then delivered a 15% rally through February. But it proved unsustainable, and the conclusion was a 4.2% loss this winter.

- Insider: directors pile into FTSE 100 stock at huge discount

- The Income Investor: prospects for Taylor Wimpey and Persimmon

But, as I said, there were twice as many big winners over the six months. IT services firm Computacenter was the best in this portfolio. A stunning rally of 25.5% extended winter gains to 30.1%, driven by an upgrade to profit forecasts as customers raced to secure supplies.

Halma did brilliantly too. The safety products conglomerate soared 16% last month, taking its return this winter to 24.3% and exceeding its winter average over the past decade of 10%.

Insurance firm Admiral Group had a terrible January as investors feared Anthropic’s new AI tools could threaten business models across many industries, including insurance. There were analyst price target downgrades, too, but a sense that AI was not an imminent risk had bulls chasing the shares up over 7% in April for a six-month gain of 3.1%.

Wild’s Aggressive Winter Portfolio 2025-26

Past performance is not a guide to future performance.

FirstGroup left its mark on the aggressive portfolio too given its impressive historic performance gained it entry to this higher risk basket of shares. And there was another awful stock that proved a drag all winter.

Less than a fortnight into the winter strategy, meat packer and seafood supplier Hilton Food Group warned about profit growth in 2026, blaming the impact of inflation on demand for white fish and delays restarting its Greek salmon factory because of the US government shutdown. Shares fell 25% and didn’t improve much over the entire six months, ending the winter down 16.4%.

However, despite these two big losses, the aggressive portfolio was the best performer this year. That was down to stellar returns from engineering contractor Keller Group and fantasy wargames company Games Workshop Group, and a 9.2% jump at defence contractor BAE Systems.

- Stockwatch: a FTSE 250 company in buying territory

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Keller was a steady ship through the winter except for a blip at the start and during the market rout in March. A 16% rally in April was the icing on the cake of a great winter which saw the stock return almost 41%.

Games Workshop was up over 20% within a month of the strategy’s launch before retreating during the first six weeks of 2026. However, it had rallied back to a record high by the end of the winter season, a 10% jump in April leaving the stock up 22.3% for the six-month strategy.

The US and European defence industries, hot sectors since Russia invaded Ukraine, have only grown stronger following President Trump’s international posturing and pressure put on other NATO members to spend more on their militaries. Share price performance at BAE Systems has become more volatile, yet despite losing 7% in the final month of winter, had still generated a 9.2% return since the end of October.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.